BLMN remains on our Investment Ideas list as a long.

Our bullish bias on BLMN centered on the following key points:

- The largest shareholder, who also controls the board, could not sit around and let the stock languish.

- Industry sales were improving.

- The company could restructure its portfolio to better allocate capital.

Today, the company took an important first step in right-sizing the organization. However, we still believe there is more to do. Despite the moves announced today, we believe the company continues to operate an unsustainable business model comprised of a portfolio of (now) four different casual dining brands.

With that being said, an improvement in industry sales, current brand initiatives, and peak food costs (should become a tailwind in 2015) continue to provide plenty of reasons to be long the stock.

The important announcements made today included:

- Restructuring the business in Korea.

- Selling the Roy’s business.

- Right-sizing the home office by selling off two company planes and trimming headcount.

While this is certainly a great start (and we commend management for this), we don’t think they went far enough. In fact, we believe the rationale behind selling off Roy’s could be directly applied to Carrabba’s – at a minimum. According to CEO Liz Smith, Roy’s is a small part of Bloomin’s portfolio and “not a priority for investment given competing opportunities.”

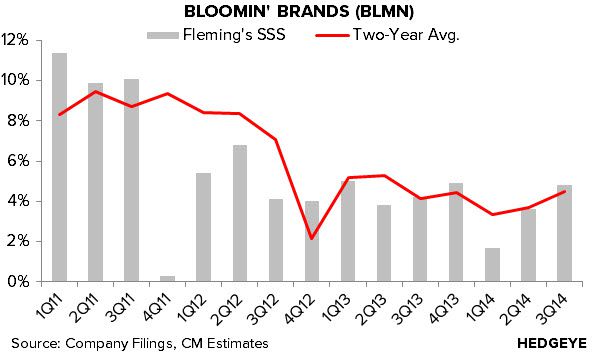

We believe the same could be said for Carrabba’s. In our view, outperforming Knapp Track is hardly something to be proud of, particularly when considering you are in the process of rolling out weekday lunch. Keeping a brand like Carrabba’s because it is better than bad doesn’t make it a compelling investment. The chart below suggests the concept is far from fixed and should be sold off.

The company is hosting its analyst meeting in NYC in December, where we plan to learn more about 2015.

The Good

- Restructuring the business in Korea; plan to close 34 underperforming restaurants; working toward optimal asset base; smaller fleet of stronger restaurants

- Selling the Roy’s business

- Right-sizing the home office team; eliminated a significant number of corporate positions; sold off two corporate planes

- Outback comps +4.8%; all aspects of the business performed well; working to reclaim steak authority; focused on LTO’s, plate presentation and advertising

- Bonefish comps +2.6%; introduced new core menu in 3Q; feedback has been encouraging; new platforms have been well-received; culinary forward brand; brought in executive chef from Seasons 52

- Fleming’s comps +4.8%; high level of innovation; well-positioned within high-end steak category

- 59% of Outback and 54% of Carrabba’s offering weekday lunch; lunch sales growing in restaurants that have had lunch for more than a year

- Brazil continues to perform at a very high level; opening new restaurants as quickly as possible; 16 new Outback’s this year; plan to open first Carrabba’s next year

- Opened 16 system-wide locations in 3Q

- YTD total openings at 37 locations; 55-60 full-year unit growth guidance

- Raised SSS guidance; full-year expectations now at 1-1.5%; plan to continue to meaningfully outperform the industry

- Reaffirmed full-year EPS in the range of $1.05-1.10; hinted toward the higher-end of that range; could surprise if current sales environment continues

The Bad

- Carrabba’s comps -1.2%; challenge is marketing and menu; working on next iteration of menu that will include lighter options and better value; using LTO’s and marketing to drive traffic in the meantime; management remains confident in the brand

- Commodity inflation expected to be 3%

- Aggressive new unit growth; capex expected to be between $215-235 million for the year; new guidance reflects fewer new stores and remodels than anticipated

Research Recap

09/25/14 BLMN: Same as it Ever Was

10/02/14 Bullish on Bloomin'

Feel free to call, or email, with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst