EARNINGS CALENDAR

COMPANY HIGHLIGHTS

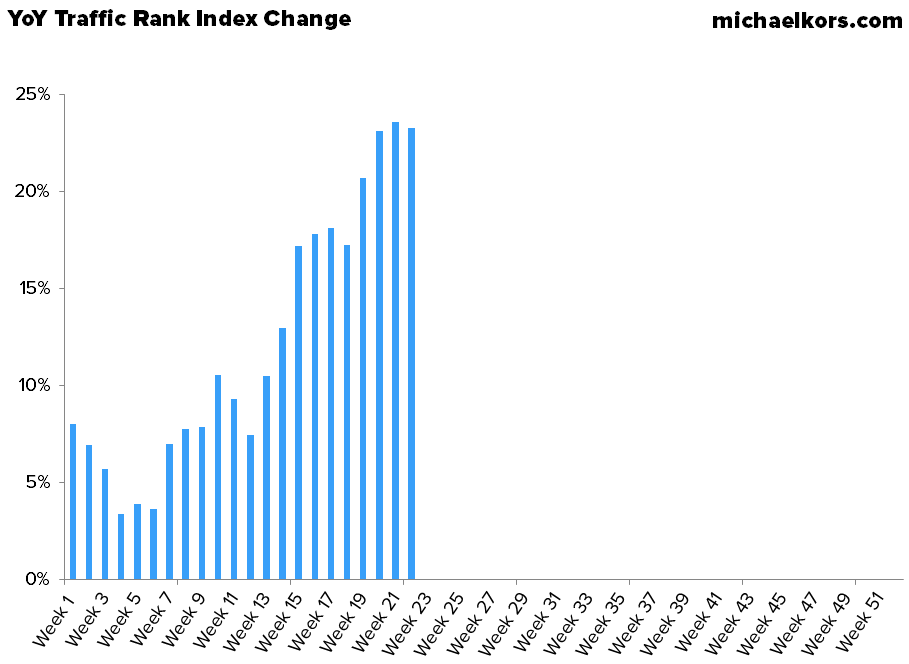

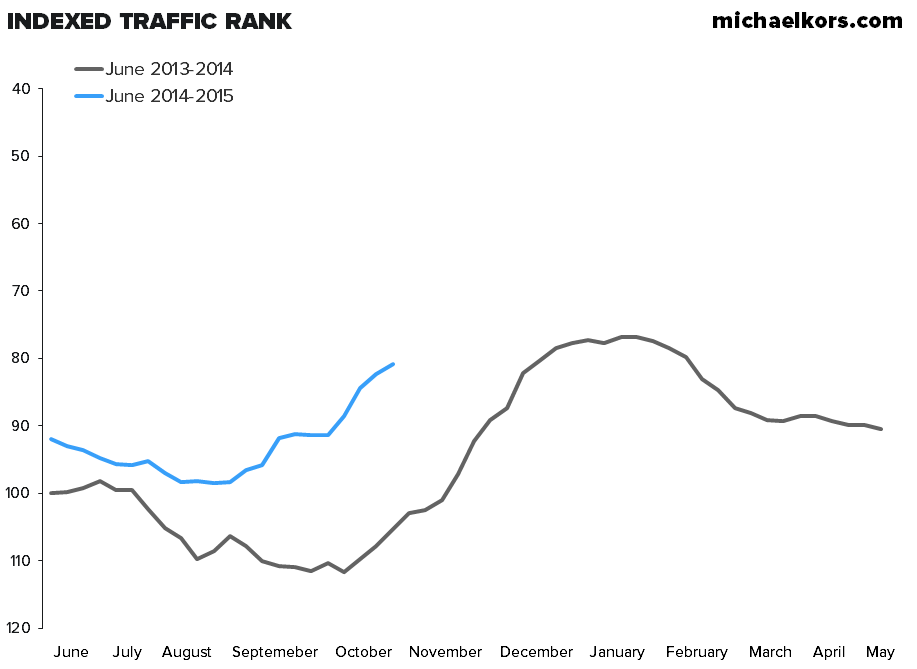

KORS INTO THE PRINT

We don't have a call on KORS right now, but we're positively predisposed headed into the print tomorrow. We all know that KORS is one of those companies that can't just 'beat the quarter'. It's the kind of company that does not know how to miss, having beat estimates by an average of 29% since the IPO. The closest it came to missing was a beat of only 5%, or $0.03ps. That was almost exactly a year ago. It was KORS' weakest comp, wholesale growth, and margin performance of the year. As we anniversary that event, we don't think estimates correctly reflect the leverage on the upside. Furthermore, our internet tracking indicator is shoring continued strength on a sequential and on a year/year basis. We're modeling $1.00, vs the Street at $0.88 and guidance of $0.85-$0.87. We don't have enough confidence in next year's numbers to make a big bullish call on this one. But into the quarter, we're not concerned.

LB - Free Shipping Offer

VS has used Free Shipping as an offensive weapon in the past (one of the first to do so, actually), but this is a continuation of the trend that we think will plague the rest of retail. Though LB is a high-end brand with a very loyal customer base, we'd note that even a powerhouse like Victoria's Secret can't easily absorb free shipping costs due to a relatively low average basket size. It's high-ticket retailers like Nordstrom and Brands like Nike and Ralph Lauren that could absorb shipping costs without a material hit to margins.

OTHER NEWS

WMT, TGT, AMZN - Walmart holiday plans include reduced prices on 20,000 products, free shipping on hot items

- "Walmart is upping the ante on holiday shopping. The chain announced that, starting Saturday, Nov. 1, it will reduce prices on more than 20,000 items. Walmart is also launching its holiday promotions on the first weekend in November to get a jump on what is expected to be a highly competitive selling season."

- "Walmart said it would provide free shipping for online orders of some 100 hot gift items, and free shipping for all online purchases over $50."

- "The move follows Target Corp.’s offer of free shipping on all items, from late October through Dec. 20."

- "Walmart has also expanded its digital offerings to include 7 million items---one million more than last holiday season. Deals typically reserved for Black Friday and Cyber Monday will start on Walmart.com shortly after midnight Pacific Time on Monday, Nov. 3."

MEO - Metro Holds Talks With Karstadt Owner

- "German retail giant Metro AG, which owns the Kaufhof chain of department stores, on Saturday said it had held exploratory talks about purchasing rival Karstadt, adding it was not aggressively pursuing a deal."

KORS - Michael Kors Joins Tech-Accessories World

- "Michael Kors’ expansion into tech accessories goes beyond the smartphone and iPad holders he already offers." "This month, the designer is launching a collection of phone-charging cases, earbuds and two chargers that are designed to resemble women’s cosmetics, as in a lipstick and a compact case."

LVMH - Anthony Ledru to Head Louis Vuitton Americas

- "Louis Vuitton named Anthony Ledru president and chief executive officer of the Americas, effective Jan. 1."

- "Ledru was most recently senior vice president, North America, at Tiffany & Co."

U.S. Gasoline Average Less Than $3 for First Time Since 2010

- "For the first time in almost four years, U.S. drivers are paying less than $3 a gallon at the pump."

- "That’s down from this year’s peak of $3.696 in April, and the first time the average has dipped below $3 since December 2010."