Below are Hedgeye analysts’ latest updates on our six current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

At the end we also feature two pieces of content from our research team, including a note revealing insight on what next week's midterm elections could mean for defense stocks.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

#ConsumerSlowing

U.S. consumer spending fell 0.2% in September, according to a government report released Friday. It’s yet another sign of the weak U.S. consumer.

IDEAS UPDATES

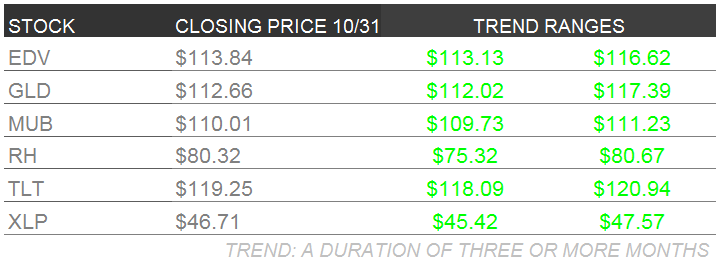

TLT | EDV | XLP | MUB

THE MONEY TEAM: TLT, EDV, MUB & XLP

The Money Team is a masterfully engineered marketing scheme/branding group consisting of ringleader Floyd “Money” Mayweather, 50 Cent, Justin Bieber, Lil’ Wayne and Warren Buffett. Yes, that Warren Buffett.

With respect to our Macro Team’s bullish bias TLT, EDV, MUB and XLP, these positions have held up masterfully in the context of a barrage of universal bullishness over the past ~10 trading days. Specifically, these positions continue to evade even the toughest “punches” from the same investor consensus that has been negative on long duration fixed income all year – much like the great “Money” Mayweather himself.

Also like Floyd, they have been throwing counterpunches of their own – in the form of this week’s slowing economic data, none more important than the Q3 GDP print:

- Headline: 3.5% QoQ SAAR from 4.6% prior

- YoY: 2.3% from 2.6% prior

- Consumption: 1.8% QoQ SAAR from 2.5% prior

- Investment: 1% QoQ SAAR from 19% prior

- Net Exports: 7.8% QoQ SAAR from 11.1% prior

- Gross Domestic Purchases: 2.1% QoQ SAAR from 4.8% prior

- Real Final Sales to Gross Domestic Purchasers: 2.7% QoQ SAAR from 3.4% prior

In fact, one could argue that the lone bright spot in the Q3 GDP report was “G” – a.k.a. pre-election government spending, which accelerated to 4.6% QoQ SAAR from 1.7% prior and contributed 24% (83bps) of the 350bps headline figure.

Our multi-cycle backtest data shows that the rate-of-change of the rate-of-change (i.e. 2nd derivative) in real GDP has been the primary determinant of the direction of bond yields in the U.S. And since our models continue to call for slowing (and falling inflation) over the intermediate term, we continue to think rates are likely to test/make new lows over that duration.

As such, defensively positioned investors should continue to outperform their counterparts as we inch closer to year-end.

Remember November 2007?

Of course you do…

GLD

A stronger dollar is not good for the commodities complex. Nor is A Yen bazooka because commodities, priced in U.S. dollars, get cheaper. We’ve been bearish on the commodities space since we entered a QUAD#4 set-up half-way through the year. Consequently, gold has move inversely, which is what we expect:

1-month correlation: -.79

3-month correlation: -.95

6-month correlation: -.84

1 -year correlation: -.58

To be clear on gold we’re wrestling with two conflicting factors and on the strong USD set-up is winning the battle right now.

- For one, our idea about gold’s interaction with Fed policy and the dollar may still manifest because our model is signaling that consensus expectations for growth remain too high and that growth and inflation are decelerating in the United States.

- In the meantime the relative currency debasement from the BOJ and ECB since we added Gold to investing ideas at the end of May has strengthened the dollar and hurt the price of gold.

With Yen-finity, and the final step of fed tapering from the Federal Reserve ending this week, gold took a big hit, and we would not buy it right here in real-time alerts. Gold failed at its first attempt to move back above its intermediate-term TREND line, and we will wait and watch for follow-through over the next week to see if Yen-finity can move the YEN to a level against the USD that can hold.

With the strong negative correlations inherent in a QUAD#4 deflationary set-up and a breakout in the VIX, our risk ranges in big macro widen out (the absolute price movements needed to generate overbought and oversold signals are larger). Therefore the chance of gold testing its $1231 intermediate-term TREND line again is greater in an environment of higher volatility. Stay tuned for direction.

RH

One of the most powerful growth algorithms in the consumer space. We think that by 2018 the company will earn $11 per share.

Common perception is that RH is building a bunch of palaces and hoping that people will show up to shop. We think about it the other way around…they are creating assortments of product across multiple categories in the home space, and are subsequently taking a massive piece of a category where they only have 2-3% share. Yes, bigger stores are a part of this, which is critical to support the kind of product extensions we’ll see from RH.

Currently, the Legacy 9,000 sq. ft. stores only house 10% of the SKUs and run at about $10mm per store. The 25,000 Design Galleries highlight closer to 30% of the product, and they average a ‘per foot productivity’ rate that is 2x the existing core.

People often ask us about why RH has the right to expand into new categories of Home. People asked that same question about Ralph Lauren in the 1980s when he expanded beyond neckties and polo shirts. This remains our favorite name in retail.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

Midterm Elections and Defense Stocks

Editor’s Note: We thought we’d do something special this week, and take you behind the scenes of Hedgeye’s research team. Below, Jay Van Sciver, our Industrials sector head, answers a question about defense stocks and next week’s midterm elections.

Question:

With the US Government spending more on defense in the third quarter and it looking like the Republicans will probably get a Senate majority, how do defense stocks look for investment now?

Answer:

This is a big question and each contractor can have its pluses and minuses, particularly smaller ones. That said, here is a broad answer:

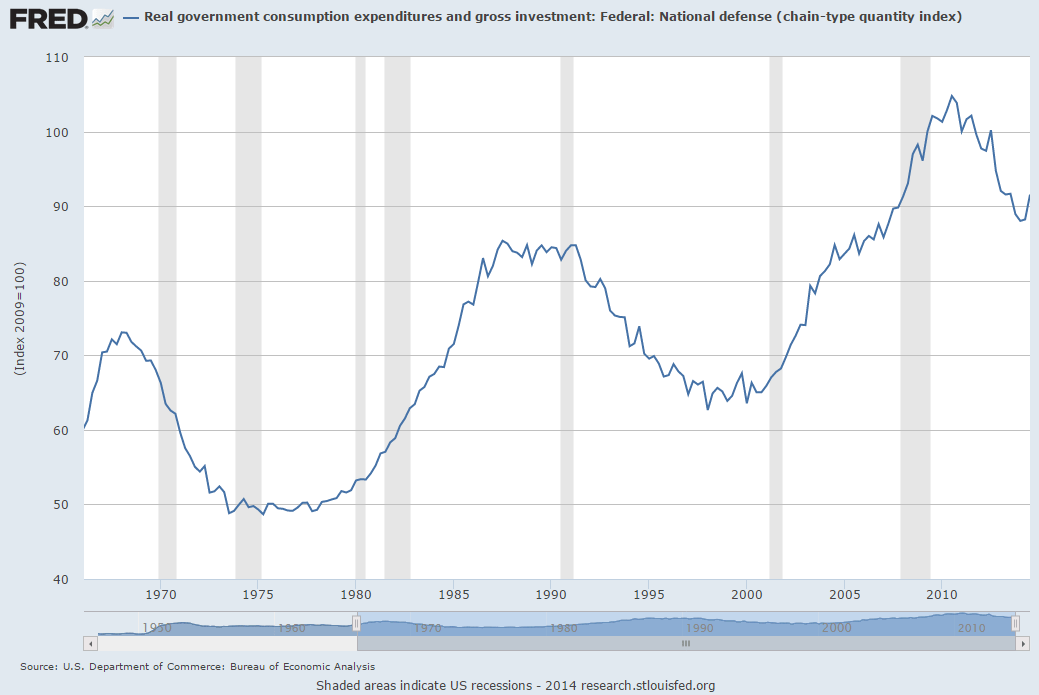

The question relates to the blip up on the right of the chart below. In the grand scheme, when defense spending declines, it tends to decline for about a decade. Defense cuts tend to be a bit reflexive, just as buildups are. We built down during conflicts, like the first Iraq war, too. Judging by history, we still have a long period of declining real defense spending ahead of us.

Procurement, which impacts contractors, tends to be even more cyclical. Cuts in defense spending can also take a while to filter through to contractor reports. The blip up is partly driven by the urge to commit funds before the government fiscal year-end at the end of 3Q (use it, or lose it), which is bigger because of the last budget deal.

As for whether to buy defense stocks, my answer is “No!” They group has been bid up on the expectation that dividend increases (it’s an interest rate sensitive group) will follow better cash flow from changes in the way the government reimburses pension costs.

While positive, accelerated pension payments do not change the value of contractors all that much because the government has owed them reimbursement – it was just behind in the payments. DoD is just paying faster now.

What also changed, we think, is that the Overseas Contingency Operations (OCO) funding has been used to protect defense budgets from steeper cuts. In a sense, this could be view as a misdirection of what are supposed to be funds for active engagements toward base spending. Regardless, the OCO funds are exempt from sequestration and are a fantastic political tool to keep spending up AND look tough on deficits.

These two factors have pushed valuations beyond historical norms during a builddown, which is pretty exceptional. We show Relative EV/Sales for NOC below, since P/Es are often hard to use for cyclicals (many contractors had very low earnings/losses in first half of 1990s).

As for Republicans, it seems that there are isolationist/deficit hawks in the party that tend to split its traditional support of big defense. Neither party seems to want to flinch on the grand deficit reduction bargain. Washington is a funny place, but midterms do not look very impactful. Bigger changes may come after 2016.

The group lacks a good downside catalyst at the moment, but we are certainly looking for one!

Under Armour: Market Share Math Matters

(Click on the title to unlock this content)

Here's our Retail sector team's take on athletic retailer Under Armour from the day when the company reported its third quarter earnings.