COMPANY HIGHLIGHTS

WMT - Wal-Mart Weighs Matching Online Prices

(http://online.wsj.com/articles/wal-mart-weighs-matching-online-prices-during-holidays-1414672782)

- "Wal-Mart executives are discussing whether to go ahead with the price-matching program, which would expand its one for local brick-and-mortar competitors, according to spokeswoman Deisha Barnett. Under consideration is how much Wal-Mart might lose if the program were to go nationwide, people familiar with the matter said."

- "Ms. Barnett said the company’s focus is on taking care of customers and said store managers have had discretion to match certain online prices for customers for some time."

Takeaway: Translation…WMT is going to ultimately offer price matching on all online purchases, ie. AMZN. The next step will be price matching and free shipping. We think that the concept of consumers paying for shipping will be a distant memory in 24 months. Of course, companies don't agree with us. But that's because they'll ultimately offer free shipping because they have to, not because they want to. This trend should be powerful enough to trigger the next round of bankruptcies.

NKE - LEBRON'S ARROGANT ATTITUDE AND POOR PERFORMANCE GOES AGAINST A KILLER NIKE MEDIA OFFENSIVE

(http://news.nike.com/news/nike-basketball-debuts-the-lebron-james-together-film)

Takeaway: This 'Together' film by Nike is one of the best we've seen from the company in a very long time. It's seemingly complimentary to LBJ's first home game in his return to Cleveland. Unfortunately, he didn't play well, and the Knicks walked away with the win. That's not the end of the world. Nike never bases its advertising on an athlete/team winning or losing a specific event. Nike is excellent at playing off of, and often creating, the emotion around an event -- win or lose. Note, it fared so poorly in the World Cup, but made out financially better than Adidas. The problem in this instance is LBJ himself. After the team's pre-game shootaround, the guy said, and we quote…

"For me, I know all of us shouldn't take this moment for granted,' James said. 'This is probably one of the biggest sporting events that is up there ever."

Really, LBJ? Don't you think that is just a little arrogant and cocky in light of all the greatest moments in US Sports history? How about The Immaculate Reception/Franco Harris, the 1969 Miracle Mets, NC State's NCAA hoops victory in 1983, Dan Jansen's 1994 Gold Medal, Rulon Gardner tearing down the Russian wrestling empire, the 1999 Women's World Cup Victory, Spitz/Phelps 15 collective Golds, the Miracle on Ice, or how about Jesse Owens sticking it to Hitler in the 1936 Olympics in Berlin. Seriously King James, do you really think that your triumphant return to Cleveland is the one of the biggest sporting events -- ever? "Ever" is a long time.

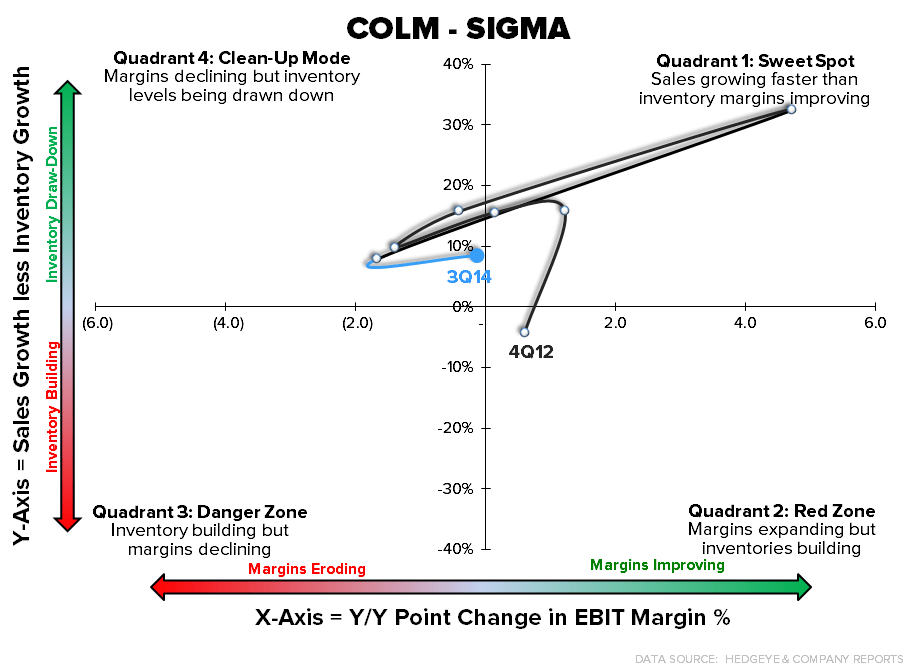

COLM - 3Q14 Earnings

OTHER NEWS

KSS - Kohl’s Kicks Off Holiday 2014 Bigger Than Ever

(http://phx.corporate-ir.net/phoenix.zhtml?c=60706&p=irol-newsArticle&ID=1983615)

- "Kohl’s Department Stores announced it will open its doors at 6 p.m. on Thanksgiving Day, giving customers more time than ever before to shop for top brands, exclusive products and amazing holiday gifts. Kohl’s will inspire customers with a huge assortment of the season’s most-wanted gifts and stocking stuffers, incredible savings opportunities all season long and an easier, convenient customer experience when shopping in-store or on Kohls.com with mobile, tablet or other devices."

AMZN - Amazon Cuts Price

(http://www.wwd.com/beauty-industry-news/financial/amazon-cuts-price-8016716?module=Business-latest)

- "In what amounted to the first shot in a promotional war, the $74 billion e-commerce giant said it would start its holiday price cuts on Saturday with a countdown to Black Friday featuring “even more deals, all day, every day."

- "'This year, we will have more than 15,000 hand-selected, limited-time promotions on hot products, including new early-access deals for Prime members on many Lightning Deals from Amazon.com and daily sales events on MyHabit,' said Steve Shure, vice president of worldwide marketing at Amazon."

FDO, DG, DLTR - Dollar General Extends Tender Offer to Acquire Family Dollar to December 31, 2014

(https://investor.shareholder.com/dollar/releasedetail.cfm?ReleaseID=879599)

- "Dollar General Corporation today announced that it has extended its tender offer to acquire all outstanding shares of Family Dollar Stores, Inc. for $80.00 per share in cash (including associated preferred share purchase rights) to 5:00 p.m., New York City time, on December 31, 2014, unless further extended."

WMT - Wal-Mart to Close 30 Japan Stores

- "Wal-Mart Stores Inc. plans to close 30 locations in Japan as it rejiggers the operation."

- "The news on Thursday that Wal-Mart’s Seiyu GK will shutter 7 percent of its “nonperforming stores that are not aligned with the company’s strategy” came as Seiyu revealed plans to invest in several areas of strategic focus over the next few years to improve customer experience in stores and provide greater access to online shopping."

COLM - Sorel opens its first pop-up store

(http://www.chainstoreage.com/article/sorel-opens-its-first-pop-store-3)

- "Premium boot brand Sorel opened its first-ever pop-up, in Manhattan's Meatpacking District."

- "The 3,300-sq.-ft. shop is designed in the brand's fashion-meets-utilitarian aesthetic. It features stark contrasts of black and white, and sleek and modern forms."