TODAY’S S&P 500 SET-UP – October 30, 2014

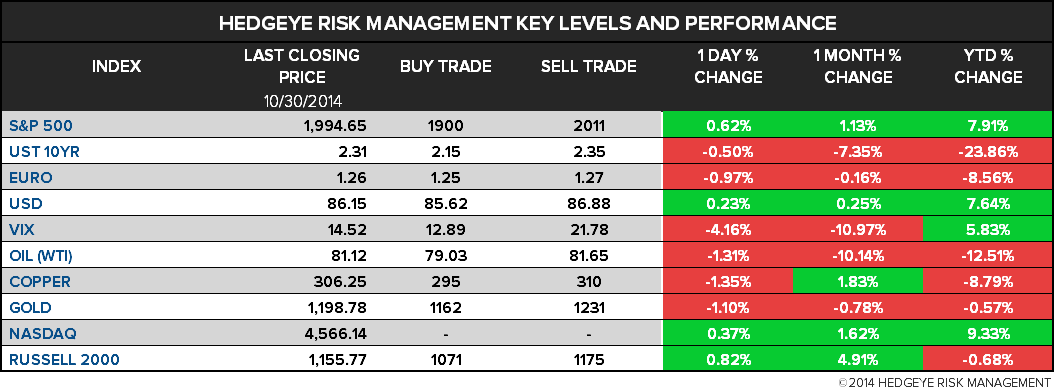

As we look at today's setup for the S&P 500, the range is 111 points or 4.75% downside to 1900 and 0.82% upside to 2011.

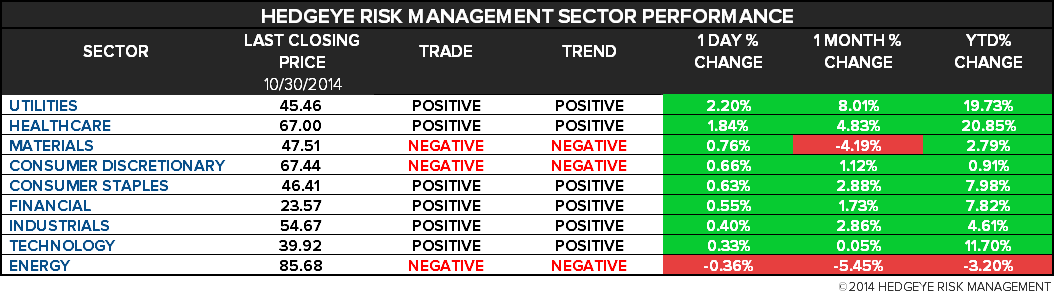

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.85 from 1.84

- VIX closed at 14.52 1 day percent change of -4.16%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Employment Cost Index, 3Q, est. 0.5% (prior 0.7%)

- 8:30am: Personal Income, Sept., est. 0.3% (prior 0.3%)

- 9am: ISM Milwaukee, Oct., est. 60 (prior 63.18)

- 9:45am: MNI Chicago Business (purchasing managers), Oct., est. 60 (prior 60.5)

- 9:55am: UofMich. Consumer Sentiment, Oct. final, est. 86.4 (prior 86.4)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Senate, House out of session

- President Obama gives speech on the economy

- Deadline for bids on Pentagon’s $11b electronic health records contract (for March 2015 award)

- 8:30am: Commerce Dept maunfacturing event; Deputy Commerce Secretary Bruce Andrews to speak at 11:45am

- U.S. ELECTION WRAP: Trouble With Polling; Ad Spending; Ratings

WHAT TO WATCH:

- Citigroup Legal Costs Jump $600m as FX Probes Accelerate

- Bank of Japan Boosts Record Stimulus as Abe Eyes Tax Rise

- Oil Set for Biggest Monthly Drop Since ’12 on Oversupply

- Russia Agrees to Terms With Ukraine for Gas Supply to Resume

- Trading in Xetra Is Suspended, Deutsche Boerse Says

- Ex-UBS Trader Defense Is Possible Threat to U.S. Forex Cases

- Android Co-Founder Rubin Leaving Google to Form Incubator

- Twitter Said to Appoint Head of Product as User Growth Slows

- Disaster Averted in NYSE Stocks as Price Feed Backup Kicks In

- Starbucks Sales Trail Estimates Amid U.S. Breakfast Rivalry

- LinkedIn New Businesses Lift 3rd-Quarter Sales Above Estimates

- Square’s Card-Reader Market Sway Slips as PayPal, Amazon Loom

- Alibaba Co-Founder Said to Back Hedge Fund of Ex SAC Trader

- BlackRock Says ETFs Aided Bond Mkt Stability After Gross Exit

- U.S. Midterm Elections, Jobs, ECB, BOE, AIG: Wk Ahead Nov. 1-8

EARNINGS:

- AbbVie (ABBV) 7:47am, $0.77 - Preview

- American Axle & Mfg (AXL) 8am, $0.62

- Aon (AON) 6:30am, $1.12

- CBOE (CBOE) 7:30am, $0.54

- Chevron (CVX) 8:30am, $2.52 - Preview

- Clorox (CLX) 8:30am, $1.03 - Preview

- CommScope (COMM) 7:30am, $0.57

- Dominion Resources (D) 7:30am, $0.95

- Exelis (XLS) 6:30am, $0.32

- Exxon Mobil (XOM) 8am, $1.71 - Preview

- Genesee & Wyoming (GWR) 6am, $1.18

- Hilton Worldwide (HLT) 6am, $0.17

- ITT (ITT) 7am, $0.60

- Legg Mason (LM) 7am, $0.01

- Madison Square Garden (MSG) 7:30am, $0.32

- Magellan Midstream Partners (MMP) 8:30am, $0.66

- Moog (MOG/A) 7:55am, $1.08

- Newell Rubbermaid (NWL) 6:30am, $0.55 - Preview

- NextEra Energy (NEE) 7:30am, $1.54

- Oshkosh (OSK) 7am, $0.82

- Pinnacle West Capital (PNW) 8:30am, $2.13

- Rockwell Collins (COL) 7:30am, $1.27

- Spirit AeroSystems (SPR) 7:30am, $0.77

- TECO Energy (TE) 7:30am, $0.33

- Telephone & Data Systems (TDS) 7:56am, ($0.08)

- United States Cellular (USM) 7:57am, ($0.30)

- Vantage Drilling (VTG) 6am, $0.02

- WisdomTree (WETF) 7am, $0.07

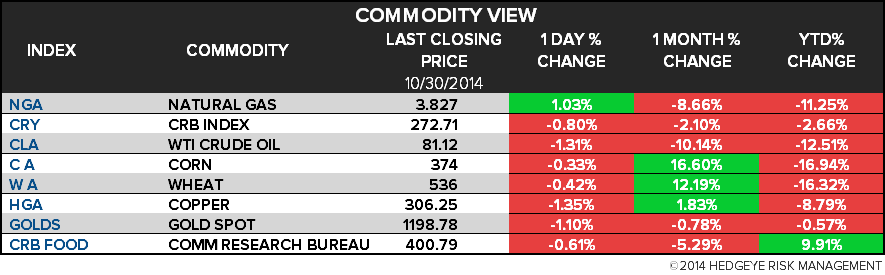

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Tumbles With Silver to Lowest Since 2010 as Dollar Advances

- Brent Oil Set for Longest Run of Weekly Losses Since ’02 on Glut

- Gold Slumping 17% to $1,000 an Ounce for SocGen on Oil’s Tumble

- Nickel Leads Gains by Industrial Metals as Japan Adds Stimulus

- No Guarantee Saudis to Repeat Price Cut That Drove Oil Lower

- Hurricane Season’s Eastern Pacific Finale Sends Storm to Mexico

- Shale Boom Redraws Oil Routes as Alaskans Ship to Korea: Energy

- Russia Agrees to Terms With Ukraine for Gas Supply to Resume

- Emerging-Market Currencies Hurt by Oil, Metals: Chart of the Day

- Wheat Futures Drop as Much as 1% to $5.305/bu, Reversing Gains

- Steel Rebar Pares Monthly Gain as Demand Seen Falling in Winter

- Freeport Indonesia, Labor Union Continue Talks on Planned Strike

- Copper Traders Bullish for Next Week Amid Distruption Prospects

- ‘Brouhaha’ Looming Over OPEC Oil-Production Cuts, Yergin Says

CURRENCIES

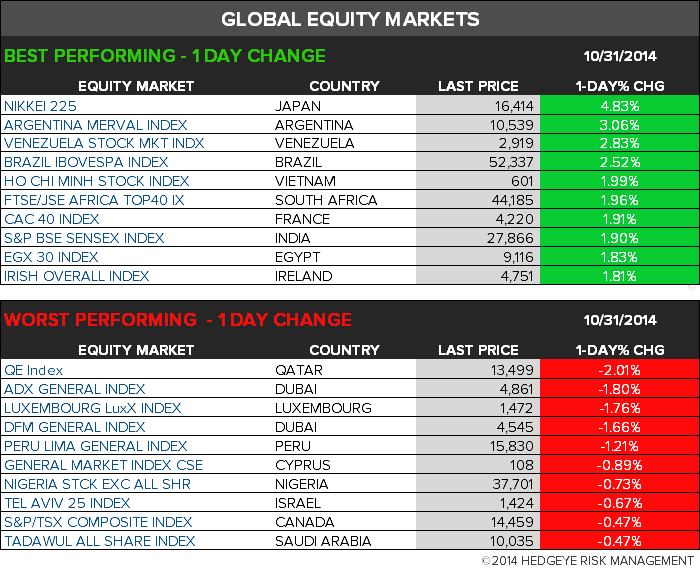

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team