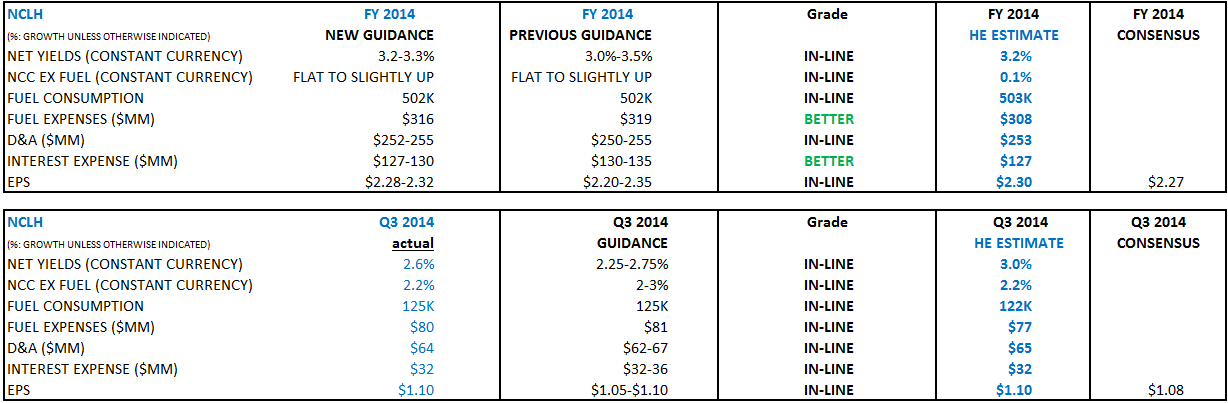

Positive commentary regarding 2015 $25m Prestige synergy target which we think is too conservative. Guidance for 4Q yields is above Street expectations.

CONF CALL

- 25th consecutive quarter of trailing EBITDA (TTM) growth; 23% CAGR

- Anticipate Prestige closing in mid-November; 4Q call will be first with integrated company

- Norwegian Escape: offering 7-day cruises beginning in Nov 2015

- Have set Ebola protocols across fleet; have seen impact on the margin over past several weeks however, booking have returned back to pre-Ebola levels.

- FX impacted 3Q by 2 cents; going forward impact will be similar in 4Q

- Made incremental investments in marketing in 3Q

- 4Q

- Drydock earlier than expected

- Work underway for scrubber installations; will have a number of staterooms out of service

- 2015 capacity: 59% in Caribbean, 17% in Europe, 5% Hawaii, 3% Bermuda

- 2015 Caribbean capacity: slightly down for the year;

- 1Q 2015: tougher comps (3.8% yield in 1Q 2014, two ship charters that did significantly well (Sochi/Bud Light Hotel)); volume will be consistent with 1Q 2014

- Investor Day in early February and will provide 2015 commentary

- In 2016 and afterwards, will report on consolidated basis

Q & A

- 2015: significantly more loaded on Getaway, Epic, and Breakaway in 1Q YoY. Well ahead on every quarter on load in the Caribbean. 1Q pricing is a little bit tough

- <1% industry capacity change in Caribbean in 1Q from 53% to 52.2%

- 1Q yield: could finish +1% yield (but would be difficult to achieve that given tough comps)

- Prestige synergy of $25m: is already in the bag; more opportunities ahead - port contracts, shore excursions, fuel

- Margin opportunity with Prestige? if economic picture gets a little better, could be another 500bps improvement

- 2015 Prestige: booked solidly; revenues up significantly, feeling some pressure in 1Q, same as Norwegian.

- Revenue opportunities with Pride of America and The Haven concept

- Shift of drydock impact on 4Q? $2-3m benefit

- 1Q 2013 charter contribution: a little over a 1% of growth

- Commissions/transportation/other line run rate: 15.5-16%; renegotiated port contracts, renegotiated credit card costs, more casino initiatives; more targeted incentive programs.

- MSC aggressive 'free-ship' offer: great brand in Europe

- Europe: pricing doing well in 2014 but because of carnage in 2012/2013; sees good pricing continuing.

- Asia: will be more interested in 2016