Selective disclosure

MGM’s Las Vegas properties clearly disappointed. Management points out in the press release that low table hold vs last year cost them $18m in EBITDA in Las Vegas. A few observations regarding that selective disclosure:

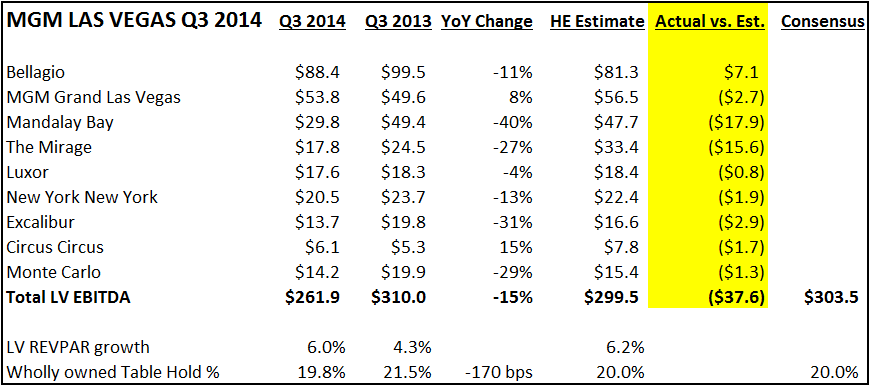

- Wholly owned Las Vegas EBITDA was $262 million in Q3 versus the Street at $304 million

- Table hold percentage at wholly owned casinos was 19.8%, almost exactly in the middle of management’s historical guidance of 18-22% (as discussed on conference calls and in 10Qs)

- Analysts typically model Las Vegas to normal hold, so the $42m Las Vegas EBITDA miss was apples to apples

- In Q2, wholly owned table hold % was 21.3% vs 18.1%, a 320bp delta. In Q3 it was 19.8% vs 21.5%, only a 170bp delta. Last quarter management didn’t emphasize that they got a huge boost from higher hold YoY nor did they quantify what would’ve been a much bigger delta than the slightly lower YoY hold experienced in Q3. In fact, we pointed out in a note last quarter that Las Vegas EBITDA would’ve been flat with normal hold in both periods. Here is what we wrote in our 8/5/14 note “MGM & MACAU OBSERVATIONS: NOT GOOD”:

- “MGM reported wholly owned adjusted EBITDA of $414 million, up 10% over last year. However, if you normalize hold in both periods, EBITDA was roughly flat. That seems disappointing to us given the excitement about a surging Las Vegas recovery and the solid RevPAR gain of 6% generated in the quarter.”

We still maintain that the Vegas recovery is concentrated in the hotel business and this past quarter was another indication that the Strip casino segment is stagnant. However, the hotel business nationwide is doing quite well and actually better than the mid-single digit Strip RevPAR gains.