KEY POINTS

- 3Q14 UPSIDE DRIVEN BY 2Q14 ACQUISITIONS?: TWTR beat consensus expectations for advertising revenues by only 2%; with y/y growth decelerating to 109% vs. 129% in the prior quarter (3Q14 also includes World Cup as well). Much of its 3Q14 upside came from its Data segment, which grew 171% y/y vs. 91% in 2Q14. It appears much of its guidance raise in 2Q14 may have been inorganic after all; we suspect this may become a recurring theme.

- 4Q14 GUIDANCE SUGGESTS AD LOAD WON’T BE ENOUGH. 4Q guidance suggests ad revenue growth will decelerate sharply from the 129% in 2Q14 to 88% in 4Q14. There’s nothing wrong with 88% growth, but such a sharp deceleration in such a short period suggests an unraveling of its monetization strategy (rising ad load), which creates a much tougher setup for the company moving forward.

- 2015 WILL BE A STRETCH (ORGANICALLY): We suspect the limitations of its monetization strategy will become more evident in 2015 as management struggles with balancing ad load vs. user growth. The 67% revenue growth consensus is assuming for 2015 will be a stretch organically. Acquisitions could fill the void, but will the street be willing to pay up for that? This morning's pre-market action suggests that won't be the case.

3Q14 UPSIDE DRIVEN BY 2Q14 ACQUISITIONS?

Advertising revenues grew 109% y/y; yet only beating street estimates by 2%. Note 3Q14 likely had some lingering benefit from ad campaigns around the World Cup, which essentially straddled 2Q14 and 3Q14 in terms of timing (June 12-July 13).

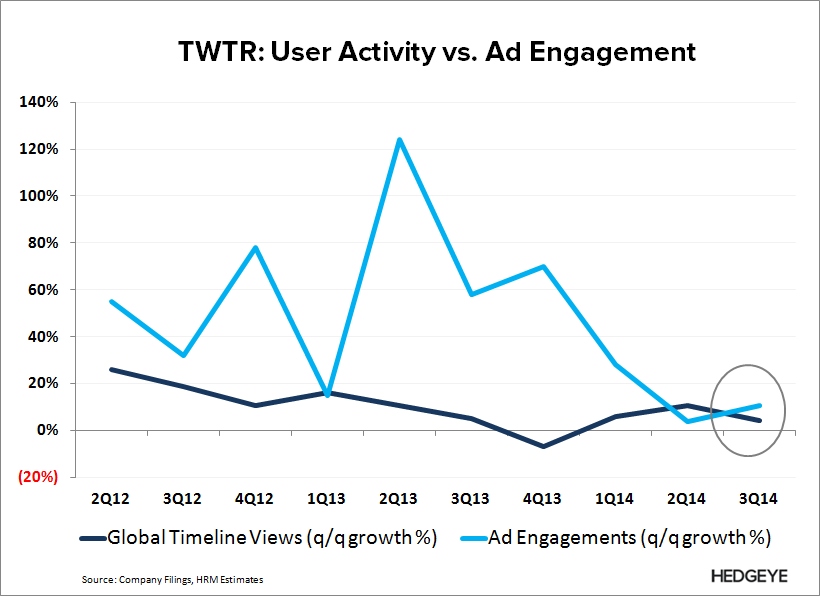

Still, the quarter was very strong. Ad engagements were up over 150% y/y; reversing the concerning inflection we saw in 2Q14 when the sequential change in ad engagements lagged that of global timeline views, which suggested users were fading TWTR ads at an increasing rate. However, that inflection wasn't particularly impressive, and it’s possible this dynamic is still occurring, but we just can’t see it in the data because TWTR may have increased ad load more than its ad engagement metrics suggest.

Data Licensing/Other Revenues accelerated sharply, up 171% y/y vs. 91% in the prior quarter. We don’t believe the street was prepared for that acceleration, which suggests much of its guidance raise from the prior quarter may have been tied to its recent string of acquisitions. Given that it just raised an additional $1.7 billion less than a year after its IPO, and now has $3.6B in cash and short-term investments, we suspect acquisitions may become a recurring theme moving forward. Question is why?

4Q14 GUIDANCE SUGGESTS AD LOAD WON’T BE ENOUGH

Management suggested that 4Q revenues will be up 28%-30% q/q in a seasonally strong quarter, which at the midpoint implies 88% growth y/y vs. 109% and 129% in 3Q14 and 2Q14, respectively. There’s nothing wrong with 88% growth, it’s the sharp deceleration from 2Q14 that’s concerning.

It’s interesting that 2H14 is when we’re seeing the slowdown in revenue growth. That may have to do with TWTR comping past what we refer to as the 2Q13 supply shock, which we suspect was a colossal surge in ad load given the 124% sequential increase in ad engagements that occurred during the quarter. Ad price and engagements are near perfectly inversely correlated (-.87 correlation since 2Q12), and we suspect this relationship suggests a supply-demand dynamic (we estimate ad engagements are a proxy for supply). We don’t believe it’s a coincidence that y/y ad revenue growth is slowing precipitously now that we’re a year past 2Q13.

If ad load has been the driver of its recent strength, then that puts management in a box. The street has been punishing the stock whenever its user metrics aren’t accelerating, so the company can’t risk increasing its ad load too much for fear of pushing the casual user away. Only ~50% of its MAUs use twitter daily, which means much of its user base is on the fringe. In short, there may be a perverse relationship between revenue and net user growth moving forward…Maybe this is why TWTR is raising capital.

2015 WILL BE A STRETCH (ORGANICALLY)

We suspect the limitations of TWTR's monetization strategy will become more evident in 2015 as management struggles with balancing ad load vs. user growth. Further, TWTR will be comping past the World Cup in 2Q15/3Q15, which we believe is an underappreciated headwind.

We believe the 67% revenue growth consensus is assuming for 2015 will be a stretch organically. User growth will naturally slow from here, while growth in automated accounts should continue to pressure engagement (timeline views/MAU). So the void must be filled by monetization, which is where we are seeing the most pressure across its model.

Acquisitions could potentially fill the void; we suspect this is why TWTR raised an additional $1.7B in capital when it already had roughly over $2.2B in cash and S/T investments on its balance sheet. This ads an extra level of risk being short into the 2015 guidance release, but the question is whether the street is willing to pay up for inorganic growth? TWTR's pre-market action this morning suggests that won't be the case.

Let us know if you have any questions, or would like to discuss in more detail. For additional detail on our thesis, see the two notes below.

Hesham Shaaban, CFA

@HedgeyeInternet

TWTR: Has the Story Changed?

09/17/14 08:51 AM EDT

http://app.hedgeye.com/feed_items/38023

TWTR: What the Street is Missing

05/19/14 09:09 AM EDT

http://app.hedgeye.com/feed_items/35420