TODAY’S S&P 500 SET-UP – October 24, 2014

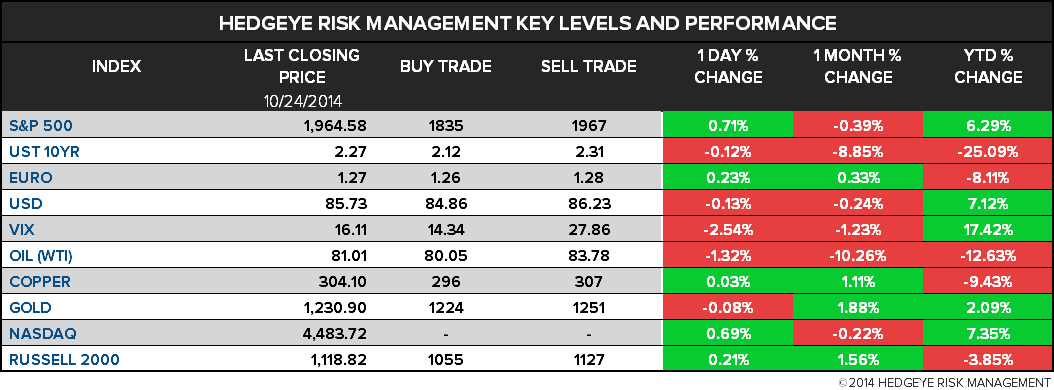

As we look at today's setup for the S&P 500, the range is 132 points or 6.60% downside to 1835 and 0.12% upside to 1967.

SECTOR PERFORMANCE

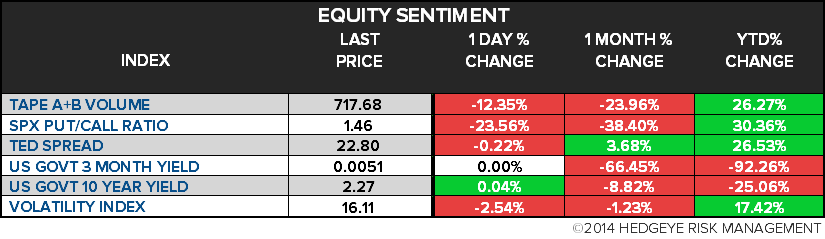

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.88 from 1.88

- VIX closed at 16.11 1 day percent change of -2.54%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:45am: Markit US Services PMI, Oct. prelim, 57.8 (prior 58.9)

- 10am: Pending Home Sales m/m, Sept., est. 1% (prior -1%)

- 10:30am: Dallas Fed Mfg Activity, Oct., est. 11 (prior 10.8)

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $24b 3M bills, $30b 6M bills

GOVERNMENT:

- U.S. authorities at airports in 6 states begin monitoring people coming from Liberia, Sierra Leone and Guinea for Ebola

- President Obama hosts Advanced Manufacturing Partnership steering cmte meeting at White House

WHAT TO WATCH:

- Williams Partners, Access Midstream Agree to Improved Terms

- ECB Fails 25 Banks in Test as Capital Hole Lurks in Italy

- Vodafone Starts Audit Into Possible Fraud at Ono Before Buy

- Venezuela Scraps Plans to Sell Citgo Petroleum, Universal Says

- Apple Pay Faces Challenge as CVS, Rite Aid Disable Payments

- U.S. Gasoline Declines to Lowest Since 2010, Lundberg Says

- Hedge Funds Pare Bullish Coffee Bets as Brazil Drought Eases

- Keystone Foes Energized as Tumbling Crude Pinches Oil Sands

- Horror Flick ‘Ouija’ Outdraws Assassin Movie Starring Reeves

- Rousseff Ready for Great Changes After Tight Brazil Victory

- CDC Moves Fast on NY Ebola as Soul-Searching Brings Changes

- BARRON’S ROUNDUP: Charles Schwab, Amazon, Coca-Cola, Aflac

AM EARNS:

- Allergan (AGN) 8am, $1.77 - Preview

- Armstrong World (AWI) 7am, $0.77

- Franklin Resources (BEN) 8:30am, $0.93

- Huntsman (HUN) 6am, $0.53

- Merck & Co (MRK) 7am, $0.88 - Preview

- Old National Bancorp (ONB) 9am, $0.25

- Precision Drilling (PD CN) 6am, C$0.17

- Roper Industries (ROP) 7am, $1.53

- Seagate Technology PLC (STX) 8am, $1.25 - Preview

- Tenneco (TEN) 8am, $1.08

PM EARNS:

- Allison Transmission (ALSN) 4:05pm, $0.30

- American Capital Agency (AGNC) 4:01pm, $0.73

- Amgen (AMGN) 4:02pm, $2.11 - Preview

- Amkor Technology (AMKR) 4:08pm, $0.24

- AvalonBay Communities (AVB) 4:05pm, $1.19

- Cliffs Natural (CLF) 4:30pm, $0.01

- Cognex (CGNX) 4:06pm, $0.56

- Compass Minerals Intl (CMP) 4:15pm, $0.81

- Crane (CR) 6:15pm, $1.17

- General Growth Properties (GGP) 4:01pm, $0.09

- Hartford Financial (HIG) 4:15pm, $0.83

- HealthSouth (HLS) 4:30pm, $0.49

- Integrated Device (IDTI) 4:05pm, $0.18

- Manitowoc (MTW) 4:25pm, $0.41

- Masco (MAS) 5pm, $0.32

- Owens & Minor (OMI) 5:08pm, $0.47

- PartnerRe (PRE) 4:15pm, $3.60

- Plum Creek Timber (PCL) 4:04pm, $0.30

- PMC-Sierra (PMCS) 4:05pm, $0.10

- Regal Entertainment (RGC) 4:01pm, $0.15

- T-Mobile (TMUS) 9pm, $0.05

- Twitter (TWTR) 4:08pm, $0.01

- Universal Health (UHS) 5:01pm, $1.34

- XL Plc (XL) 4:05pm, $0.62

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel Falls to Lowest Since March as Demand Concern Persists

- Commodities Drop to Five-Year Low Led by Sugar, Coffee on Brazil

- Hedge Funds Cut Coffee Bets as Brazil Drought Eases: Commodities

- Brent Oil Falls Second Day as Goldman Cuts Forecasts; WTI Slips

- Gold Trades Near 1-Week Low as Investors Weigh Stocks to Buying

- Sugar Falls on Speculation of Weaker Brazil Real; Coffee Drops

- Oil Speculators Bet Wrong as WTI Rebound Proves Fleeting: Energy

- Corn Falls With Soybeans as Drier Weather Seen Aiding U.S. Crop

- Rebar Extends Weekly Loss on Speculation of Slowing China Demand

- Goldman Cuts Oil Forecasts as OPEC Loses Influence to U.S.

- Trade Negotiators Say Balanced TPP Deal Is ‘Crystallizing’

- BlueScope Sees China Steel Demand Growth in Decline, AFR Says

- Thai Farmers Fret Over Survival as Sluices Shut: Southeast Asia

- China Gold Imports Rise to Five-Month High Before Holiday Sales

CURRENCIES

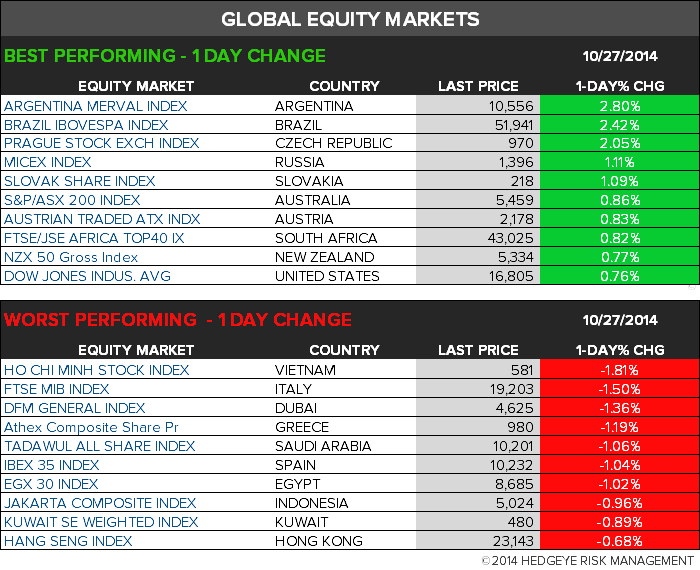

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team