This note was originally published October 23, 2014 at 07:18 in Retail

Conclusion: Target offering free shipping over the holidays accelerates a trend that we think will play out over two years -- which is that almost all retailers offer free shipping and free returns. Only those with the highest basket size (Nordstrom) can win at this game. Other retailers are likely to follow TGT over the near term. The math does not look good.

DETAILS

Every year there seems to be a new strategy the retailers embrace to gain share of wallet as the Holiday's approach. With many stores now open all day on Thanksgiving and staying open 24/7 in the final stretch in December, there's not much more (aside from price) that the retailers can do to get more people to shop at the stores. But Target has an interesting, albeit costly, idea.

TGT is offering free shipping on all items in the store for online customers beginning yesterday, and lasting through Dec 20th. This is a huge event for retail -- at least how we see it. And it does not result in profitability going up, unfortunately.

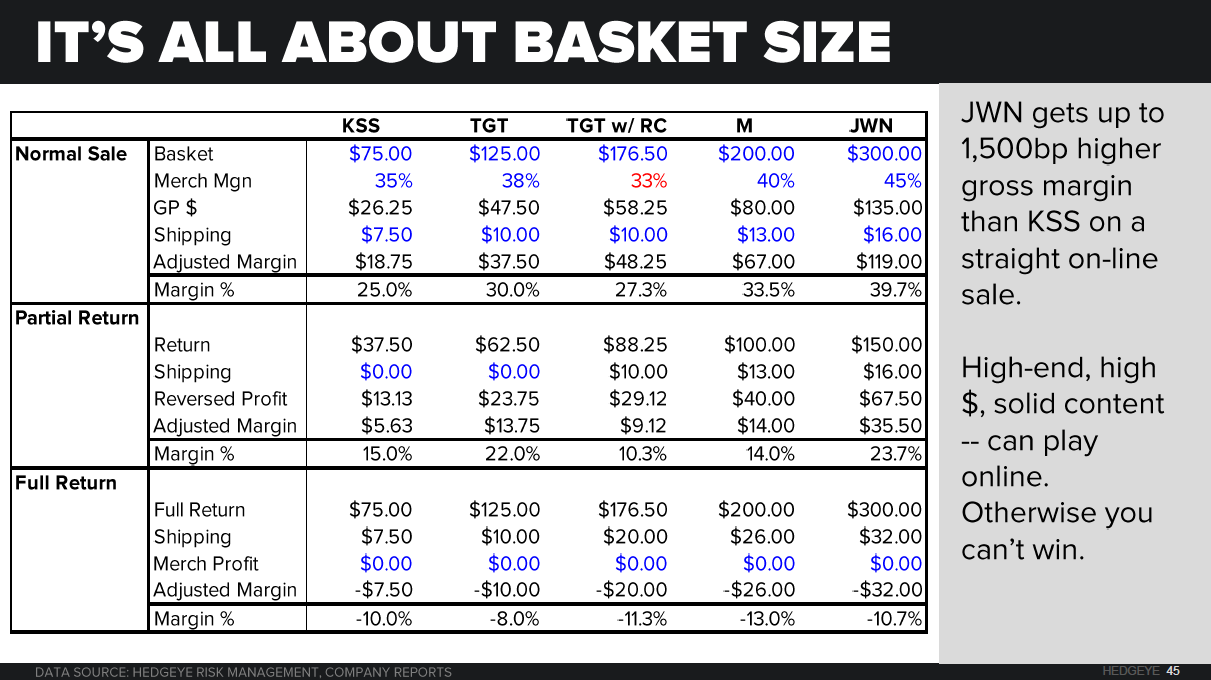

Common perception is that e-commerce margins are higher than brick & mortar. That might be true for content owners like Ralph Lauren, Nike and UnderArmour -- who can side step a wholesaler and capture 100% of the margin. But for retailers like Target, Macy's, Kohl's and JC Penney, e-commerce is not margin accretive.

Take KSS, for example. It's e-commerce gross margins are about 25% -- 1,200 basis points below the company average. The big culprit is the triangulation of lower-value (commodity) product, low basket size, and fixed shipping costs.

In the example below, you can see that a company like Nordstrom, which is the only retailer that offers free shipping and free returns, has a big enough basket size due to very defendable brands and price/points such that it can still print a superior e-commerce gross margin. Other retailers -- even Macy's, which is known for being a trailblazer in e-commerce (we don't particularly agree) has an extremely high threshold for free shipping ($99), and still does not have a superior e-commerce margin.

Our concern about this move by TGT is that it currently has a $50 'free shipping' threshold. Over the next two months, if you want to buy a package of q-tips for $3.89, or a package of pacifiers for $5.89, you get them delivered for free. Unfortunately, the shipping cost on those items is about double the gross profit that Target would otherwise record.

Another angle on shipping costs is that a by-product of a 'free shipping' threshold is that it causes many consumers with a low basket size to come in to the store to pick up the product to avoid a $5-$10 shipping charge. According to Target, 14% of its digital sales are picked up in stores, and then about 20% of those customers buy additional items. What happens now that shipping is free?

We're not as concerned about this event as a negative for Target, but we are definitely concerned that (almost) all retailers are gravitating to a very unprofitable place -- that's free shipping and free returns. Free shipping is kind of like a dividend -- once you give it, you really can't take it away without severe repercussions.