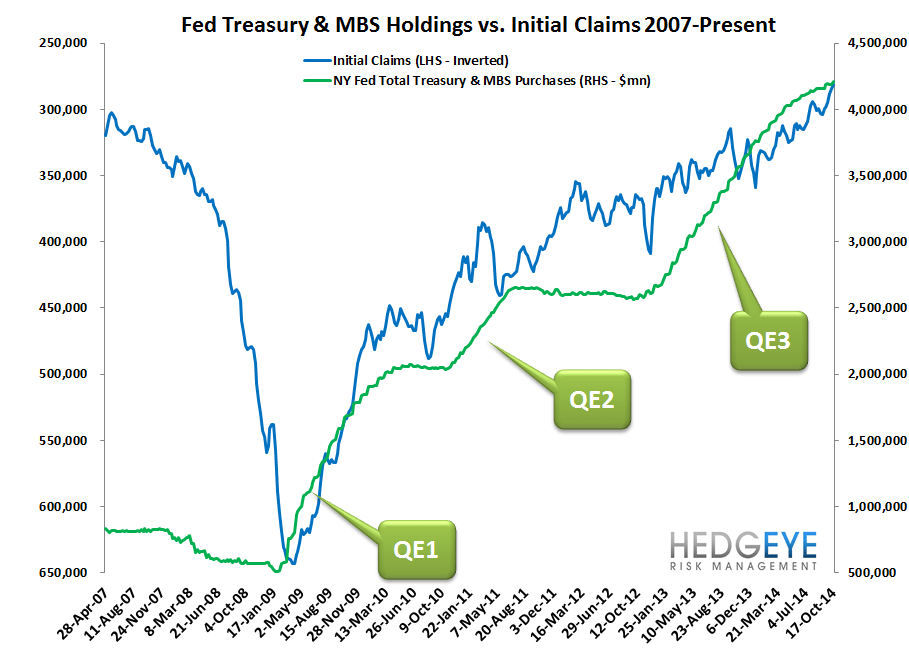

Labor and Credit, Together, Tell the Whole Story

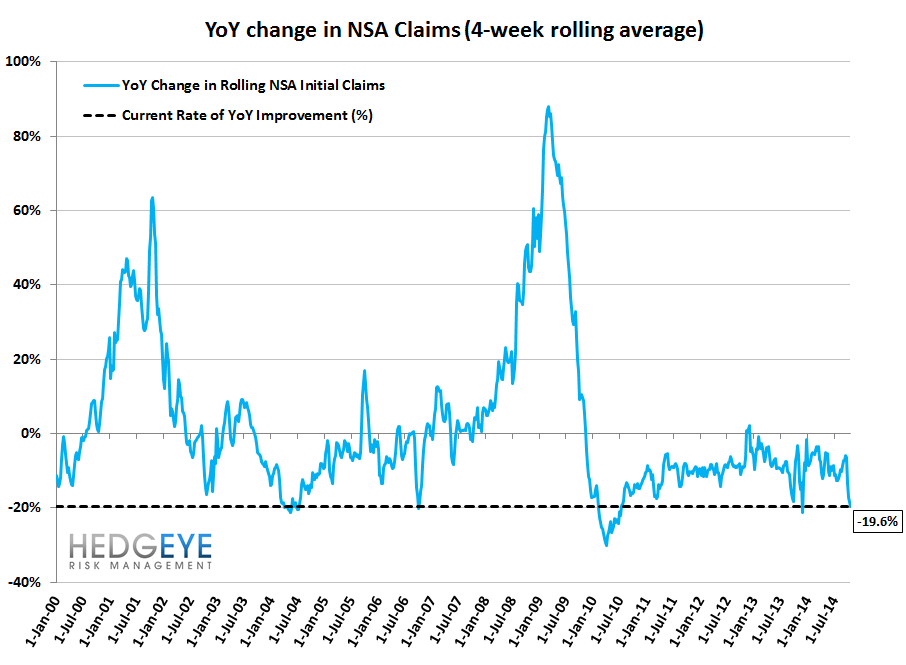

The improvement in the jobless claims series continues unabated. This week rolling SA claims dropped to a new low of 281k - for perspective that's now lower than at any point in the peak of the economic expansion in 2005/2006. Meanwhile, our gauge of rate of change looks at the y/y change in the rolling NSA claims, which also accelerated to its fastest rate YTD at -19.6%.

While there are many macro-level factors that have us cautious, labor is the one thing steadying the ship in the storm. The credit cycle and the labor market are reflexive meaning that they interactively affect each other simultaneously. Labor remains strong, and we should receive the next quarterly installment of the Fed's senior loan officer survey in the coming weeks, which will give us the latest update on the outlook for credit. With that in hand, we should be able to move forward with greater confidence, one way or the other. We've found that the C&I survey has effectively predicted every major downturn well in advance going back to the inception of the survey.

The Data

Prior to revision, initial jobless claims rose 19k to 283k from 264k WoW, as the prior week's number was revised up by 2k to 266k.

The headline (unrevised) number shows claims were higher by 17k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -3k WoW to 281k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -19.6% lower YoY, which is a sequential improvement versus the previous week's YoY change of -17.1%

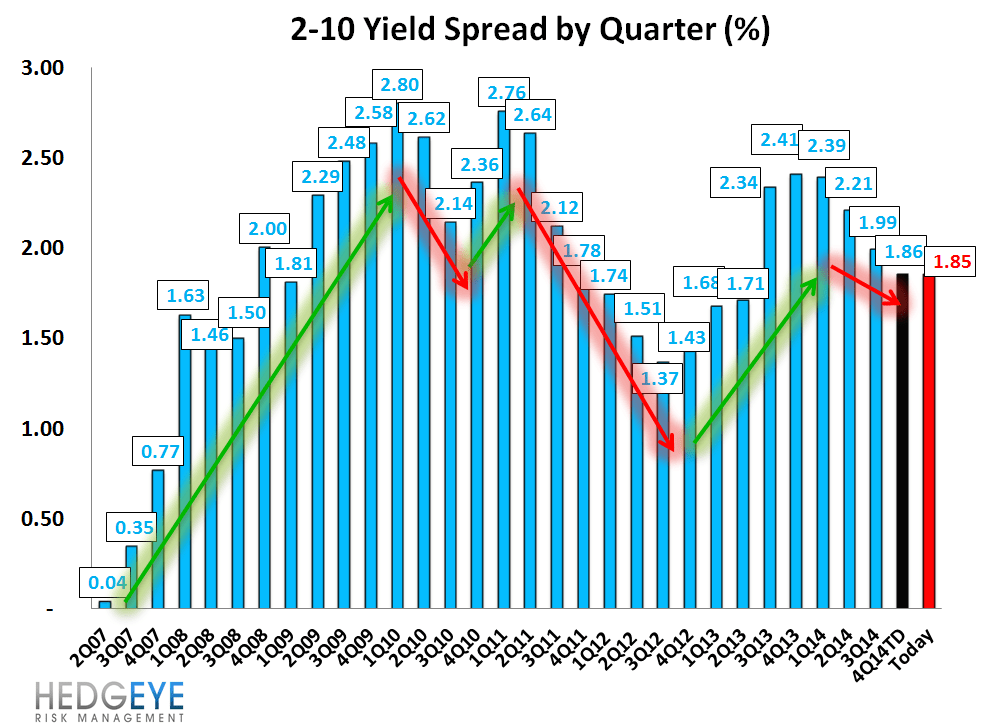

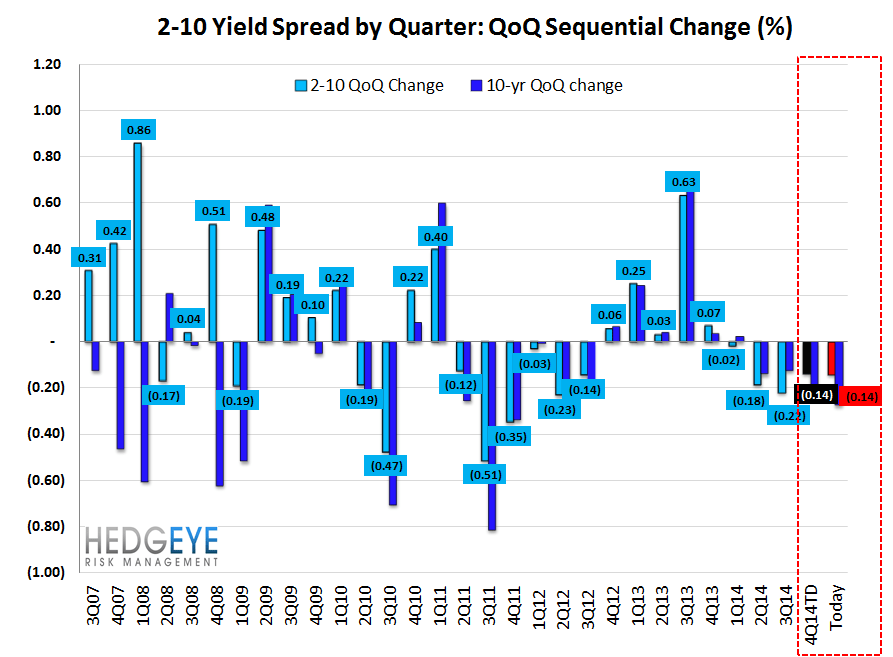

Yield Spreads

The 2-10 spread rose 2 basis points WoW to 185 bps. 4Q14TD, the 2-10 spread is averaging 186 bps, which is lower by -14 bps relative to 3Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT