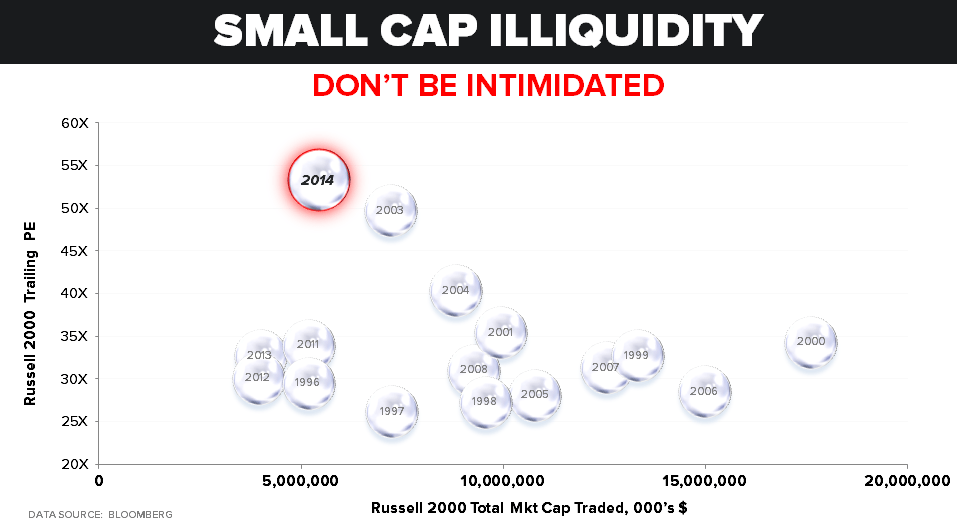

“We will not be intimidated.”

-Stephen Harper

I drove up to Maine in the rain yesterday. My ride was a metaphor for macro markets in the last six weeks. I got in the car in the late morning – equities were up, on decelerating volume. There was a faint bid to European equities and Oil. There was some low-conviction selling in the bond market too.

“So”… I did the opposite (in Real Time Alerts) – going right back to our #Quad4 playbook, sending out buy signals in Munis (MUB) and sell signals in stocks with energy price related risks (MLPs like Linn Energy, LNCO). #Bubbles that bounce to lower-highs on no volume don’t intimidate me.

As I drove through New Hampshire in the early afternoon, the US equity markets picked up on the intraday drop in oil prices – and bonds caught a bid. I flipped through a few of the manic media’s channels – they all blamed Canada.

Back to the Global Macro Grind…

While it would be nice if we could boil down intraday, weekly, and monthly macro market moves to a single factor like ebola or Canada, that is not how a non-linear and interconnected ecosystem (the market) works.

That’s why we spend so much time grinding through both multi-factor and multi-duration analysis. We will not write to you about risks in the rear-view. We will not be whipped around by newsy headlines either. Our Global Macro risk management process will not be intimidated.

There’s a great complexity theory quote in the WWII #history book I am in the middle of reading that summarizes how the American, British, and Canadian men acted when storming the beaches of Normandy on June 6th, 1944:

“Beset by mischance, confounded by disorder, they had mostly done what they were asked to do.”

-Rick Atkinson, The Guns At Last Light (pg 53)

And while I try to not feel anything when communicating #timing decisions in markets, I do want our analytical troops to feel confident that, instead of being glued to the screens and emotions of the moment, they can do what they were trained to do. #Process

To be clear, the process is dynamic and flexible. That means that if the economic facts and/or market read-throughs change, we are both equipped and tasked to change alongside those changing factors. If they don’t change, we double down on the #process.

In asset allocation terms, here’s what we did (before the morning part of that drive!) yesterday:

- CASH – took it down small, deploying assets to a region of the market that likes #Quad4 (Municipal Bonds – MUB)

- FIXED INCOME – took it up, in kind, to a 26% allocation (which is 78% of what I consider my max, 33%, to any asset class)

- EQUITIES – stayed the course with the “net zero” exposure, adding to the bear side of energy related shorts like LNCO

For those of you who are new to reading my rants, the Hedgeye Asset Allocation Model is basically like my p.a. (personal account). It’s not what a long-only fund with a mandate to be fully invested has to do. It’s not a hedge fund either. It’s simply what I would do with my money - not being intimidated!

“So”, when I say “net zero” that means that if I had to be in something like US Equities, at a minimum, I’d hedge (with alpha oriented shorts) out the market risk and have a beta-adjusted net exposure to that asset class of 0%.

That’s why, on the morning of October 17th, in the Early Look you saw an asset allocation to US Equities of +3%. After a stiff selloff, I signaled “buy” in #RealTimeAlerts in 1 of the 2 S&P Sectors that are LONGS in our #Quad4 playbook – Consumer Staples (XLP). Then I took us back to net zero, on the bounce.

I know. It’s not easy trying to communicate a process that the Old Wall doesn’t use.

Commercializing how I think about risk has been as much a communication learning process for me as it has been for those of you trying to learn it alongside me. I appreciate your open-mindedness. These are still the early days of our changing parts of a profession that needs changing.

Back to what is really crushing market expectations (it’s not Canada – it’s #Quad4 deflation):

- Oil prices got smoked for another -2.8% loss yesterday, taking WTI to down -18.2% YTD

- Bullish to Bearish Phase Transitions in both Energy prices and their related stocks/bonds is #on because Oil is crashing

- Alongside a -25% drop in WTI Crude since June, the Russian stock market has crashed (-25.8% YTD)

That’s also why the Canadian Stock Market (TSX) went from bullish to bearish TREND @Hedgeye. Not because some whacko loser started killing people in Ottawa yesterday. In chaos (or complexity theory) speak, that was simply the grain of sand that knocked over the interconnected sand-pile.

In our playbook, terrorism doesn’t have a quadrant; #deflation does. If our quantitative signal is right, and the price of oil remains in an intermediate-term TREND risk range of $64.67-86.11:

- Both Oil & Gas (XOP) and Energy (XLE) related equities are going to be bearish TREND

- MLP related stocks and bonds are going to start discounting distribution (dividend) cuts

- Kevin “The Bear” Kaiser is going to look really right on his Best Short Ideas!

Instead of listening to more than 3 minutes of market spew on the radio yesterday, on that same drive up to Maine’s coast, I smoked a cigar (don’t tell my wife!) and listened to Kaiser’s Institutional Research call on MLPs from 1-2PM. It was awesome.

And I’m not just saying that because the man is on my team. I am telling you what it is to hear a world class analyst not be intimidated by institutional group-think and stay with a fundamental call that companies who don’t have the cash flow to pay out future promises are shorts.

Stocks that he doesn’t like (VNR, LNCO, etc.) got hammered intraday. If you’d like access to the replay of his call and 40 slide deck, please ping .

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.09-2.34%

SPX 1

RUT 1037-1119

VIX 15.09-28.26

WTI Oil 79.43-82.63

Natural Gas 3.59-3.79

Best of luck out there today,

KM