note summary

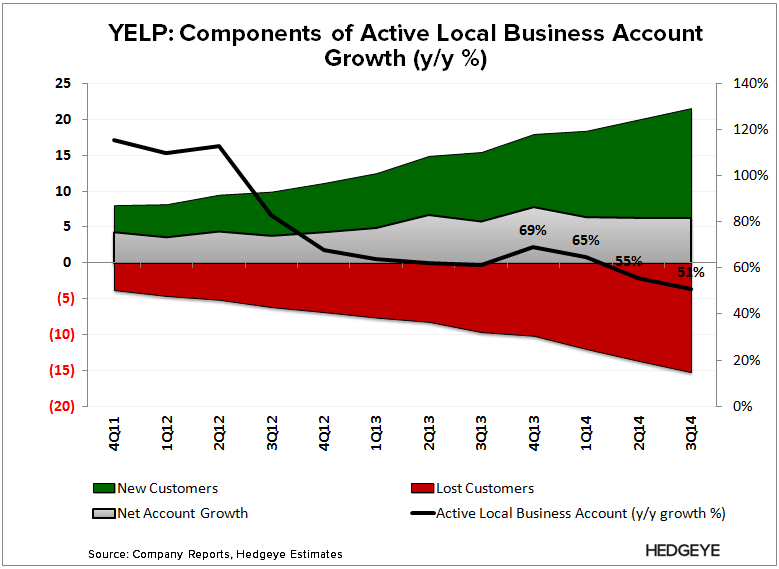

- 3Q14 BEAT, BUT UNIMPRESSIVE: Much of the upside came on a surprise surge in its Other Revenue Segment. YELP’s core Local Advertising segment missed expectations on its highest attrition rate since 4Q12. Despite some noise around some misleading metrics, 3Q14 pointed to further deterioration in its core account metrics

- 4Q14 GUIDANCE WORSE THAN THE MISS: Aside from guiding below street estimates, YELP provided segment-specific guidance on the smaller two of its three segments (<20% of revenue). From there, we can estimate that guidance implies its core Local Advertising revenue growth decelerates from 66% in 3Q14 to 57% in 4Q14

- 2015 WILL BE A DISASTER: YELP’s business model is breaking down, which is most evident in new account growth that can’t keep pace with the growth in sales rep hires. That means hiring more bodies can no longer sufficiently compensate for its attrition issues, and unless you understand that element of the story, you really can’t understand how bad 2015 will be.

3Q14 BEAT, BUT UNIMPRESSIVE

- Local Advertising Came in Light, Despite the Beat: The beat came from YELP’s Other Revenue segment, which grew over 150% y/y ($4M q/q), and was largely driven by its new partnership with YP.com. However, Other Revenues are expected to decline next quarter. Local Advertising missed street expectations, as attrition continued to accelerate. Absolute attrition levels continued to rise, which is to be expected simply because it has more accounts. However, it attrition rate of 19.1% was at its highest level since 4Q12.

- More Noise, No Substance: The customer repeat rate was 75%, same as the prior two quarters, and a historical high. Remember this is a measure of MIX, not retention. Also, management stated that its non-deal account growth grew 66% y/y vs. the 51% in Active Local Business Account (ALBA) growth. However, note that this metric includes SeatMe, which had very few accounts when YELP acquired it late in 3Q13. The better question is what its ALBA growth was ex-SeatMe?

4Q14 GUIDANCE WORSE THAN THE MISS

During the call, management provided segment-specific guidance on the smaller two of its three segments (<20% of revenue). From there, we can estimate that guidance implies its core Local Advertising revenue growth decelerates from 66% in 3Q14 to 57% in 4Q14. Management mentioned a challenging 4Q14 comp from the migration of int’l accounts from its Qype acquisition back in 4Q13. While this is notable headwind for account growth, it is a disproportionally smaller headwind in terms of revenue growth since international is lower ARPU product. In short, the weakness is much more than just Qype.

2015 WILL BE A DISASTER

YELP’s business model is predicated on aggressive sales rep hires to offset its rampant attrition. New account growth is failing to keep pace with its growth in sales rep hires, which means its model is broken, and it only gets worse from here.

Consensus estimates for 2015 remain outside the realm of reason. Their mistake is simple: If you don’t understand the attrition element to the story, you can’t understand the excessive number of new accounts required to hit 2015 estimates. YELP will need to produce both accelerating new account growth and historically low attrition to hit consensus estimates, which are calling for 46% revenue growth.

We expect estimates to come in moderately post the print, but likely not enough. Our bull case is calling for 32%; bear case for 23%.

Let us know if you have any questions, or would like to discuss further.

Hesham Shaaban, CFA