This note was originally published at 8am on October 08, 2014 for Hedgeye subscribers.

“History is just one thing after another.”

I’m not sure who the attribution for the above quote goes to, but it does offer a nice little existential change of pace for the early AM global macro hombres.

The macro practitioners’ grind is just one data point and price tick after another.

If we’ve successfully employed our “communication tool” over the last six years, you’re gainfully aware that, at its core, our macro process operates as a hybrid model with our fundamental macroeconomic research dynamically informing our quantitative view of markets.

Reciprocally, as my colleague Darius Dale highlighted yesterday, we apply those top-down quantitative signals – which often front-run reported fundamental inflections - in a reflexive manner to our bottom-up qualitative analysis (e.g. our Growth/Inflation/Policy framework) in order to generate actionable investment ideas and themes.

Most of the time the fundamental and the quantitative are in accord, or harmonize on a small lag.

More rarely, the incongruency persists for an extended period. In those instances we default to the price/quantitative signal – in recognition that market prices are real-time leading indicators and that the market and the economy are not the same thing, particularly over shorter durations.

Theoretically, corporate earnings should reflect economic growth with the high end of sustainable earnings growth capped at potential GDP and the value of the stock market reflecting GDP, corporate earnings as % of that GDP, and the multiple investor’s put on those earnings. But that certainly doesn’t hold in the short run and it’s only approximately true over the long-term.

It’s the conflation of perceived fundamental trends into a convicted market call where economists turned strategists most often go awry.

Back to the Global Macro Grind…

In covering the domestic macro economy, the quasi-persistent discontinuity between the research (fundamental) and the risk management (quantitative) signals has been my reality for the last couple months.

Juxtaposing the current domestic labor market data (positive) against the prevailing price signals (bearish) provides a timely and tangible case study:

INITIAL CLAIMS: Rolling Initial Jobless Claims were just under 295K in the latest week, matching the best levels of the post-recession period. As we’ve highlighted, over the last two cycles rolling SA claims have run sub-330k for 45 and 31 months, respectively, before the corresponding market peaks in March, 2000 and October, 2007. We are currently in month seven at the sub-330K level in the present cycle. Further, over the last half century, the trough in initial claims has led the peak in equities and the peak in the economic cycle by 3 and 7 months, respectively. At present, we are still putting in the trough – with cycle precedents suggesting the economic peak is not yet imminent.

NFP: Monthly NFP gains have been solid on balance and, due to seasonal artifacts, even sequential slowdowns in net monthly payroll gains have been characterized by flat to rising employment growth on a year-over-year and 2Y average growth basis. At +1.93% YoY in September, Nonfarm Payrolls recorded their fastest rate of improvement since April 2006 and are in-line with peak growth in the last cycle. Similar to initial claims, peak monthly NFP gains lead the economic cycle by ~7 months. Whether the May-July NFP gains represented peak improvement remains to be seen.

JOLTS: Total Job Openings made a new 13 year high and the quits rate held at cycle highs in the August report released yesterday. Total hires moderated sequentially alongside the dip in NFP gains reported for August but is likely to re-accelerate to new highs in the September release. Historically, the Job Openings data leads accelerations in wage growth by about a year. The relationship has been muted vs previous cycles but with the NFIB’s compensation index making new highs, the share of short-term unemployed continuing to rise and labor supply (total available workers per job opening) tightening to pre-recession averages, wage inflationary pressures are percolating.

INCOME: The confluence of an accelerating employment base and flattish wage growth has driven an acceleration in disposable personal income growth over the last 5 months. Indeed, aggregate private sector salary & wage growth is currently running at +5.8% and holding at its best levels of the recovery outside of the peri-fiscal cliff period.

CREDIT: Consumer revolving credit declined at a -0.3% annualized pace in August according to Federal Reserve data released yesterday. The sequential decline wasn’t particularly surprising given the comps (the increase in July was the 2nd largest in 6.5 years) and the already reported retreat in spending on durable goods ex-defense and aircraft (ie. the stuff the average household buys). On a year-over-year basis, growth in credit card spending decelerated just -5bps from the 6 year high recorded in July.

In a Keynesian economy, total spending is cardinal, and income and credit is predominate. You can spend what you make (income) and you can spend what you don’t make (credit) and, with both income and credit accelerating presently, the underlying trends in both are positive.

The caveat has been that while the capacity for consumption growth has improved alongside accelerating income growth, actual household spending has not because the savings rate has shown a commensurate increase.

So, while reported consumption growth remains middling, it’s hard to characterize accelerating income growth, a rising savings rate and moderate credit growth alongside increased investment as fundamentally negative.

Transitioning to the price signals, which paint a contrasting picture for the prospects of forward growth. Keith has hit the boards hard in highlighting these, but to briefly review:

10Y Yields: 10Y bond Yields are down -69 bps YTD (-23%), the yield spread (10’s-2’s) continue to compress and inflation expectations are collapsing – all of which are discretely bearish growth signals.

Russell 2K: The Russell is down -7.5% YTD with the rotation out of growth style factors and small Cap Illiquidity accelerating over the last month+ - again, not a growth-accelerating signal . The Russell 2000 is immediate-term TRADE oversold around 1076, but remains in a Bearish Formation.

Consumer: The XLY is the worst performing sector YTD (-1.84%), underperforming the S&P500 by 6% as real median income growth continues to trend negative and the bottom 60% remain very much income constrained. Also in Bearish Formation.

Housing: The ITB is down -9.1% YTD with housing sitting as one of the worst performing asset classes globally. We have been bearish on housing since the end of 2013 and continue to believe housing related equities underperform, trading sideways-to-down, alongside ongoing deceleration in HPI trends.

ROW: The EU and Japan are in discrete deceleration, China is not an upside catalyst, EM markets are flagging alongside dollar strength and the US is already past the mean duration of expansions over the last century. The IMF marked its (still too optimistic) global growth forecast lower yesterday and growth estimate revision trends over the last quarter across both developed and EM markets have been almost universally negative. Further, the disinflationary trends prevailing globally only add to the Feds Sisyphean fight towards sustained, above target CPI and core PCE inflation.

From a Hedgeye modeling perspective we are entering Quad #4 which is characterized by both growth and inflation slowing from a 2nd derivative perspective and a generally dovish policy response. A sequential slowdown in GDP in 3Q14 from the near 5% in 2Q14 is almost as inevitable as the sequential acceleration from the worst post-war expansionary period GDP print ever in 1Q14. Whether that manifests into a protracted slowdown domestically remains TBD.

Markets are discounting an increasing probability of a more enduring deceleration and are, at the least, refuting consensus’ laughably linear straight-lining of 3% growth into perpetuity.

May the wind be always at your back.

May the sun shine warm upon your face.

May your fundamental and quantitative signals always be in accord.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.35-2.46%

RUT 1072-1100

DAX 9026-9367

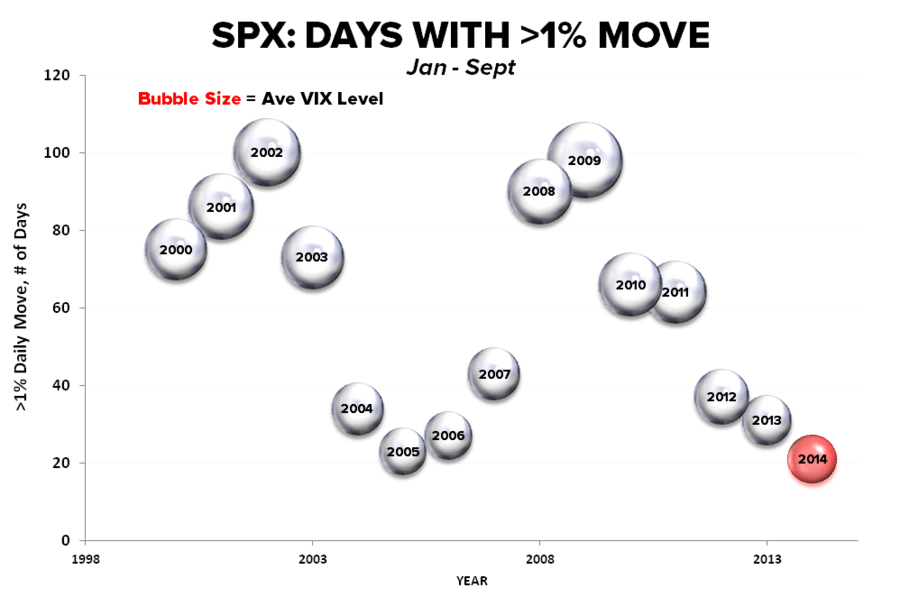

VIX 15.67-17.58

USD 85.05-86.64

WTI Oil 86.92-91.39

To cognitive dissonance, its ubiquity and successful management,

Christian B. Drake

Macro Analyst