MCD is scheduled to report August comparable sales tomorrow.

U.S. (facing a 4.5% comparison from last year)

Good: +3.5% or better would signal that the company is maintaining its 4%-plus 2-year average trend. If the number comes in at 5% or better, it would point to a sequential acceleration in 2- year trends from July.

Neutral: +2.5% to +3.5% would signal a sequential slowdown in 2-year average trends from July, but would point to trends that are still better than what we saw in June. July 2-year average trends improved 185 bps on a sequential basis from June.

Bad: < +2.5% would signal a return to the May and June 2-year average trend levels. Anything below +1% would signal a slowdown even from the already depressed June level.

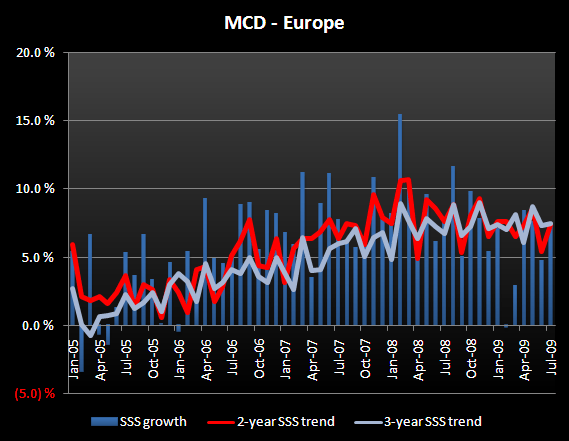

Europe (facing a difficult 11.6% comparison from last year)

Good: +4.0% or better would signal an acceleration in 2-year average trends. A number better than 4.4% would represent an 8%-plus 2-year average trend.

Neutral: +2.0% to +4.0% would signal that the company is maintaining its 2-year average trend from July.

Bad: < +2.0% would point to a sequential slowdown in 2-year average trends from July. Although a 2% number would still represent 6%-plus 2-year trends, investors are accustomed to 5%-plus reported numbers on a 1-year basis so a number below 2% would be alarming. A result worse than flat YOY performance would signal a return to June levels.

APMEA (facing a difficult 10.0% comparison from last year)

Good: +3.0% or better would signal an improvement in 2-year average trends on a sequential basis from July. Anything better than 4% would represent a return to 7%-plus 2-year average trend levels.

Neutral: +1.0% to +3.0% would signal an acceleration from June and July 2-year average trend levels, which had slowed rather significantly from prior months.

Bad: < +1% - A flat to +1% result would still signal a slight acceleration in 2-year average trends from June and July, but like Europe, I think a number below 1% on a 1-year basis would be alarming to investors that are accustomed to 5%-plus results out of the APMEA segment. A reported -0.5% to -1% would point to 2-year average trends that are similar to the already slowed trends in June and July.