TODAY’S S&P 500 SET-UP – October 21, 2014

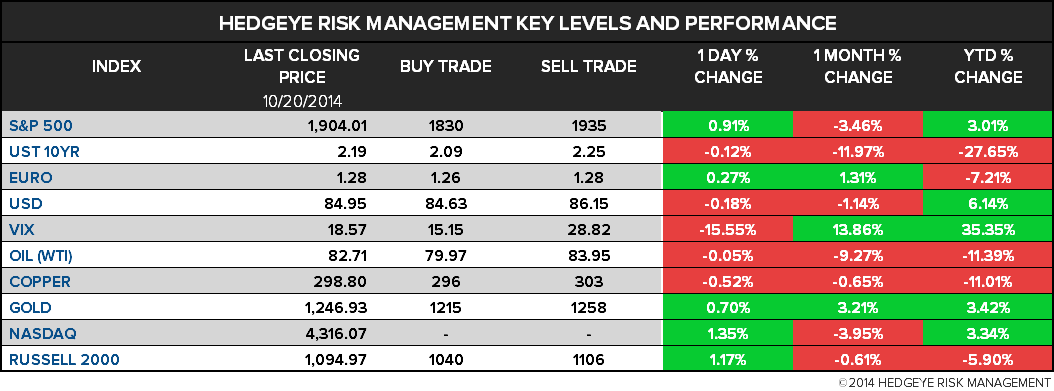

As we look at today's setup for the S&P 500, the range is 105 points or 3.89% downside to 1830 and 1.63% upside to 1935.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.85 from 1.84

- VIX closed at 18.57 1 day percent change of -15.55%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:55am: Redbook weekly sales

- 10am: Existing Home Sales, Sept., est. 5.10m (prior 5.05m)

- 11:30am: U.S. to auction 4W bills

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- Senate, House out of session

- Sec. of State John Kerry travels to Berlin

- 10:30am: American Petroleum Institute media briefing

- 11am: Foreign Policy Initiative briefing call on Ebola policy

- 11:30am: Michael Lewis speaks at Mortgage Bankers Assn

- 12pm: Gov. Chris Christie, R-N.J., speaks at U.S. Chamber of Commerce’s Legal Reform Summit

- 12:15pm: SEC examinations dir. Drew Bowden luncheon interview at Natl Society of Compliance Professionals conf.

- U.S. ELECTION WRAP: Comparing Sen. Models; Fundraising Reports

WHAT TO WATCH:

- Total CEO De Margerie Dies in Moscow Plane Crash

- Actavis Said to Bid for Omega Pharma Joining Sanofi, Perrigo

- AbbVie Scraps $52 Billion Shire Deal on U.S. Tax Changes

- Paulson Said to Urge Shire-Allergan Merger as AbbVie Talks End

- Apple’s Forecast for Holiday Quarter Tops Analyst Estimates

- Texas Instruments Quarterly Profit Outlook Exceeds Estimates

- Staples Says It’s Probing Potential Customer Credit-Card Breach

- Yahoo Said to Be in Talks to Buy BrightRoll: TechCrunch

- Tudor’s Jones Said to See U.S. Stocks Beating Globe Rest of Year

- China’s GDP Growth Bolsters Case for Stimulus Restraint

- Guardrail Maker’s Faulty Secret Changes Cheated U.S. Government

- Pimco’s Former Parent Pacific Life Switching Accounts to Janus

- FBI Warns of Hacks by Moonlighting Foreign Government Agents

- Dudley Warns Banks to Fix Culture or Be ‘Dramatically Downsized’

AM EARNS:

- Allegheny Technologies (ATI) 7:30am, ($0.06)

- AO Smith (AOS) 7am, $0.57

- Apollo Education (APOL) 7:30am, $0.27

- Brinker Intl (EAT) 7:45am, $0.50

- Canadian Pacific Railway (CP CN) 7:30am, C$2.36 - Preview

- Carlisle Cos. (CSL) 6am, $1.22

- Coca-Cola (KO) 7:30am, $0.53 - Preview

- Graphic Packaging (GPK) 7:30am, $0.20

- Harley-Davidson (HOG) 7am, $0.59

- Illinois Tool Works (ITW) 8am, $1.23

- Kimberly-Clark (KMB) 7:30am, $1.54

- Lexmark Intl (LXK) 6:30am, $0.91

- Lockheed Martin (LMT) 7:25am, $2.72 - Preview

- Manpowergroup (MAN) 7:30am, $1.50

- McDonald’s (MCD) 7:58am, $1.37 - Preview

- Omnicom Group (OMC) 7am, $0.90

- Pentair (PNR) 7am, $0.94

- Regions Financial (RF) 6am, $0.21

- Reynolds American (RAI) 6:58am, $0.91 - Preview

- Synovus Financial (SNV) 7:47am, $0.37

- Travelers (TRV) 6:57am, $2.26

- United Technologies (UTX) 6:59am, $1.81 - Preview

- Verizon Communications (VZ) 7:30am, $0.90 - Preview

- Waters (WAT) 7am, $1.29

PM EARNS:

- ACE (ACE) 4:05pm, $2.33

- Broadcom (BRCM) 4:05pm, $0.84

- Canadian Natl Railway (CNR CN) 4:01pm, C$1.05 - Preview

- Celestica (CLS CN) 4pm, $0.24

- Cree (CREE) 4:01pm, $0.34

- Cubist Pharmaceuticals (CBST) 4pm, $0.08 - Preview

- Discover Finl Services (DFS) 4:05pm, $1.34

- E*TRADE Financial (ETFC) 4:05pm, $0.22

- FMC Technologies (FTI) 4:01pm, $0.74

- Fulton Financial (FULT) 4:30pm, $0.20

- Interactive Brokers (IBKR) 4:01pm, $0.03

- Intuitive Surgical (ISRG) 4:05pm, $3.81 - Preview

- Nabors Industries (NBR) 5:30pm, $0.36

- Pinnacle Finl (PNFP) 5:15pm, $0.50

- Robert Half Intl (RHI) 4:02pm, $0.58

- Sonic (SONC) 4:01pm, $0.34

- VMware (VMW) 4:01pm, $0.83

- Waste Connections (WCN) 4:05pm, $0.55

- Yahoo! (YHOO) 4:05pm, $0.30 - Preview

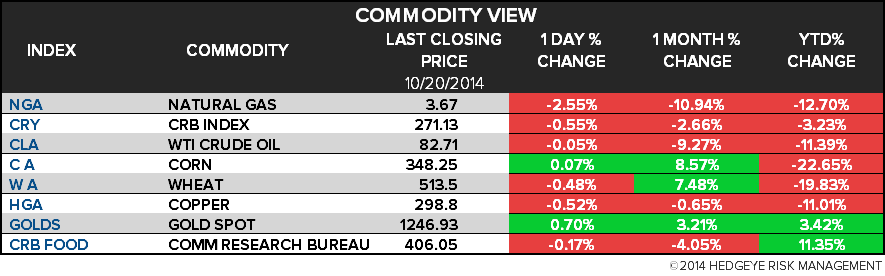

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Codelco Puts Faith in China to Resolve Metal Collateral Case

- Gold Buying Rebounds in India as Diwali Sales Shine: Commodities

- Oil’s Plunge Snares Nigeria Seeking to Defend Naira: Currencies

- Palm Oil Reserves in Indonesia Seen Shrinking Most in 19 Months

- Aluminum Rebounds as Copper Extends Gains in London Trading

- Brent Crude Rises as China’s Growth Exceeds Estimates; WTI Gains

- China’s ‘Aggressive’ Electric Car Ambitions to Boost Aluminum

- Soybeans Rise From 1-Week Low as Investors Assess Harvest Pace

- Rebar Drops to One-Week Low on China Economic Growth Concerns

- WTI Crude Seen Supported Near $75 a Barrel on Drop Below $80

- Arabica Extends Biggest Slump in Five Weeks as Sugar Declines

- Palm Growers Raised by Hong Leong to Neutral as Worst Seen Over

- Codelco Not Affected by China’s Metal Collateral Case (Video)

- Codelco to Sell $8 Billion Bonds for Record Copper Mine Spending

CURRENCIES

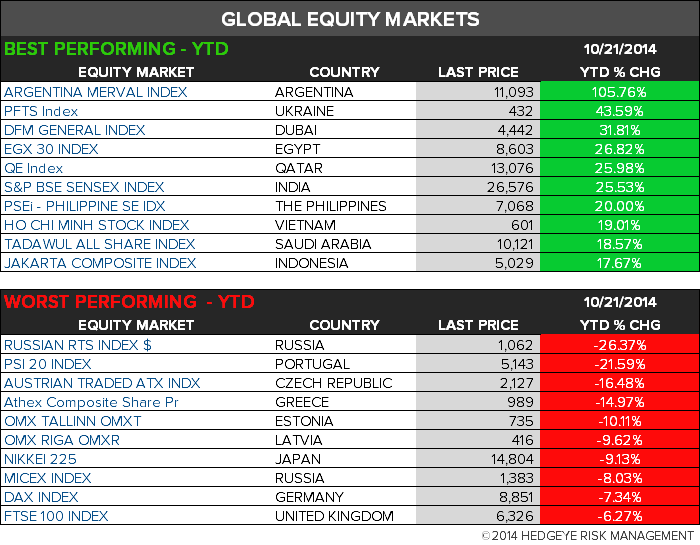

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

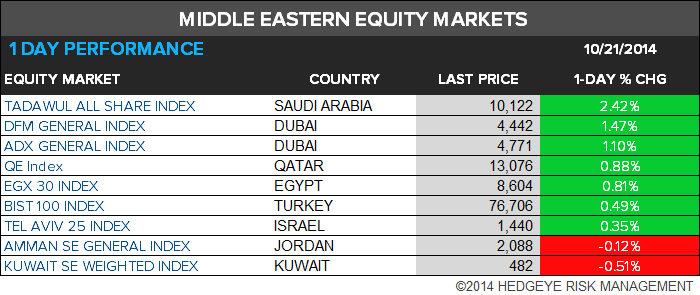

MIDDLE EAST

The Hedgeye Macro Team