CMG continues to be on our Investment Ideas list as a long.

Brief Analysis: 3Q14 marked another impressive quarter for Chipotle, which managed to grow same-store sales by nearly 20% at a time when the majority of quick service and fast casual restaurants would be pleased to deliver a low-single digit comp. The company continues to thrive amid what appears to be a secular shift in the way people, and particularly Millennials, eat out.

The stock traded down after hours, however, as low to mid-single digit comp guidance for 2015 came in well below the street's 7.2% estimate. We believe this was a concerted effort by management to temper aggressive expectations. This guidance may very well prove to be conservative, but CMG will be lapping the strongest period of comp growth since being spun out as a public chain in 2006.

Underlying food inflation was up +8% in the quarter, which is quite possibly the only red flag we could find in the quarter. The fact of the matter is, this is an incredibly strong company, with strong management, best-in-class unit economics, a robust balance sheet and unparalleled momentum. We believe any sell-off today would be a nice buying opportunity.

Comps: CMG delivered 19.8% comp growth in the quarter, beating estimates of 17.2%, led by traffic growth and, to a lesser extent, an +8.5% increase in average check. Management guided to low to mid-single digit comp growth in FY15. Revenues of $1,084 billion (+31.1% y/y) beat consensus estimates by 2.34%.

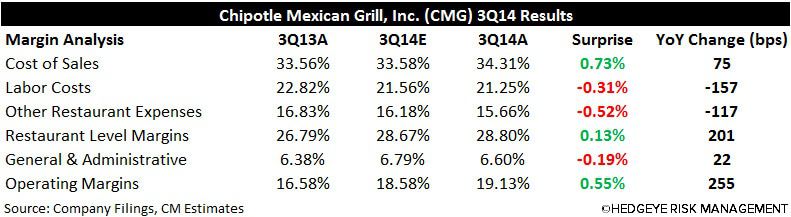

Margins: Despite an accelerating top line trend and a price hike, cost of sales squeezed profits in the quarter, coming in at 34.31% of sales (+75 bps y/y) vs. expectations of 33.58%, as beef, avocado and dairy inflation persists. Fortunately, Chipotle benefitted from sales leverage throughout the rest of its P&L as labor costs, other restaurant expenses, and general & administrative costs all came in well below expectations. Operating margins came in at 19.13% (+255 bps y/y), beating estimates by 55 bps.

Earnings: Adjusted EPS of $4.15 (+56% y/y) beat expectations of $3.83 by 8.26%.

What We Liked:

- Revenues of $1,084 billion (+31.1% y/y) beat estimates by 2.34%

- +19.8% same-store sales growth; +13.0% two-year average

- Restaurant level margin expanded 201 bps y/y

- Operating margin expanded 255 bps y/y

- Adjusted EPS of $4.15 (+56% y/y) beat estimates by 8.26%

- Throughput continues to improve; this quarter by 6 transactions at peak hour lunch and 6 transactions at peak hour dinner

- AUVs for restaurants in the comparable base reached an all-time high of $2.4 million

- Strong transaction growth with minimal price resistance and trade-downs

- Only repurchased $13 million of stock in the quarter; $127 million remaining on current share buyback program

- Comps momentum in September has continued into October

- Brand and food continues to resonate with consumers; particularly with Millennials who are increasingly rejecting traditional fast food

What We Didn't Like:

- Management guided to low to mid-single digit comp growth in FY15 vs. current consensus estimates of +7.2%

- Cost of sales ratio (34.31%) came in 73 bps above estimates and continues to march higher; beef remains an issue, while avocado could moderate, and dairy has likely peaked

- ACA costs will hit the P&L next year; impact unknown, but costs unlikely to exceed 1% of sales

- Catering took a step back from a favorable, in-season 2Q; only 1% of sales in 3Q

Call or email with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst