What To Do When the Stars Don't Align

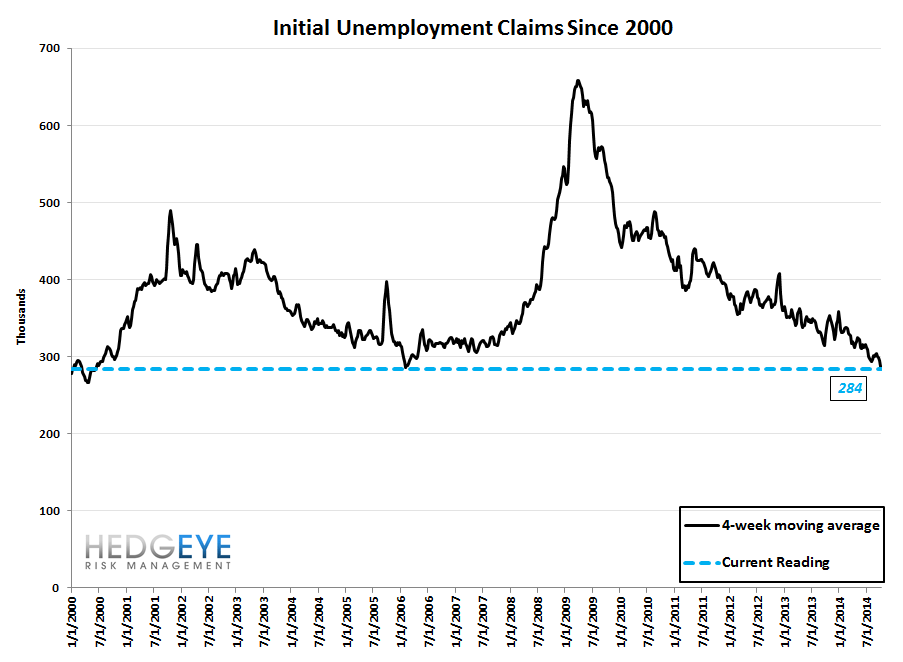

Sometimes conflicting data can put you in a tough analytical position. We track labor data closely because the credit cycle trumps all for Financials investors. Labor (i.e. loss frequency) is the primary driver of the credit cycle with collateral values (i.e. loss severity) riding shotgun. We track both. This morning's claims data suggests the recovery in the labor market is ongoing. In fact, the rate of improvement accelerated to the fastest clip we've seen YTD. Rolling NSA initial claims were better by 17.2% this week vs the prior year comp. Admittedly, the comps from last year were easier, making the significance slightly less, but the conclusion is still the same. The labor data suggests all systems go.

However, every Monday morning we also publish a note called the Monday Morning Risk Monitor and the titles of that note have been increasingly bearish for the last 3 weeks, including this past Monday's note: "Danger Zone". The Risk Monitor helps us navigate the short to intermediate trends while the labor market data helps us keep perspective on the longer-term credit cycle.

At the moment, they are in conflict. The short to intermediate term outlook is decidedly bearish based on the signals from our Risk Monitor. The longer-term outlook remains constructive, for now. A word of caution, however: the longer-term outlook is dynamic, and can be altered by short to intermediate term pressures. We've learned over the years to wait for the Risk Monitor to give us the green light before getting back in the water. So, for now, we'd be pressing the shorts.

The Data

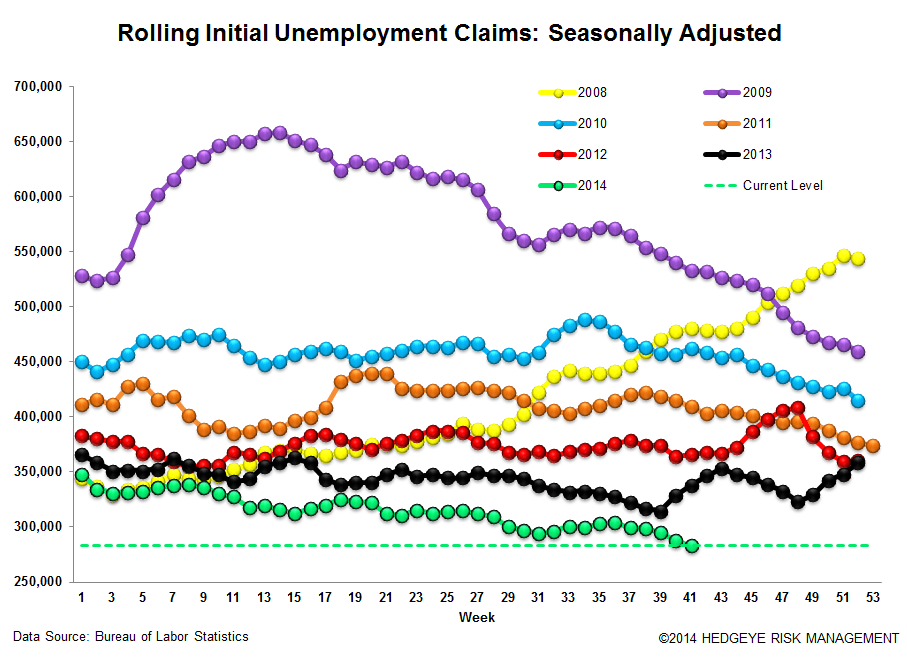

Initial jobless claims fell 23k to 264k from 287k WoW. The prior week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4.25k WoW to 283.5k.

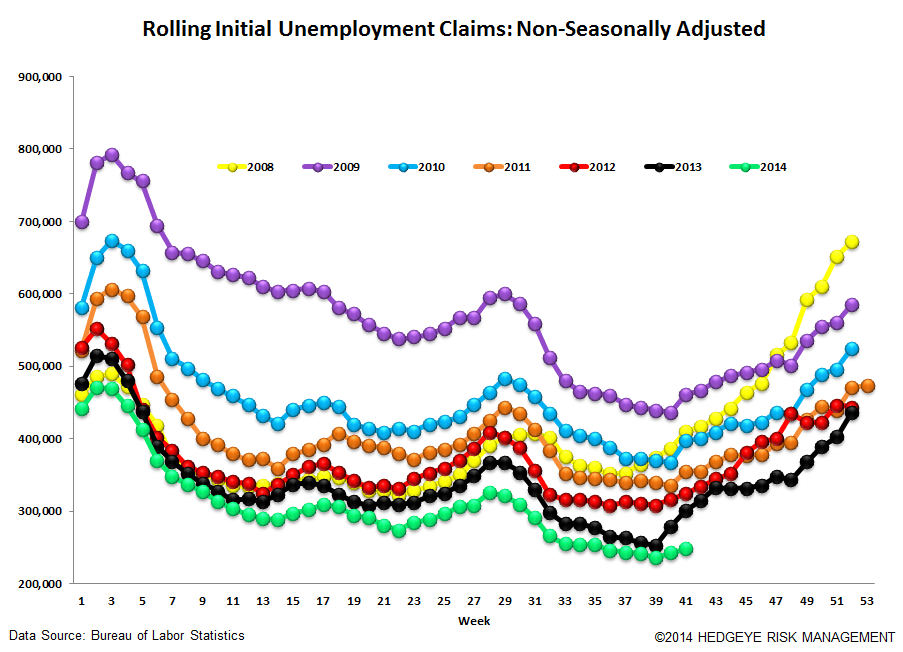

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -17.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of--13.4%

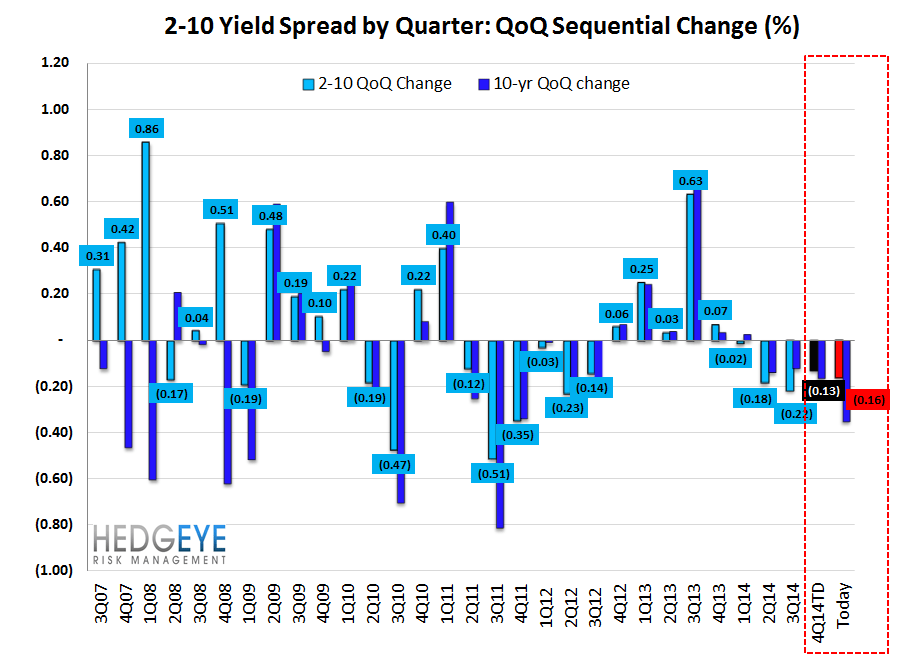

Yield Spreads

The 2-10 spread fell -4 basis points WoW to 183 bps. 4Q14TD, the 2-10 spread is averaging 186 bps, which is lower by -13 bps relative to 3Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT