This note was originally published at 8am on October 02, 2014 for Hedgeye subscribers.

“Did you think I’d lay down and die? Oh no, not I – I will survive.”

-Gloria Gaynor

I’m thinking some of the bond bears need some love this morning, so I thought I’d bring you some of that with Gloria Gaynor’s 1978 Grammy Award Winning disco love track, I Will Survive!

“At first I was afraid… I was petrified.

Kept thinking I could never live without you by my side…

But then… I grew strong. And I learned how to get along”

‘Oh, as long as I know how to buy the Long Bond, I will get along… I know I will stay alive. And I’ll survive. I will survive! Hey, hey…’

Back to the Global Macro Grind…

Being born in the 1970s, I still get what living without all of the entitlements in the world means. Savings matter. So does saying thank you to the people who helped bring me along in my #blessed life.

One of the greatest gifts I’ve ever received was the time in which I entered this business. From my first trading internship at Williams Trading in the summer of 1998, to my first job @FirstBoston in 1999, I saw both the hedge fund business hockey stick and the Tech #Bubble manifest, then collapse.

For my 1st three years on the buy-side, the SP500 was down on the year (2000, 2001, 2002), so I learned how to A) not lose other people’s moneys first, then B) get really long when people hated stocks in 2003-2006. Oh, and then another #Bubble in 2007. Market crash. Epic recovery. Then this…

But what is this?

I’ll go through what I think this is on our flagship research call (Q4 Macro Themes) today at 1PM EST (ping Sales@Hedgeye.com for access). But to summarize it in hash tag terms, here it is:

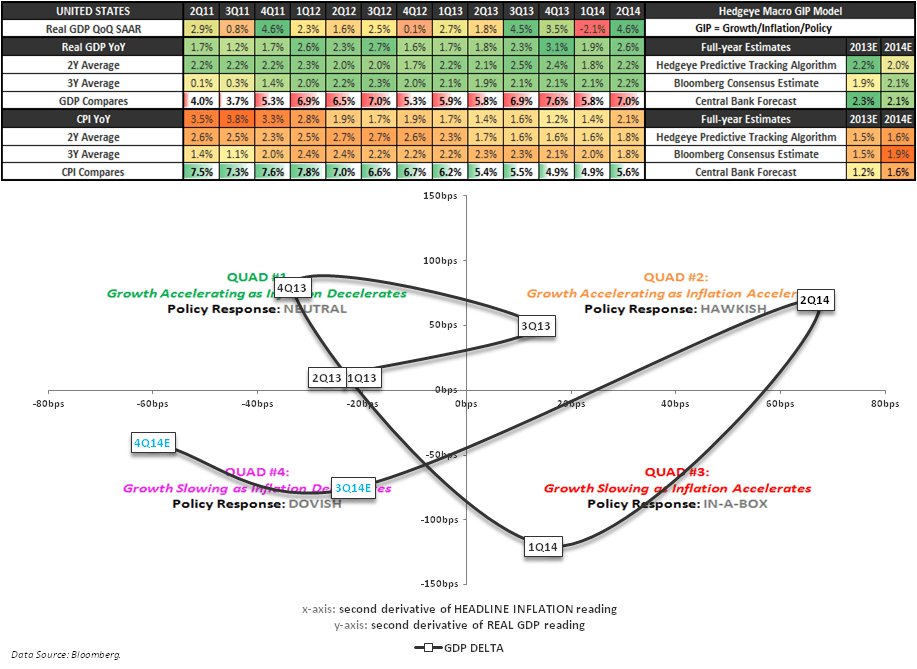

- #Quad4 – where both US growth and inflation (in rate of change terms) are slowing, at the same time

- #EuropeSlowing – and why Draghi’s central planning drugs will be hard pressed to arrest it

- #Bubbles

Oh, yes. #Bubbles.

How does your portfolio survive an early cycle global recession as asset prices are deflating and #Bubbles are popping?

- Raise Cash (mine is at 62% in my asset allocation model this morning)

- Be big on the long side of Long Term Treasuries (TLT, EDV, etc.)

- On pullbacks add to Munis, and maybe some Healthcare and Consumer Staples stocks

While this call may have sounded aggressive with the 10yr UST yield at 2.63% less than 3 weeks ago, it should have. While I don’t get paid like I used to (just putting the position on, in size), I still wake up at 4AM wanting to win, just like you do.

In Signal Terms (Real-Time Alerts), I issued 33 SELL signals (13 BUYS) in the month of September. Most of the sells were in US and European equities. Most of the buys were bonds. And I’d still buy more long-term bonds if there’s another opportunity!

When something big and contrarian like this is going your way, you don’t run for the exits during no-volume market head-fakes. You press it (or, as the great Stan Druckenmiller would say, “you spread your wings”).

That said, almost 100% of the questions I got in mid-September had to do with:

- Selling Bonds

- Buying Stocks

When the right questions should have been:

- How big do I make the Long Bond position on the recent pullback?

- How big do I get on the short side of the Russell 2000’s liquidity trap?

Markets don’t go from #bubble mode to buys on a -3.2% correction (that’s where we are for the SP500). However, on a -10.2% draw-down (Russell 2000’s drop from its all-time #Bubble high on July 7th 2014), levered long players start to freak out.

As they should.

What is the catalyst to reverse the Long Bond’s (TLT) total return of over +18% (vs Russell -7% YTD loss)? I don’t think there is one. If there is one catalyst we have been warning investors of all year long that matters most here, it’s the cycle.

That is it. The cycle, slowing.

And if one ISM slow-down print (yesterday’s was reported at 56.6 for SEP vs 59.0 for AUG) can smoke the 10yr Treasury Yield down to 2.39% in a day, what do you think the next bad jobs report and/or US GDP miss is going to do?

Personally, I don’t say buy FogDog.com or the FireEye on that. Stay with our Macro Playbooks, and you will survive this #bubble.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.36-2.53%

SPX 1927-1963

RUT 1067-1118

VIX 14.84-17.93

EUR/USD 1.26-1.28

WTI Oil 89.01-92.14

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer