Brief Analysis: DFRG reported an unimpressive quarter, in our view, despite the fact that the market has responded positively. We covered our short last week for this reason, as sentiment around restaurants has been improving due to strong industry sales data. What really saved the day, however, was management's decision to maintain its full-year guidance and not provide guidance on 2015. We don't think its unreasonable to expect DFRG to hit the numbers in 2014, but believe 2015 guidance on the 4Q14 earnings call will be a negative catalyst for the stock. The street currently expects 2015 EPS growth of 19%, after delivering -7% growth in 2013 and what looks to be 3% growth in 2014. Considering persistent cost of sales inflation, the ongoing struggle at Sullivan's and operational inefficiencies associated with the rollout of the Grille, we view this as highly unlikely.

Comps: DFRG delivered +3.7% system-wide comp growth in the quarter on a calendar basis. Del Frisco's Double Eagle delivered +8.4% same-store sales growth driven by a +4.6% increase in customer counts and a +3.8% increase in average check. Sullivan's delivered +0.6% same-store sales growth driven by a +7.3% increase in average check, offset by a -6.7% decline in customer counts. Per usual, management did not disclose same-store sales data for the Grille. Consolidated revenues of $61.949 million (+14.3% y/y growth) missed consensus estimates of $62.529 million by 93 bps.

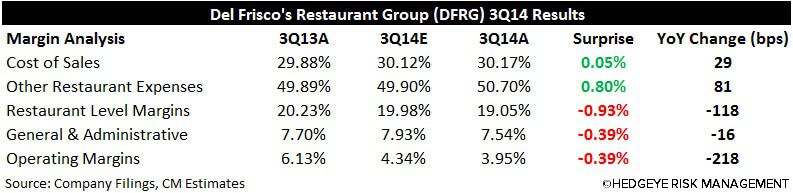

Margins: DFRG suffered from margin deleverage in the quarter, primarily driven by two new Grille openings, the ongoing sales challenges in Phoenix, AZ and Palm Beach, FL, and persistent beef inflation. Cost of sales surprised to the upside (+29 bps y/y) as restaurant level margins (-118 bps y/y) and operating margins (-218 bps y/y) fell short of consensus expectations.

Earnings: Adjusted EPS of $0.08 was in-line with expectations and notably stronger than last year's $0.02 loss. Strength here was primarily driven by G&A leverage and the reduction of 165,496 shares of outstanding stock ($3.6 million in repurchases).

What We Liked:

- System-wide same-store sales increased +3.7% on a calendar basis

- Del Frisco's delivered its 19th consecutive quarter of comp growth (+8.4%)

- Del Frisco's delivered an impressive +4.6% increase in customer counts

- The natural hedge of the Grille should help mitigate food cost inflation as it becomes a larger part of the portfolio

What We Didn't Like:

- Top-line miss

- The reliance on share buybacks to hit bottom-line estimates

- Persistent beef inflation with no end in sight

- Restaurant level margin deleverage

- Operating margin deleverage

- Sullivan's rapid -6.7% decline in guest counts

- Ongoing weakness at the two Grille's in Phoenix, AZ and Palm Beach, FL

- 2013 class of Grille's continue to perform below the level of both 2011 and 2012 classes

- Sullivan's continues to be a drag on the company

- Grille continues to be an unproven growth concept

- Management approved another $25 million in share repurchases over the next three years despite no FCF generation

Research Recap

DFRG: New Best Idea Short (06/12/14)

DFRG: A Castle-in-the-Air (07/02/14)

DFRG: Thoughts into the Print (07/21/14)

DFRG, EAT: Covering Our Shorts Given Strong Knapp Sales (10/09/14)

Call or email with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst