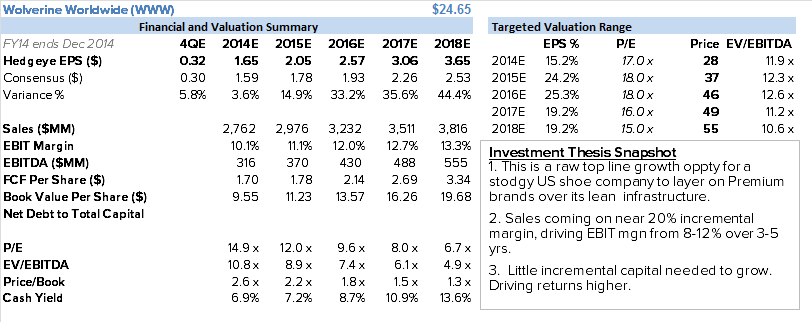

Conclusion: Despite the 5% pop in the stock, WWW is officially in the penalty box from where we sit. Our long thesis builds to 20%+ EPS growth, or a $45 stock in 12-18 months (70%+ upside). But we’re not seeing the revenue that we want to see to support a big call. We still think that a worst case top line is 200bp better than the consensus for next year, which should result in a minimum of 10-20% upside in the stock. But is that enough for WWW to remain on our Best Ideas list? Probably not. It’s not bad, but it wouldn’t be the kind of return Hedgeye Retail is playing for. We think we’re being paid to wait on this cheap, high quality, hated name. We have it on a 3-6 month leash.

DETAILS

Our patience is wearing thin for our bullish call on WWW. Yes, the headline was good -- $0.63 vs our $0.62 and the Street at $0.59. But revenue missed our estimate. We don’t care that sales were in line with WWW’s internal forecasts, and largely in-line with guidance. We need to see something bigger than guidance. And thus far it’s nowhere in sight. The crux of our call is predicated on a meaningful growth acceleration in Sperry, Keds, Saucony and Stride Rite outside of the US – in markets that were largely ignored by the prior owner. Our math gets us to growth of 8-10% on the top line, 12-14% gross profit, 16-18% EBIT, and 20-22% EPS as the company’s cash flow is used to de-lever its balance sheet. That’s an algorithm we can get behind, especially for a company that has such a proven track record of consistently creating shareholder value over such a long period of time. That kind of sustainable growth is probably worth a high teens p/e, which implies a stock near $45 in 12-18 months (18x $2.50 in ’16).

This thesis is fine and good, but the reality is that the company is not delivering the revenue upside we need to see. Management talks about how revenue penetration for brands like Sperry has doubled in two years as a percent of total (5% in 2012 up to 10% of Brand revenue). But if consolidated revenue is flat does it really matter? The answer is no. We get their point that there are a lot of moving parts on the top line – like the Stride Rite realignment plan, decision to take Sperry out of bad channels of distribution, and the general hit we’ve seen all year with the Women’s Sperry business. The strategic actions are temporary, and the Sperry business in the US appears to have stabilized. As such we should see a natural lift in sales next year.

That said, our point all along is that we needed to see a sequential acceleration to a mid-high-single digit growth rate by 4Q, which should set the company up to benefit meaningfully from significant depth on the international bench starting in 1Q15. Based on what the company says, at least the 4Q growth ramp is in the cards. But there’s no question that our conviction is waning in its ability to drive an incremental 800-1,000bp of growth starting in another 12 weeks. To be clear, this growth level is our goal – not the company’s. The money making call will be in management’s ability to deliver sales growth that is far in excess of what it is telling the Street. The good news there is that consensus sales growth expectations next year are only for 3.7%. We think that a worst case number is 5-6%.

Is that enough for WWW to remain on our Best Ideas list? Probably not. Is it enough to make the stock work by 10-20% from here? Probably. But that’s not the kind of return Hedgeye Retail is playing for.

The good news is that the stock is trading at only 14x earnings, remains quite hated, and is facing a near term bump in its revenue – as evidenced by its order trends. We still think that there will be a more meaningful contribution from its non-US business in 2015, which does not appear to be represented by the consensus estimates. We’re not worried about this stock working, but based on the company’s top line success over three (six tops) months we’ll know whether we should fish or cut bait on WWW as one of our core long ideas.

Our Sentiment Monitor (which combines short interest and sell side ratings) shows just how bad WWW Sentiment is.