This note was originally published at 8am on September 30, 2014 for Hedgeye subscribers.

“This is the real world, homie, school finished.”

-Kanye West

That’s the opening quote to the latest business book I have cracked open, The Hard Thing About Hard Things, by Ben Horowitz (of Andreessen Horowitz fame).

Unlike most of the #behavioral and #history books I’ve been citing throughout the year, this one has a much more #bubbly feel to it. I’m only four chapters in but, suffice it to say, I don’t agree with some of Horowitz’ business building and leadership principles.

Maybe it’s because his parents were communists. Maybe it’s because I’m a knucklehead athlete. I’m not sure. I’m just certain that all of the techie “valley” culture and the Keynesian Economics school stuff isn’t playing out according to plan, in the real world.

Back to the Global Macro Grind…

Another one of the 2014 Tech Bubble’s “he’s got mad dough, bro” darlings who is selling his book these days (Peter Thiel) made headlines yesterday in telling Fox Business anchor Deidre Bolton that it wasn’t, well, a Tech Bubble.

Thiel, who blew up his hedge fund, multiple times (buying stocks in 2008, shorting them in 2009, etc.) is as academically intelligent as I can be hockey-head dumb, went on to say that it’s not a bubble in stocks because there is a bubble in bonds.

To be specific, Thiel said “I’m investing in Tech stocks to hide from the government bond bubble.” “So”, I replied (in tweet terms to @peterthiel) “I’m hiding in the Long Bond so that I can be short the Tech Bubble.” #timestamped

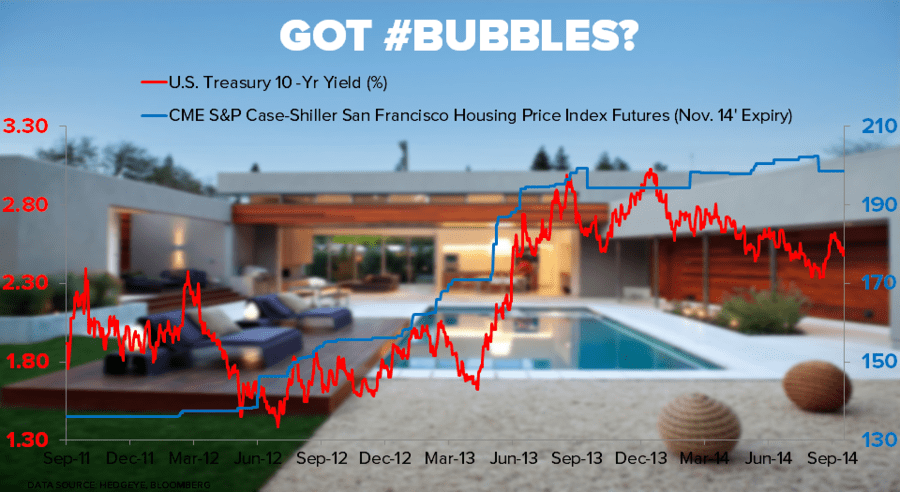

Got #Bubbles?

We do. On our Q4 Macro Themes Call we have a whole slide deck full of these suckers. If you’d like to be educated on some #history and #context of the current components of the US stock market bubble, please join us this Thursday at 1PM EST.

While there is plenty of low-quality junk debt in this world that we would consider #bubbly, the upside to fully understanding how all of this might end (Japanese style) is that the mother of all bubbles (Japanese Government Bonds) has been inflating for decades.

While I’m not sure if Thiel joined the ranks of the many who have a higher IQ than I and shorted Japan’s debt because the country’s Keynesian Abenomics experiment was going to fail, the only failure in the real world was not being long those bonds.

Homies, here’s the point:

- In the face of failing economic policies, Japan, Europe, and USA have only one option – moarrr #cowbell

- As these central planners attempt to artificially inflate economies, they simply inflate asset prices

- As asset prices (Tech Bubbles) inflate, so does the cost of living associated with those assets (CA real estate)

- As the cost of living rises to pain thresholds consumers cannot overcome, the economy surprises on the downside

- Then, central planners respond with moarrr #cowbell

I’m sure Kanye West can come up with a song that’s more clever than what this really is. But I’m pretty sure that the 60% of Americans who have negative real wage growth (read: falling purchasing power) since the Fed engaged with its Policy To Inflate get it.

So do the Japanese. Here’s the latest on that Eastern front:

- Japanese Real Wages -2.6% year-over-year in August (vs. -1.6% y/y in July)

- Japanese Household Spending -4.7% year-over-year in August (vs. -5.9% in July)

In Mucker rapper terms, that is called getting train wrecked.

Oh, and if you aren’t into Burning Yens and Euros, there’s this other devaluation story to update you on this morning – Russia:

- The Russian Ruble dropped -14% in the last 3 months (versus a basket of Dollars and Euros)

- The Russian Trading System Index (its stock market) is crashing, -19.1% YTD

- And the Ruskies are going to now “defend” their currency by raising interest rates!

As it has, across centuries, this is how the Keynesian School of QE and/or Currency Devaluation ends – epically. I’ll have no problem shorting Treasuries (our call for all of last year) when our research and risk management signals tell me to do so.

But, in the meantime, I’ll stay long of Long-Term Treasuries (via TLT, which has a total return of +17.1% YTD) and short of small cap illiquidity and social tech bubbles via anything that is getting smoked in TAM terms right now.

While the over 40% of IPO’s that are crashing (down 20% or more from peak) aren’t all techie related, both in # of issues and in market cap terms, the froth of this #Bubble in US growth expectations is as big as when Horowitz’s first company almost went bankrupt.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.46-2.56%

SPX 1962-1987

RUT 1097-1132

VIX 13.81-16.75

EUR/USD 1.26-1.29

WTI Oil 91.69-94.98

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer