RETAIL FIRST LOOK: THE BOTTOM IN FAMILY FOOTWEAR

AUGUST 3, 2009

TODAY’S CALL OUT

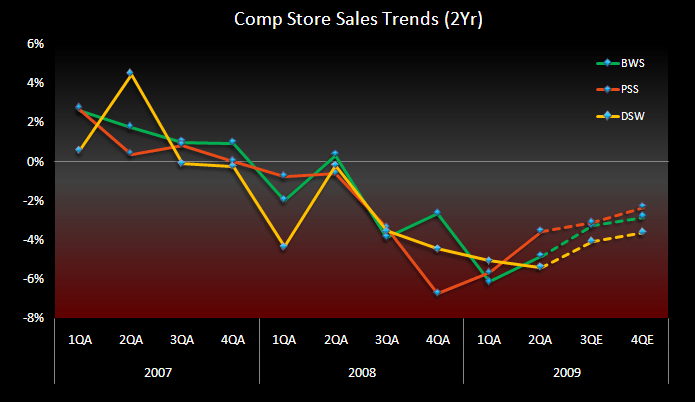

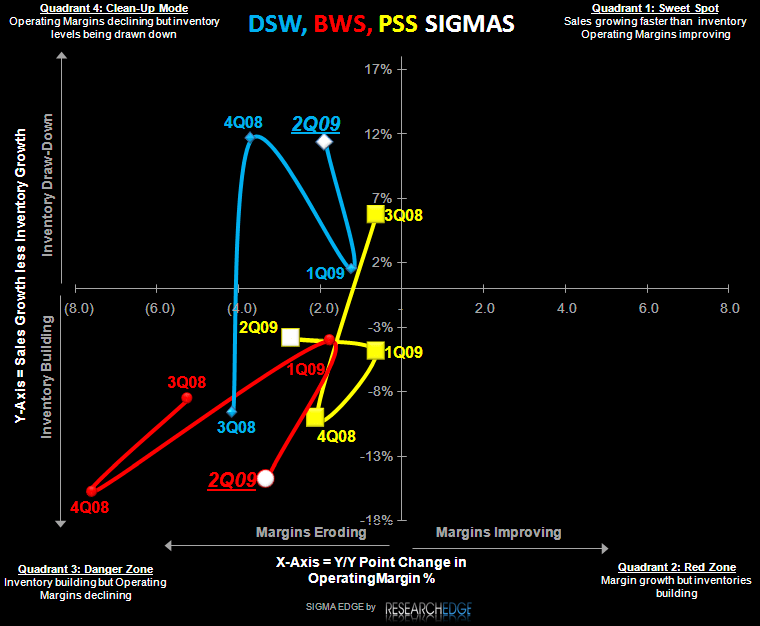

By no means could anyone call the PSS -7.3% comp good, but after seeing PSS, DSW and Famous Footwear (BWS), one thing that is clear to me is that the family footwear space has probably seen its bottom. The charts herein speak for themselves.

LEVINE’S LOW DOWN

Some Notable Call Outs

- While the benefit of lease negotiations has been talked about on just about every call this earnings season, management mentioned that Collective Brands is realizing 15-20% reductions on leases. With rent accounting for ~15% of COGS and roughly 20% of the store base up for renewal each year. One of PSS’s tailwinds heading into 2010 just got stronger.

- Oxford Industries (owner of Tommy Bahama) noted that demand for their Spring/Summer 2010 lines are stronger than expected. While most wholesalers have taken a more conservative approach to inventories heading into the 2H, improving business is resulting in the pulling forward of deliveries and what inventory happens to be on hand. With OXM in a similarly under-inventoried position, they too are having to ramp business to meet demand.

- Among the regions of strength noted on OXM’s call was…Hawaii? It was suggested that the swine flu could be impacting retail as vacationers decide to reroute plans from destinations like Mexico where the epidemic is in full swing to alternative destinations. Florida was also highlighted as having a notable rebound through August.

MORNING NEWS

-Samsonite files for bankruptcy and reorganization - Samsonite Company Stores, the U.S. retail division of Samsonite Corp., filed both a Chapter 11 petition for bankruptcy court protection and a prepackaged plan of reorganization on Wednesday in a Delaware bankruptcy court. The store division, based in Mansfield, Mass., said it expects to exit Chapter 11 in 45 to 90 days. Under the terms of the reorganization plan, creditors would receive 100 percent of their claims. The plan includes cutting Samsonite’s 173-store count by 47% and streamlining operations. Parent company Samsonite Corp. is not a party to the filing. Donald E. Walden, vice president for finance and chief financial officer of Samsonite’s store division, said in an affidavit filed with the bankruptcy court that U.S. sales in 2008 were $108.1 million, down from $112 million in 2007. <wwd.com/retail-news>

-Banglaesh's exports of finished garments to Japan increased over 100% - Banglaesh's exports of finished garments from Bangladesh to Japan has increased over 100% in the fiscal year 2008-09, valued at US $74.381 million ascompared to $28.035 million in the previous year. The country has reduced its finished garment imports from China, which helped its industry to increase its sales in Japan, according to Fazlul Hoque, President Bangladesh Knitwear Manufacturers and Exporters Association (BKMEA). Hoque said that Japan is a ready market for Bangladesh as it produces high-quality products which are exactly what the Japanese market need. The ongoing trend indicates that the apparel exports of Bangladesh will reach billion dollars in the next five years. Japanese leading retail chains Uniqlo has also been purchasing from Bangladesh and is planning to make an initial investment of $100 million, added Hoque. <fashionnetasia.com>

-Chinese ambassador urged the EU to relax its anti-dumping measures - Chinese ambassador has recently urged the EU to restrain its use of anti-dumping measures against imports from China and called for more dialogue and cooperation. "We saw re-emergence of anti-dumping cases against China recently. We're very concerned about an increasing number of Chinese enterprises received unfair treatment," Song Zhe, Chinese ambassador to the EU said. "But we believe between China and Europe, there is more cooperation than competition, more opportunities than challenges. At present, it is urgent to strengthen economic and trade cooperation by maintaining mutual flow of trade and investment and creating more business opportunities," he added. Faced with the worst economic crisis in decades, the EU has launched a series of anti-dumping actions against China this year, covering a wide range of Chinese products. As from late July, the 27-nation bloc took five separate decisions in just three weeks. <fashionnetasia.com>

-Hundreds of American Apparel employees must leave due to illegal immigration status - Hundreds of American Apparel Inc. workers must leave the company because they were unable to prove their immigration status or fix problems with their employment records, the company said Wednesday. The terminations come two months after the Los Angeles manufacturer and retailer announced that a government inspection had found that about 1,600 of its workers didn't appear to be authorized to work in the U.S. About 200 more had been found to have discrepancies in their employment records. Among the infractions found were some employees' use of fake Social Security numbers. "There are approximately 1,500 workers facing termination during the month of September," said Peter Schey, a lawyer for American Apparel. The company "is very disappointed and disheartened at having to terminate a very large number of workers who by and large have been reliable contributors to the success of the company." All of the affected workers are based at the company's manufacturing facility in downtown Los Angeles, Schey said. Virginia Kice, a spokeswoman with Immigration and Customs Enforcement, declined to discuss American Apparel specifically, saying the federal agency was "not at liberty to discuss fines levied in work site enforcement cases until the fine amount becomes final." <latimes.com>

-Retail sales for all core outdoor stores combined (chain, internet, specialty) declined 4% in July - Select equipment, outerwear and several footwear categories grew this July. Year-to-date sales totaled $2.6 billion, down 4% from the same period a year ago. <sportsonesource.com>

-China Resources Says It May Sell Stake in China Joint Venture With Esprit - China Resources Enterprise Ltd., the local partner of SABMiller Plc, may sell its stake in the venture it has with clothier Esprit Holdings Ltd. as it seeks to focus on retail, food and beverage businesses. <bloomberg.com>

-New Balance and aerie by American Eagle Launch Fitness/Lifestyle Shoe - New Balance and aerie by American Eagle announced the introduction of the New Balance 600, a new fitness lifestyle shoe. The NB 600 is available beginning today exclusively at all aerie standalone stores across the country. Offered at $65, the shoe is designed to complement aerie f.i.t.™, aerie’s fitness and workout wear line. The NB 600 features a comfort molded EVA sole unit, Abzorb (a proprietary cushioning foam that resists compressions for all day comfort) and a lightweight mesh upper. The 600 is available in two trendy color combinations of grey/pink and white/lime, the perfect solution for the girl who wants an athletic look without sacrificing fashion. “With this program we have the opportunity to reach a style-savvy consumer with fashionable athletic footwear that merchandises with the incredible range of aerie,” says Steve Gardner, strategic business unit manager for New Balance Lifestyle. “It’s a program that brings a fresh perspective to product and merchandising, while synergizing these two great brands.” <corporate-ir.net>

-Chico’s tries on a new distribution center - After making an investment of $15 million and adding about 189 full-time jobs, Chico’s in August made the move to a new 300,000-square-foot distribution facility that will give the retailer room to expand through 2016. <internetretailer.com>

-ColdwaterCreek.com leads the e-retailer pack in August response time - For the seventh month running, ColdwaterCreek.com gave shoppers the fastest high broadband access time among large web retailers, says Gomez. In August ColdwaterCreek.com produced a high broadband response time of 4.04 seconds. <internetretailer.com>

-Cato brings on new board member - The Cato Corporation reported that on August 27, 2009 the Board of Directors appointed Mr. Bryan F. Kennedy, III to fill a vacancy on the Board effective September 1, 2009. Mr. Kennedy is President and Chief Executive Officer of Park Sterling Bank. Mr. Kennedy currently serves on the board of Park Sterling Bank and as Chairman of the Board of Hospice and Palliative Care-Charlotte Region. <prnewswire.com>

-Quick look at expectations for today's same store sales - August same-store sales results, being reported today, are expected to be better than July’s and mark the last month of difficult comparisons with 2008 dating back to the days before last September’s financial crisis. August comps will provide a better idea of how this year’s later back-to-school season has shaped up. In retailers’ favor is a series of state tax holidays that shifted to August, putting more pressure on July, but working against them is a later Labor Day than in 2008, sales for which will fall into September. One factor could neutralize the other. According to the International Council of Shopping Centers, retail sales for the week ended Aug. 29 fell 0.5% from the prior week and 0.7% from the comparable week in 2008. The first week of August came in flat versus the prior week but sales were up 0.4% on a year-over-year basis. ICSC predicts August comps declined between 3.5% and 4%. <wwd.com/business-news>

-Fast Retailing Co. Ltd. wants to be the biggest around - Tadashi Yanai, chairman of the firm, said Wednesday that the Japanese apparel company aims to grow its annual sales by more than seven times to 5 trillion yen, or $53.7 billion, by the year 2020. And analysts don’t think the goal is that far-fetched. “We hope to become the biggest maker and retailer in fashion,” Yanai said during a press conference. “The dream will come true if we can grow our business by at least 20 percent each year.” The executive reiterated Fast Retailing is eyeing potential acquisitions, especially in Europe, but said there are few attractive companies on the market right now. Even without acquisitions, he said he thinks the company can reach 1 trillion yen, or $10.74 billion, in sales by 2010. <wwd.com/business-news>

-Thom Browne offers new line of clothes with lower price points - Thom Browne is establishing two new ranges that will be priced 30% to 40% lower than his fashion-forward runway offerings, making him the latest men’s designer to adopt a strategic focus on lower prices and repositioned staples — as Tim Hamilton, Duckie Brown and others have also done recently. The new Thom Browne ranges, launching for spring 2010, do not have distinct labels but are known unofficially as Thom Browne “classics” and Thom Browne “red/white/blue.” Initiating with a few styles, they are expected to grow to 50 percent of the collection and broaden the market for the brand. <wwd.com/retail-news>

RESEARCH EDGE PORTFOLIO: (Comments by Keith McCullough): BBBY, KSWS

09/02/2009 03:25 PM

BUYING BBBY $35.76

McGough and Levine continue to have a very high level of conviction that the earnings recovery will be there for BBBY. KM

09/02/2009 03:18 PM

BUYING KSWS $9.29

So far, this dog has acted exactly like what McGough called it - a dirty wet dog. There is value here, and that's why I am buying more of it on red. KM