Current Best Ideas:

Key Takeaway:

Our last two weekly risk monitors have been titled:

"Don't Get Complacent" - 10/6/14

"Risk is Rising" - 9/29/14

Our Risk Monitor note was born in 2011 out of the recognition that - as Dan Och famously once said - "If you don't do macro, macro will do you". Its relevance obviously waxes and wanes depending on the environment, but the point of the product has never changed. It's intended to be an early (or at least concurrent) warning system as it measures a number of high-level macro signals across asset classes and geographies.

For the last few weeks we've been flagging rising risk dynamics across the complex of indicators we track and last week we finally got a material sell-off. The XLF dropped 3% last week and is now down 3.5% on a month-over-month basis. This week, the risk monitor looks similar to how it has the last few weeks: Red. Red permeates the summary table below suggesting it's not just a recent US equities phenomenon but rather a multi-asset class/geography problem. In other words, correlations are rising globally as the sell off gathers momentum.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 12 improved / 4 out of 12 worsened / 7 of 12 unchanged

• Intermediate-term(WoW): Negative / 3 of 12 improved / 7 out of 12 worsened / 2 of 12 unchanged

• Long-term(WoW): Negative / 3 of 12 improved / 4 out of 12 worsened / 5 of 12 unchanged

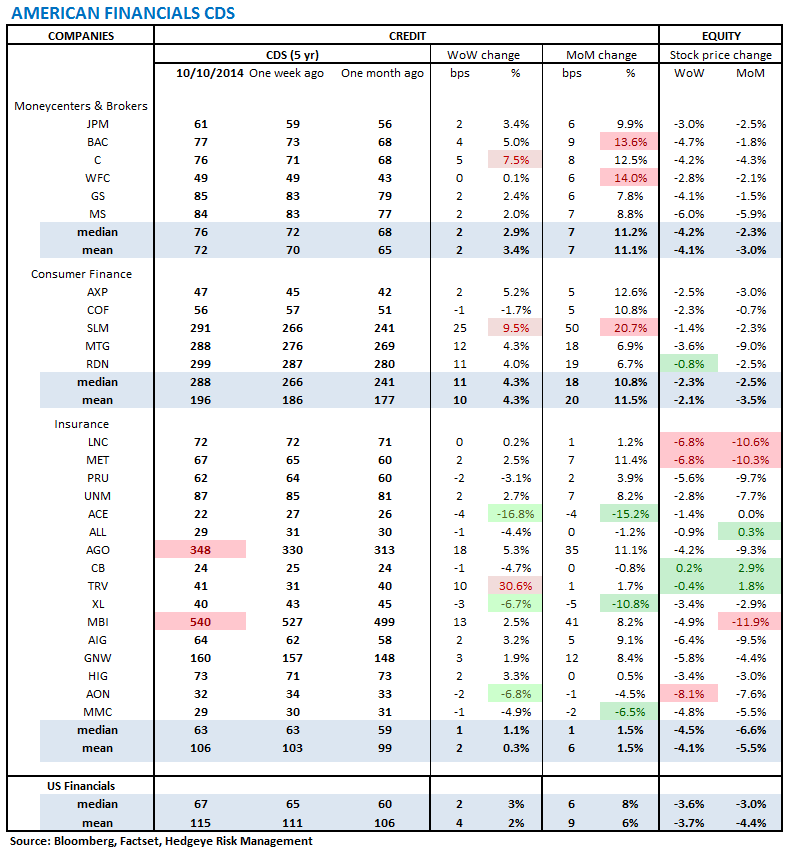

1. U.S. Financial CDS - Swaps widened for 19 out of 27 domestic financial institutions. The widening was modest at +4 bps, on average, but that brings the month-over-month change up to +9 bps, on average. The large cap banks are higher by 7 bps (+11 %) on the month now. We'll see what earnings season has in store beginning tomorrow.

Tightened the most WoW: ACE, AON, XL

Widened the most WoW: TRV, SLM, C

Tightened the most WoW: ACE, XL, MMC

Widened the most MoM: SLM, WFC, BAC

2. European Financial CDS - Swaps were notably wider across Spanish Banks and Russia's megabank, Sberbank. We are intrigued with Russia as falling oil prices coupled with the effects of ongoing Western sanctions appear to having a significant weakening effect on Russia's economy. The average CDS profile across the EU bank complex is moving in the opposite direction of Euribor-OIS, our preferred gauge of systemic risk for the European banking system. In other words, while the systemic risk measure appears to be declining, the average individual risk measure across European banks is rising. Stay tuned.

3. Asian Financial CDS - Indian banks saw swaps tighten on the week, as did two out of three of the big Chinese banks. Much of Japan was unchanged on the week, except Mizuho which widened +4 bps to 56 bps.

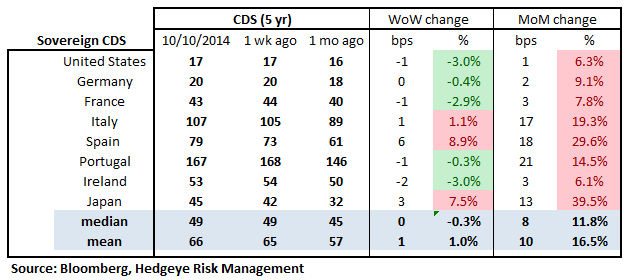

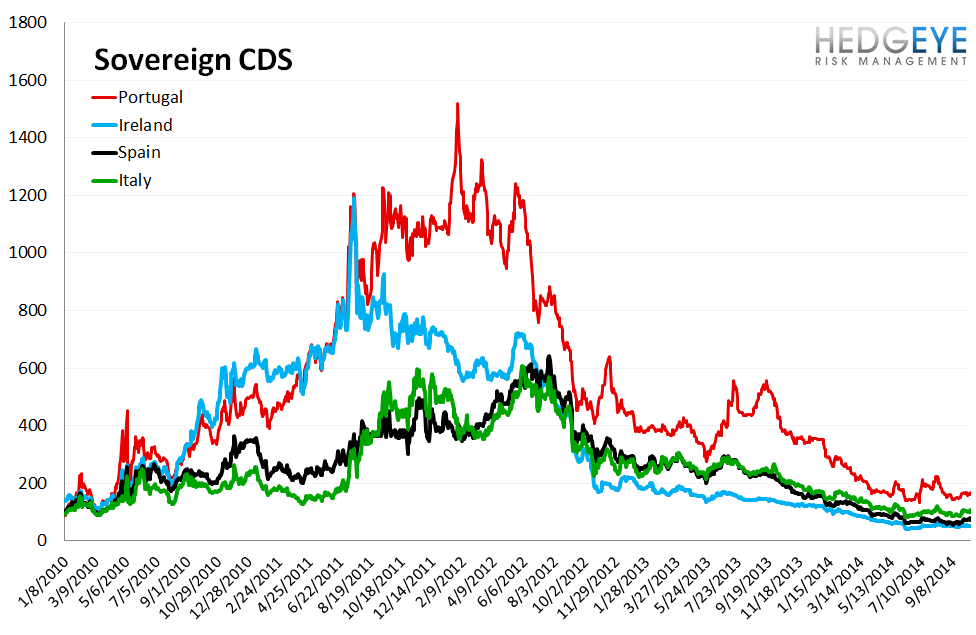

4. Sovereign CDS – Sovereign swaps were mixed with Spain widening the most at +6 bps to 79 bps. On balance, however, the average change for the week was just +1 bp.

5. High Yield (YTM) Monitor – High Yield rates rose 17.4 bps last week, ending the week at 6.12% versus 5.95% the prior week.

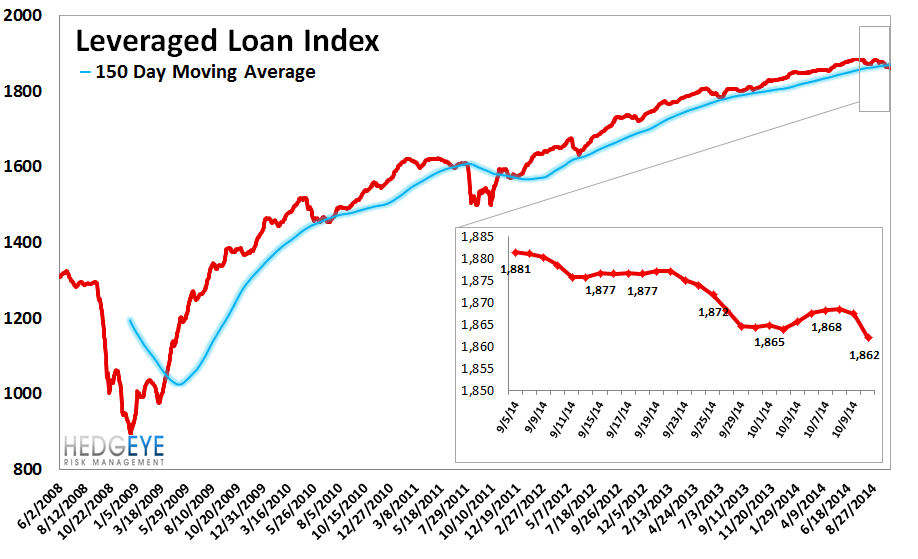

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 4.0 points last week, ending at 1862.

7. TED Spread Monitor – The TED spread fell 0.3 basis points last week, ending the week at 22.1 bps this week versus last week’s print of 22.36 bps.

8. CRB Commodity Price Index – The CRB index fell -0.8%, ending the week at 276 versus 278 the prior week. As compared with the prior month, commodity prices have decreased -2.5% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps to 10 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 3 basis points last week, ending the week at 2.56% versus last week’s print of 2.53%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China rose 0.1% last week, or 4 yuan/ton, to 2921 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

12. 2-10 Spread – Last week the 2-10 spread tightened to 186 bps, -2 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.2% upside to TRADE resistance and 1.7% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT