“But pardon, gentles all…”

-Shakespeare

That’s from William Shakespeare’s Prologue to Henry V. It’s also the opening volley from a #history brick my wife gave me for Father’s Day (sorry, just digging into it now!) called The Guns At Last Light – The War in Western Europe 1.

While I think she sometimes thinks I’m at war with my keyboard in the early mornings, she puts up with my market life – and for that I am forever grateful. From my family to my friends at the firm, getting it done is an all-out team effort.

But whose team is The Bear on? While I received some kind emails while in London last week, I’m not sure that being right this time is a good thing. The #Quad4 Deflation is nastier than a gnarling grizzly. And I fear the war between inflated asset #Bubbles and gravity has just begun.

Back to the Global Macro Grind…

The thing about fear is that you need to accept it before you conquer it. Last week’s +46% move in the front-month fear (VIX) index to +54.8% YTD should help pave part of that path towards acceptance. But don’t forget that there’s a long way between denial (1st stage of grief), anger, bargaining, depression, and acceptance.

Maybe using the Five Stages of Grief is a little over the top for a Monday morning. Maybe not (especially if you are a NY Jets fan). Being bearish at 1208 on the Russell (all-time #Bubble high = July 7th) or during the Ali-Bubble (BABA) IPO day (September 19th) at SPX > 2011 wasn’t easy for me. The denial stage for the bulls was equally isolating for our bearish macro view.

So pardon, gentles all – isolation is often where the alpha lives. And we certainly hope you had the Long Bond (TLT) on versus the Russell 2000 (short side) as the performance divergence in being long #GrowthSlowing hit its widest for 2014 YTD (ex-reinvesting interest, TLT = +18.3% YTD vs Russell 2000 -9.5%).

In US Equity terms, here’s how the Def-#Quad4 Deflation looked last week:

- SP500 down -3.1% (down for the 3rd straight week) to +3.1% YTD

- Russell 2000 down -4.7% (down for the 6th straight week) to -9.5% YTD

- US Energy Stocks (XLE) down -5.2% to -5.6% YTD

- US Industrial Stocks (XLI) down -4.7% to -3.7% YTD

- US Consumer Staples (XLP) up +0.4% to +6.1% YTD

That’s right. In addition to the Long Bond (Treasuries), Munis, and Cash, we’ve noted in our most recent Macro Themes slide deck that Consumer Staples (XLP) is as good as any place to hide as the world clamors for low-beta-big-cap-liquidity.

Typically, when Correlation Risk (commodities trading inversely to USD) is this high, Down Dollar pays the commodity bulls. But last week, that was only true for pockets of the commodity complex (Oil was -4.4%). In addition to Gold +2.4% last week:

- Coffee was up another +6.7% to +83.5 % YTD

- Palladium was +4.0% to +8.7% YTD

- Cocoa was +3.3% to +16.4% YTD

But I am thinking there are more hedge funds who are still carry trading oil futures with a levered long bias than there are 2 and 20 alpha dogs who are long Cocoa on the #Ebola trade.

In fact, if you look at how hedge funds are positioned from a speculative net futures and options perspective:

- Crude Oil still has a net LONG position of +299,755 futures and options contracts (vs. 6 month avg of +385,000)

- US 10yr Treasury still has a net SHORT position of -51,954 contracts (vs. 6 month avg of -15,000)

- SP500 (Index +E-mini) has a net LONG position of +48,616 contracts (vs. 6 month avg of -41,000)

We’re obviously on the other side of every one of these Consensus Macro positions (bearish on Oil, bullish on Treasuries, bearish on SPX), so it was a good week. But the bigger question is where do the US equity bulls (and Treasury bears) go from here?

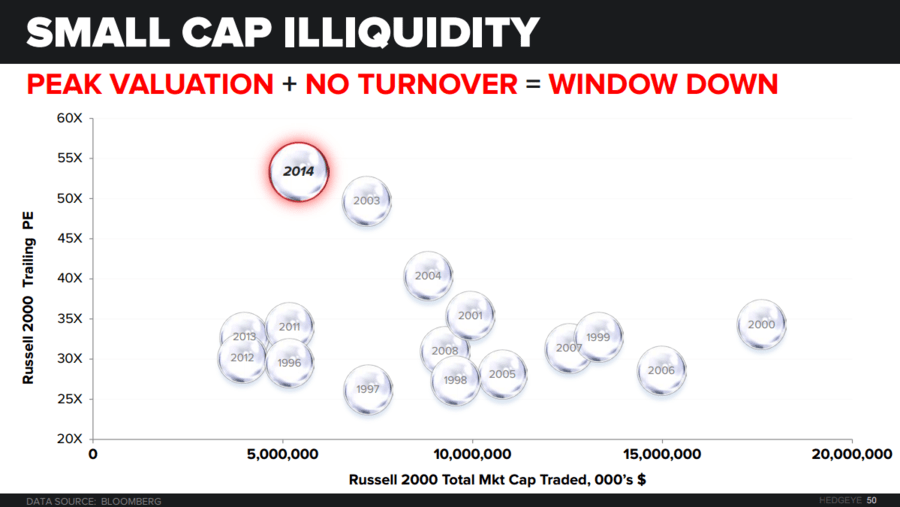

Within the small cap US equity #Bubble, there are a whole bunch of #bubbles we highlighted on our Q4 Macro Themes call (ping if you want the replay). And some of them play right into hedge fund consensus:

- Complacency #Bubble (slide 44)

- Levered Beta Chasing #Bubble (slide 45)

- Leveraged Speculation #Bubble (slide 46)

We can do a conference call with you to review all of these #bubbles, but the #Complacency one is really easy to show in terms of the number of days where the SP500 has had a > 1% move. After hitting an all-time YTD low, we just had 4 of those days, in a row!

Sure, markets scare people when they do that. I think I scared the hell out of some Institutional Investors in London with some of these slides too. Coming off the all-time lows in complacency, there’s never been this level of #VolatilityAsymmetry, ever.

While never-ever is a very long time – and I certainly don’t mean to be mean (or scare people) - I’d appreciate it if you took it easy on my inbox. My wife thinks of me as a cuddly Thunder Bay Bear, so be gentle with me.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1

RUT 1037-1086

VIX 16.85-21.67

USD 85.07-86.67

WTI Oil 83.99-88.64

Gold 1

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer