Below are Hedgeye analysts’ latest updates on our seven current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*Please note that we removed the British Pound (via the etf FXB) and Och-Ziff Capital Management Group (OZM) this week from our Investing Ideas list.

We also feature two institutional research notes which offer valuable insight into the markets and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

Small caps. Tech stocks. IPOs. And more. There are bubbles everywhere, and it’s why #Bubbles is one of Hedgeye’s three core Macro Themes this quarter.

IDEAS UPDATES

TLT | EDV | XLP

Montrez-moi l'argent!

Per Google Translate, the title of this note means, “show me the money!” in French. Why French? Because it is the language of love. And we love helping you make money…

Indeed, the week ended October 10th, 2014 was another great week for the slow-growth, yield-chasing trade we’ve been ardently advocating all year. To recap weekly performance:

- iShares 20+ Year Treasury Bond ETF (TLT): +2.0%

- Vanguard Extended Duration Treasury Bond ETF (EDV): +2.56%

- Consumer Staples Select Sector SPDR (XLP): +0.37%

Those performance figures represent material outperformance when benchmarked against traditional equity exposures like the S&P 500 (SPY) or Russell 2000 (IWM), which were down -3.04% WoW and -4.48% WoW, respectively.

Moreover, the widening spread of relative performance over the past month is supported by our view that both domestic and global economic growth is slowing.

- iShares 20+ Year Treasury Bond ETF (TLT): +4.3% MoM

- Vanguard Extended Duration Treasury Bond ETF (EDV): +5.86% MoM

- Consumer Staples Select Sector SPDR (XLP): +0.57% MoM

- SPDR S&P 500 Trust (SPY): -4.76% MoM

- iShares Russell 2000 ETF (IWM): -9.60% MoM

#alpha

There wasn’t really any meaningful domestic economic data to anchor on this week. In spite of this lack of data, global financial markets managed to go completely haywire on the Fed reminding everyone exactly what we’ve been forewarning all year:

US real GDP growth is unlikely to come in anywhere in the area code of consensus projections of 3-plus percent.

To recap the decidedly dovish minutes from the FOMC’s September 16-17th meeting:

- The minutes highlighted risks to the US economy and domestic inflation expectations from sluggish global growth and a stronger US dollar.

- The minutes suggested that the “considerable time” forward guidance and “significant underutilization of labor market resources” language may remain in the October FOMC statement.

- The minutes suggested that any changes to the board’s current guidance will present communication challenges and that caution would be required to avid an unintended tightening of financial conditions.

- Lastly, the minutes also downplayed concerns about potential risks to financial stability, which effectively means the Fed would be slow to react, if at all, to bubbly valuations in either the credit and/or equity markets with a less accommodative policy mix.

It is clear to us that market participants – many of whom have been anchoring on the Fed (which itself has a terrible track record at forecasting the economy) to guide their asset allocation all year – are interpreting the Fed’s dovish shift as signaling cause for concern with respect to the growth outlook. They should.

All told, we continue to think long-term interest rates are headed in the direction of both reported growth and growth expectations – i.e. lower. In light of that, we encourage you to remain long of the long bond.

GLD

Stick with the playbook. The USD-monetary policy hedge that is gold loves surprisingly dovish statements from FOMC members. We continue to lean on our internal model for predicting the change in the slope of 1) growth and 2) inflation, and the third part of the model is a policy input.

We’ve hammered this point all year with regard to our gold position, but the policy response from today’s central bankers has been one of the most predictable inputs into the model.

When growth and inflation are decelerating and consensus positioning suggests that growth will surprise to the downside, the monetary response will take a relatively dovish turn.

While Draghi was successful in taking down the Euro over Q2/Q3, the Federal Reserve will be dovish at the same time. Gold remains neutral from an intermediate-term TREND duration and will catch a bid on each incrementally dovish statement pressuring the outlook for the dollar.

Yellen’s commentary Wednesday on the minutes from the September 16th-17th Fed meeting indicated the global economy was weaker than expected and that policy members were worried that “FURTHER GAINS IN THE DOLLAR COULD HURT EXPORTS AND DAMP INFLATION.”

- The 10-yr yield tightened (Bonds rallied)

- The USD closed RED on the day after being in positive territory right before Yellen’s speech (-46bps)

- GOLD followed up Thursday with a +1.6% rally

LM

Legg Mason (LM) continues to surprise to the upside with results above Street expectations. During the most recent week, the company posted its monthly assets-under-management report with the strongest results in six months. In aggregate LM posted net new asset growth of $11.4 billion in September with all 3 of its major segments posting gains. While the company posted net new inflow of $800 million within its leading bond franchise and $8.8 billion within its money fund business, most impressive was the $1.8 billion inflow within its equity franchise.

While we continue to recommend a long position in Legg Mason on its underappreciated bond business, if the high margin equity franchise starts to generate above average results, our estimates could be too conservative leading to further upside. We currently estimate fair value on LM stock at $57-58 per share but if the Legg equity segment continues its recent trend line our estimates will prove too conservative.

OC

Earlier this week we hosted a follow-up call on the roofing market’s pricing and the current environment with Bill Carlin. Bill has over 36 years experience in the industry and previously held executive positions in OC’s roofing business.

Bill noted a more stable pricing environment for asphalt roof shingles, a significant improvement from year-on-year price declines in 2Q and most of 3Q 2014. Following OC’s poorly explained lack of pricing discipline in late 2013, prices and margins suffered.

The industry offers little fixed cost leverage, limiting the competitive benefits of seeking volume and market share over price (>80% non-variable cost). As long as competitors respect the value of oligopolistic pricing over market share, the industry should remain reasonably profitable.

The September 2014 price increase appears to be holding so far, transferring some pain to distributors. Unfortunately, high inventories across the channel may limit the 4Q benefit of better pricing. The survival of the price increase is a key issue for OC investors to track.

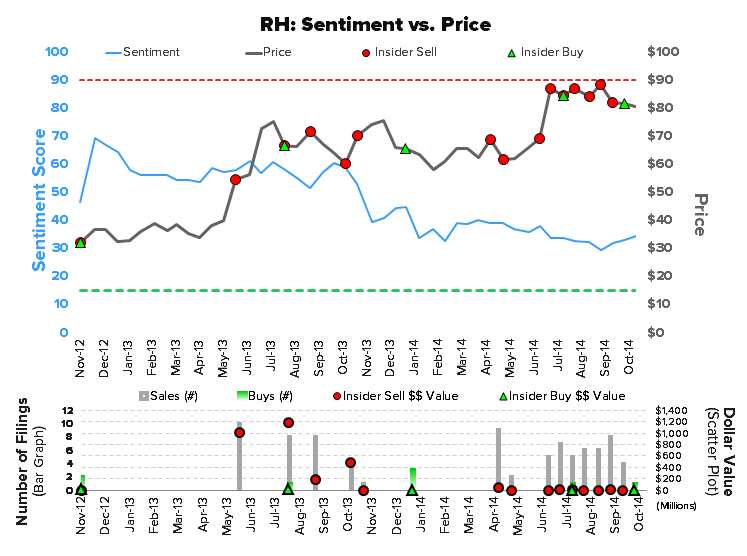

RH

Sentiment around RH ticked up slightly over the last month, which is largely due to an 8% reduction in short interest for the month. That’s not a major surprise in light of CEO Gary Friedman’s $2mm open market stock purchase, which sent a powerful signal to the market.

All that said, 28.6% of the RH float is currently held short. To put that into context, JC Penney, which one might think sets the standard for ‘investor hatred’ is sitting right at 29%. By comparison, Williams-Sonoma is at 6.8%, Macy’s is 3.1%, and Nike is 0.9%.

We think the fundamental story will play out in a way that will prove today’s short interest levels to never be retested.

* * * * * * * * * *

Click on each title below to unlock the content.

ICI Fund Flow Survey - Worst Quarter since 4Q 2012 for Equity Fund Flows

The most recent ICI fund flow survey rounded out the worst quarter for equity funds since 4Q 2012 and also reflected the dislocation at PIMCO.

Semiconductor Downcycle Confirmed by MCHP

Semiconductor Downcycle Confirmed by MCHP; All Chip Firms to be Impacted over the course of a couple quarters.