This note was originally published at 8am on September 26, 2014 for Hedgeye subscribers.

“We are the ones that we have been waiting for.”

-Alice Walker

“So,” how is everyone feeling this morning? I’m feeling great.

Since I’m running out of fresh content on both shorting the Russell 2000 (IWM) and buying the Long Bond (TLT), today I decided to weave a little Alice Walker (she wrote The Color Purple in 1982) with some perma-bear prepping.

If you don’t know what a #prepper is, look it up. On Wiki you’ll be re-directed to “Survivalism” and on the Googler you’ll get everything from “How To Build Your Own Bunker” to “Getting Ready For Barackalypse.” There’s always a bear market somewhere!

Back to the Global Macro Grind…

When you see me going all bear-mauler in the introduction to a research note, you buy/cover.

Yep, that’s pretty much the call this morning. I call it fading myself. If you didn’t buy and/or cover the swan dive that the SP500 took into yesterday’s close, you aren’t a real bull anyway.

Oh, and don’t forget to sell the “GDP is back” bounce by noon. Damn day-traders.

Forget the traders, how about them damn moving monkeys? Huh? Did Mucker call me a monkey? No. No. I would never call anyone names. I’m referring to this billion dollar app thing that I built for my 6yr old son called Monkey In The Middle.

Here’s how it works:

- It has a 1yr chart

- It has a simple moving avg

- It has a ticker box

And voila! That’s it. So easy a kindergartner can do it. He can analyze any ticker in the world, across asset classes!

Other than this being the most myopic single-factor interpretation of risk since the caveman throwing grass into the wind, the problem I foresee with this billion dollar idea is what happens when my son starts doing wacky stuff like multiplication.

Or, what if he figures out that moving monkeys are different if he uses a simple vs. an exponential moving average? Then my app is dead. But, in the meantime, you never know, yo. There’s an app for that too btw (it’s called “yo” – you say yo to me, I say yo back).

Serious question though, what is the 50-day Moving Monkey?

- Is it 1978 (exponential moving avg) or 1976 (simple moving avg) for the SP500?

- Or, is it 1151 (exponential moving avg) or 1148 (simple moving avg) for the Russell 2000?

I am not messing around here guys. If I am going to start building my family a legitimate bunker, I need to know what the signal is! Will using the exponential one help me front-run the simple ones? In the bush (with bears), all I need to do is out-run the last guy.

In all seriousness, the entire linear concept of using the 50-day is as ridiculous as the ideology that the Federal Reserve, European Central Bank, and Bank of Japan, can collectively bend gravity.

Moving along…

Does your iPhone bend? The stock did yesterday. It moved 2x what the market did, signaling immediate-term TRADE oversold within its bullish intermediate-term TREND setup. “So” I signaled buy AAPL (Apple) yesterday.

If we get the Q2 “GDP is back” bounce (newsflash: next week it will be Q4), I want to own the real bubbly stuff. Remember when The Facebook (FB), Apple (AAPL), and BABA had a projected $1 TRILLION in combined cap? I do. That may have been the top.

Tops are processes, not points. And the thing about the real bubbly ones is that you can risk manage them for a little while with a bullish bias (commonly called buying the damn dip). But there will come a time when they pop. Try it at home – those don’t bounce.

This is where I use my immediate-term Risk Range process (sorry Jack, our app doesn’t have real-world application!):

- SP500 signals immediate-term TRADE oversold at 1962, within a bullish intermediate-term TREND

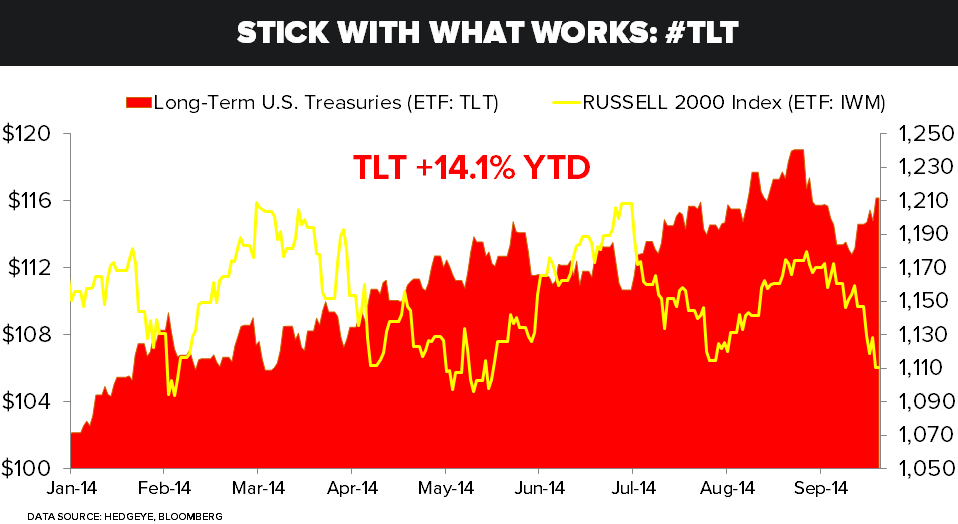

- Russell 2000 signaled immediate-term TRADE oversold at 1104, within a bearish TREND

- Front-month VIX signals immediate-term TRADE overbought at 15.92, within a bullish TREND

In other words, both volatility and the SP500 are bullish on an intermediate-term duration and the Russell 2000 small-cap #bubble is bearish across all durations. “So” on the oversold signals, you keep your small cap shorts on and buy big cap liquidity (AAPL).

If you’re longer-term, and not into managing the immediate-term risk of the range… and are right freaked out about something like the #Quad4 (US growth and inflation slowing at the same time), #preppers have a ton of stuff to sell you. Someone should definitely IPO that!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.42-2.58%

SPX 1962-1988

RUT 1104-1138

VIX 13.48-15.92

USD 84.64-85.53

Gold 1209-1250

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer