HEDGEYE TV

McCullough: Russell 2000 Is "Definitive Bubble"

In this brief excerpt from Friday's Morning Macro Call, Hedgeye CEO Keith McCullough reiterates his opinion that small cap stocks are in a bubble.

Semi Stocks Facing Risks?

Hedgeye semiconductor analyst Craig Berger discusses a weak pre-announcement from one company in the sector and looks at growing risks for other names in the chip space.

HEDGEYE PODCAST

London Calling

We caught up with Hedgeye CEO Keith McCullough in between investor meetings in London. Keith tells us what’s on the minds of those investors.

CARTOON

Hedgeye + $TLT = LOVE

As the 10-year yield drops back below 2.40%, we reiterate our non-consensus, best macro long idea of the year: Long the Long Bond.

Beware of #QUAD4

Hedgeye's Macro Team, led by CEO Keith McCullough recently hosted its quarterly Macro Themes conference call in which it detailed the THREE MOST IMPORTANT MACRO TRENDS it has identified for 4Q14 and the associated investment implications. At the top of the list is #Quad4. Our models are forecasting a continued slowing in the pace of domestic economic growth, as well as a further deceleration in inflation here in Q4. The confluence of these two events is likely to perpetuate a rise in volatility across asset classes as broad-based expectations for a robust economic recovery and tighter monetary policy are met with bearish data that is counter to the consensus narrative.

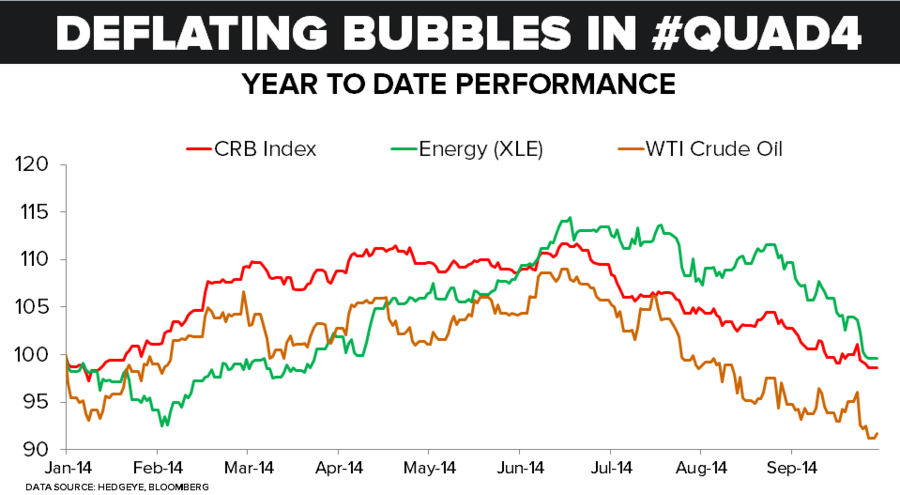

CHART

Deflating #BUBBLES in #QUAD4

Exorbitant Privilege (Fed Remittances to the U.S. Treasury)

Energy Price Sensitivity (Wildcatters Energy E&P Index)

As you can see in today’s chart, the Thomson Reuters Wildcatter’s Index (small and mid-cap E&Ps) has retreated -33% from its June YTD highs. If you top-ticked that move, it was the same day you shorted oil at the 2014 highs.

POLL OF THE DAY

Oil Prices

With WTI crude oil prices trading around $90/barrel, we wanted to know what’s the likeliest next stop?