More Sub-300k Thoughts

The labor market is chugging along with seasonally-adjusted initial jobless claims tracking well inside of the magic 300k line, which represents a frictional floor of sorts. We've shown in recent weeks that when claims breached 330k to the downside in the last two economic cycles, the market has continued its upward march for another 31 and 45 months. This go-around, we're currently at 8 months suggesting the market may not yet be done with its rally.

Conversely, the fact that we're sub-300k also represents a warning call of sorts as it has historically signified that we're in the proverbial 8th inning of the rally. Moreover, there's no guarantee that this cycle will play out similarly to the last two, especially considering the less-than-robust sample size (n = 2). As such, we'd be keeping Financials exposures on a relatively short leash from a big picture standpoint and we'll continue watching the labor data closely for any signs of negative inflection.

All that being said, so long as the good times keep rolling, we continue to like unsecured consumer lenders like Capital One (COF) and Discover (DFS) on the long side. Resurgent credit card loan growth dynamics coupled with stable credit quality metrics should combine to push estimates higher and potentially expand the multiple by a point or two.

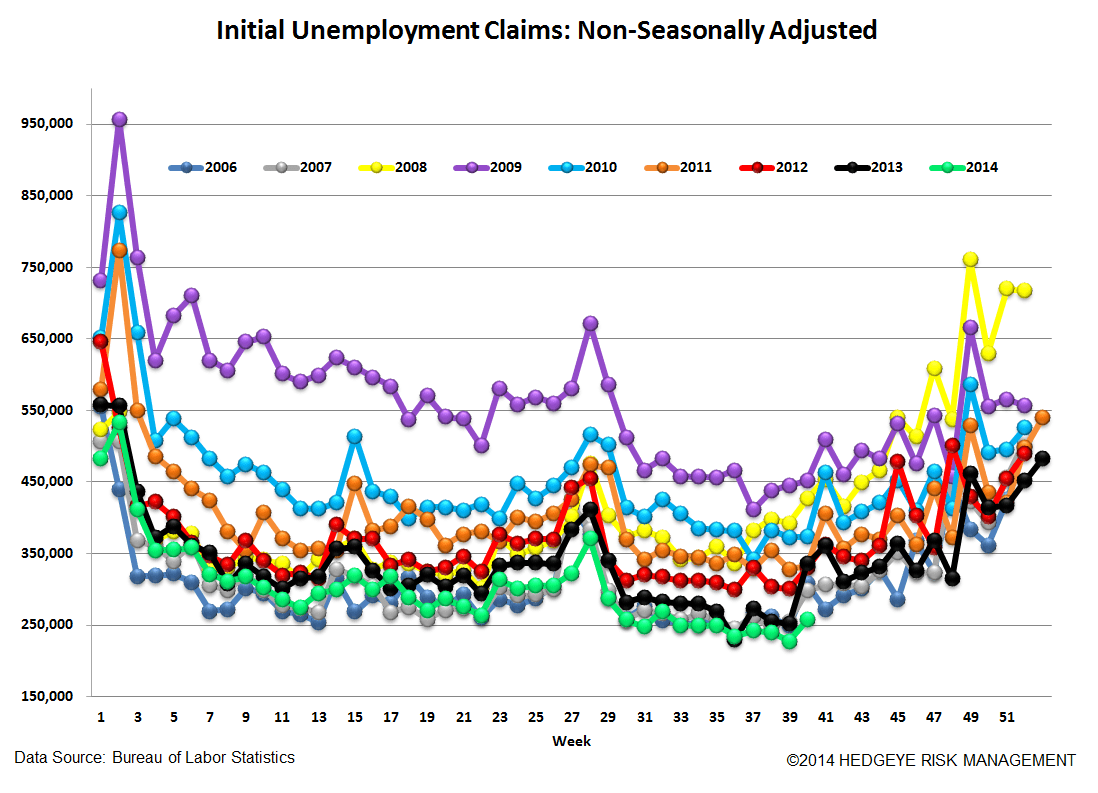

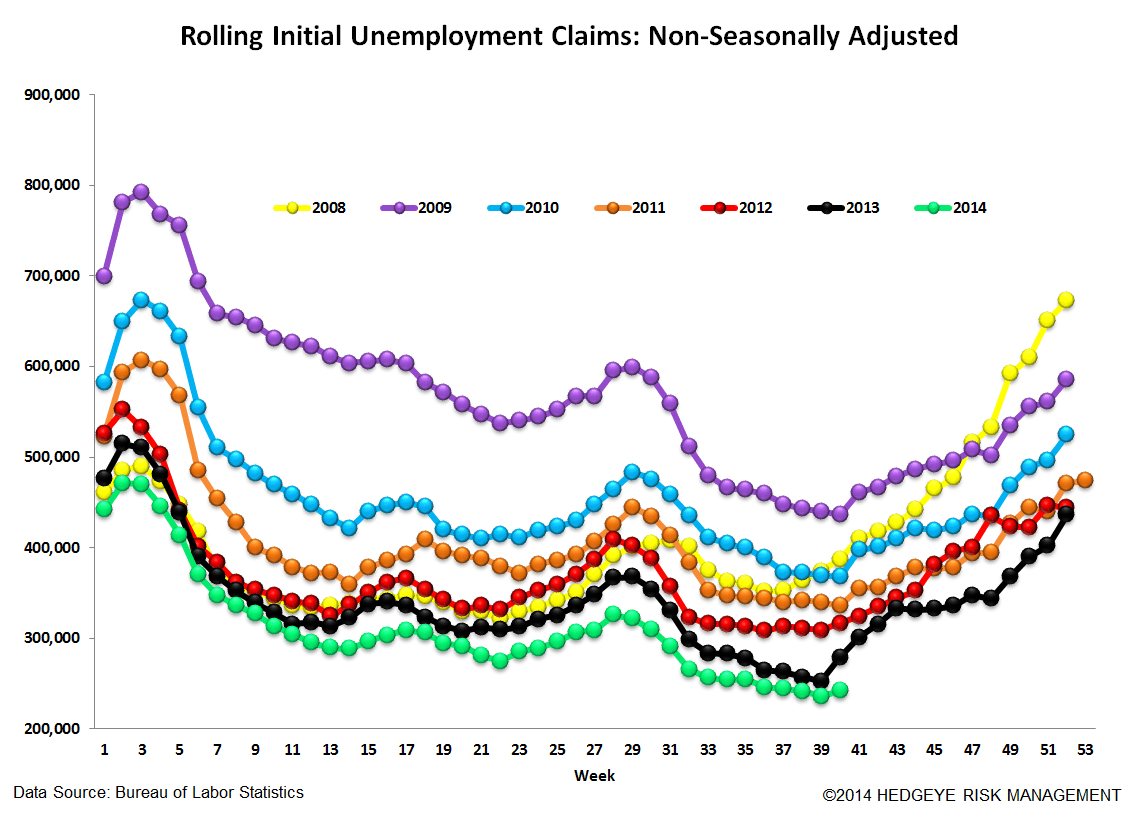

The Data

Prior to revision, initial jobless claims were unchanged at 287k WoW, as the prior week's number was revised up by 1k to 288k.

The headline (unrevised) number shows claims were lower by 1k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -7.25k WoW to 287.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -13.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -6.5%

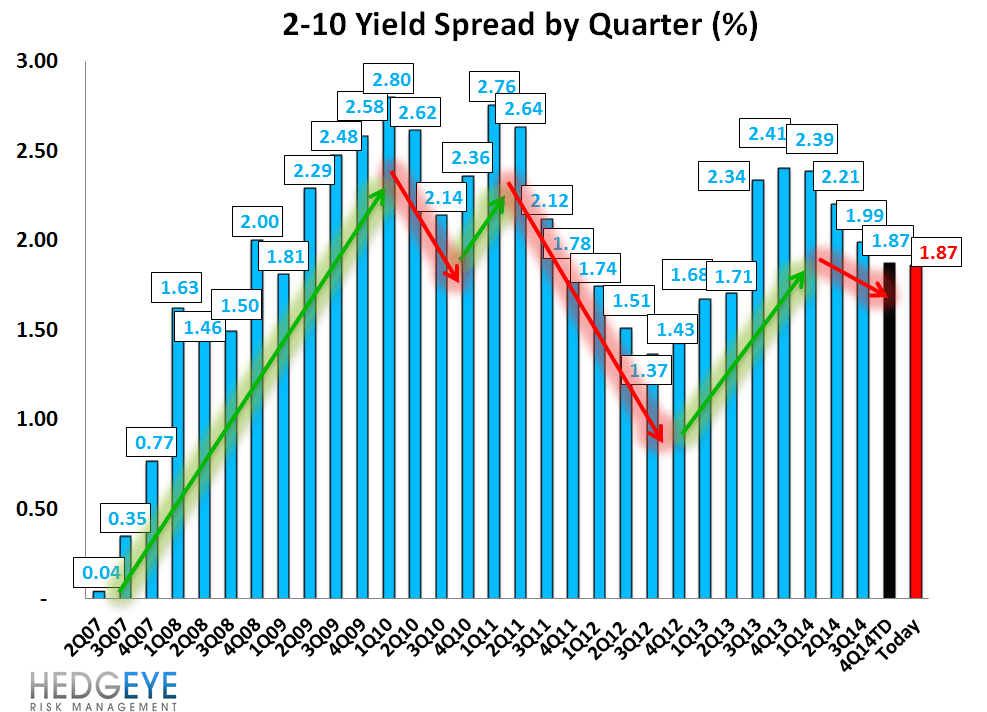

Yield Spreads

The 2-10 spread fell -1 basis points WoW to 187 bps. 3Q14TD, the 2-10 spread is averaging 187 bps, which is lower by -12 bps relative to 2Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT