EVENTS TO WATCH

Thursday (10/9)

FDO - Earnings Call: 5:00pm

COMPANY HIGHLIGHTS

GPS - Gap Inc.’s Glenn Murphy to Pass Reins to Digital Leader Art Peck as Next Chief Executive Officer

- "Gap Inc. announced that Art Peck, the president of its Growth, Innovation and Digital division, has been selected by the Board of Directors to succeed Glenn Murphy as the company’s next chief executive officer, effective February 1, 2015. Murphy and Peck have worked side-by-side for the better part of a decade as Gap Inc. dramatically improved its financial performance while expanding globally."

Takeaway: This is so bad for Gap, on many levels. The reality is that Murphy is too good for the Gap -- at least the Gap that he helped create. Since he joined the company in 2007 (at the age of 45!), he engineered a 15% EPS growth CAGR on a top line that only grew about 1%. GPS was never a top line growth story, and Murphy knew that. But he freed up 500bps in operating margin, and subsequently fed accelerated share repo, which drove earnings and the stock. But we've sensed for the better part of a year that Murphy took the company has far as he could operationally, and now is at a point where he has to worry about things like fashion (clearly not where he wants to be). We won't say that Gap is in trouble without him, but that Gap is likely in trouble, which is why he is leaving. The speculation, of course, is where he will go. It's uncanny that JCP's Mike Ullman reiterated yesterday that a CEO transition is on the front burner, and then just 8 hours later Murphy announces that he's leaving GPS. We think that JCP is a big step down for him, but if the money is right, we can't rule it out. If, by the grace of the retail Gods (and a big check), JCP were to get Murphy, it would be an absolutely huge hire.

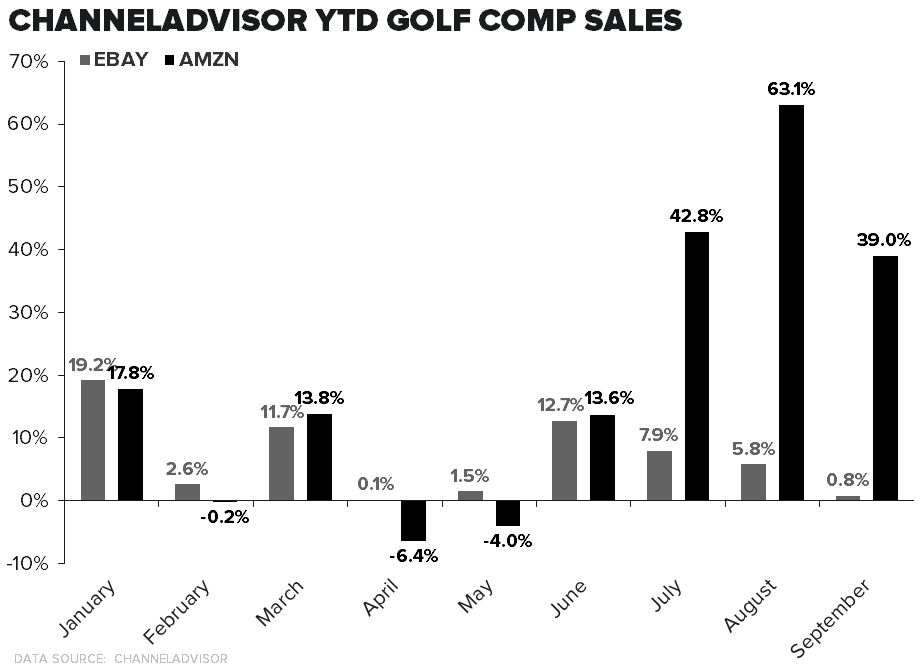

Negative Datapoint for AMZN, Positive for EBAY -- ChannelAdvisor Comp Sales

Takeaway: ChannelAdvisor works with a host of 3rd party sellers who use the AMZN and EBAY marketplaces and uses the sales results from its clientele to back into these monthly comp numbers. In September, AMZN had its first sequential deceleration of 2014. At the same time EBAY saw its first acceleration since March, reversing the large divergence seen between the two during 2014. EBAY marketplaces, which is 52% ($8.3B) of current EBAY revenue at 82% gross margins, will become its own company with the PayPal spinoff expected next year.

Golf: Amazon golf comps slowed but with a solid 39% gain. Inventory remains high in the space, apparently, as Amazon golf sales are a good proxy for excess inventory in the channel. Still not good for DKS .

TGT - Target’s new CEO makes Canadian turnaround his priority

- "The new chief executive officer of Target Corp. is taking a hands-on approach to fixing the company’s problems in Canada, making regular trips to check stores here as he heads into the all-important holiday season."

- "Brian Cornell said in an interview on Wednesday he will travel to Canada from Target’s head office in Minneapolis on a 'regular' basis to oversee the turnaround efforts."

- "He has 'put on pause' the company’s earlier plan to appoint a non-executive chairperson with domestic experience to oversee the troubled Canadian operations."

Takeaway: What does it say about Canada, when a new CEO 8-weeks into the job has put a part of the business that accounts for about 7% of total company square footage and 2.5% of revs at the top of the priority of list? Sure it's disproportionally dilutive to earnings, taking down numbers by about 20%, and we have a hard time seeing how it ever turns a profit. But, there is a lot that needs to be fixed in the core US business that needs the CEO's attention. Like un-boxing itself from the competitive set its developed over the past 5 years as it made its move into groceries, pushed the RedCard, and lost its cache in apparel and home. Now it finds itself right in the middle of five unique competitors - 1) WalMart, 2) Department Stores, 3) Dollar Stores, 4) Supermarkets, and 5) Amazon. If there is one thing we take away from this article it's that Cornell has a lot of wood to chop on the HR front. That means that he's spent the past two months meeting the organization, and either he thinks changes need to be made, or gaps need to be filled. It's probably both.

OTHER NEWS

SHLD - Sears stock down again on reports of halted vendor shipments

- "Sears Canada stock plunged by eight per cent and U.S. parent Sears Holding Corp. was down by 15 per cent after reports that a vendor had stopped shipments to U.S. stores."

- "Bloomberg News said Wednesday that a Sears vendor was halting shipments because it couldn’t obtain insurance to ensure it would be paid for its products."

M - Bloomingdale's goes high-tech at new store in Palo Alto, California

(http://www.chainstoreage.com/article/bloomingdales-goes-high-tech-new-store-palo-alto-california)

- "Bloomingdale’s goes high-tech with the opening of its store in Stanford Shopping Center, Palo Alto, California, on Oct. 10. In a nod to the digitally-savvy locale, the three-level, 125,000-sq.-ft. store features a wide array of high-tech innovations to make shopping easier. Among the offerings: state-of-the-art smart fitting rooms, a buy online, pick-up in-store feature and the launch of same-day-delivery where shoppers located within a 15-mile radius from the store can buy select merchandise on bloomingdales.com and have the product delivered within a five-hour window. And all sales associates are outfitted with mobile checkout devices."

H&M's & Other Stories Opens in New York

- "H&M’s new format, '& Other Stories,' is starting a new chapter."

- "The chain on Friday will open its first store in the U.S., in SoHo, as well as a U.S. e-commerce site."

- "The 6,400-square-foot store is at 575 Broadway. It has two entrances: on Broadway, which attracts a mixed audience, including tourists, and on Mercer Street, which is filled with designer and luxury brands."