TODAY’S S&P 500 SET-UP – October 9, 2014

As we look at today's setup for the S&P 500, the range is 45 points or 1.98% downside to 1930 and 0.31% upside to 1975.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.87 from 1.87

- VIX closed at 15.11 1 day percent change of -12.15%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Init. Jobless Claims, Oct. 4, est. 295k (prior 287k)

- 8:45am: Bloomberg Oct. U.S. Economic Survey

- 9:45am: Bloomberg Consumer Comfort, Oct. 5 (prior 34.8)

- 10am: Wholesale Inventories, Aug., est. 0.3% (prior 0.1%)

- 10:15am: Fed’s Bullard speaks in St. Louis

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: ECB’s Draghi, Fed’s Fischer speak in Washington

- 11am: U.S. announces plans for auctions of 3M/6M/1Y bills

- 1pm: U.S. to sell $13b 30Y bonds in reopening

- 1:10pm: Fed’s Tarullo speaks in Washington

- 1:15pm: Fed’s Lacker speaks in Asheville, N.C.

- 1:30pm: Fed’s Fischer speaks in Washington

- 3:40pm: Fed’s Williams speaks in Las Vegas

GOVERNMENT:

- Senate, House out of session

- President Obama speaks on economy

- 8am: Financial Services Roundtable holds Global Financial Summit, participants incl. CFTC Chairman Timothy Massad

- 9am: IMF Managing Director Christine Lagarde, World Bank President Jim Yong Kim preview IMF, World Bank annual mtgs

- 9:15am: Sec. of State John Kerry, U.K. Foreign Sec. Philip Hammond at Boston global climate change, clean energy event

- 11am: ECB President Mario Draghi speaks at Brookings Institution; Draghi, Fed Board Vice Chairman Stanley Fischer follow w/conversation

- 3pm: Homeland Security Sec. Jeh Johnson at CSIS discussion on border security

- U.S. ELECTION WRAP: Abortion Issue in N.H.; Kansas Sen. Debate

WHAT TO WATCH:

- Alcoa Earnings Rebound as Aluminum Use Rises in Autos, Aerospace

- Barclays to Pay $20m to Settle Libor Suit, Plaintiffs Say

- McClendon Said to Weigh Bid for Freeport’s California Assets

- Gap Tumbles After Saying Murphy Will Step Down as CEO Next Year

- AMD Appoints Lisa Su Chief Executive, Replaces Rory Read

- Twitter News Head Schiller Exits as Executive Turnover Continues

- Icahn Says He Plans to Send Open Letter to Apple CEO Tim Cook

- Russia Moves Ruble Band Most Since March, Spends $1.85b

- Nurse Tested for Ebola in Australia After Volunteering in Africa

- Worldwide PC Sales Declined 1.7% in Third Quarter, IDC Says

- Morgan Stanley Bankers Poised for Biggest Wall Street Bonus Bump

- Tesla to End ‘The D’ Suspense to Stay Ahead on Electric Autos

- Boeing Predicts Demand for 1,340 New Planes in Northeast Asia

- Brooklyn Home Prices Reach Record as New York Buyers Bid Higher

- CEOs Tout Reserves of Oil, Gas Revealed to Be Much Less to SEC

- Hong Kong Protest Leaders Say They May Walk Away From Talks

- China Outlines Plans to Ease Capital Controls, Boost Use of Yuan

- Elevation Partners Said to Tell Investors No New Fund Is Coming

- Google Asks Supreme Court to Decide Oracle Suit: Reuters

- Citigroup Set to Return $16m to Customers After Pact: WSJ

- Fidelity 1 of 13 Fin Groups Targeted by JPMorgan Hackers: FT

EARNINGS:

- Lindsay (LNN) 7am, $0.56

- PepsiCo (PEP) 7am, $1.29 - Preview

- Helen of Troy (HELE) 4:01pm, $0.73

- Barracuda Networks (CUDA) 4:15pm, $0.04

- Family Dollar (FDO) Aft-Mkt, $0.77 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- CEOs Tout Reserves of Oil, Gas Revealed to Be Much Less to SE

- Brent Crude Declines as Germany Nears Recession; WTI Steady

- Sugar Shortage Seen Looming by Drake Amid Drought in Brazil

- China Battles GMO Unease From Field to Dinner Table: Commodities

- Noble Said to Hire Gazprom’s Kapic to Trade European Power, Gas

- EU Carbon Contango Crushed as Yield Is Better Than ECB: Vertis

- Copper Advances Most in Three Weeks as Dollar Continues to Slide

- Alcoa Earnings Rebound as Aluminum Use Rises in Aerospace

- Gold Futures Rise to Highest in More Than 2 Weeks on Fed Minutes

- Food Prices Slide a Sixth Month to Four-Year Low as Grains Fall

- Solar’s $30 Billion Splurge Proves Too Much for Japan: Energy

- Investors Shun World’s Richest Mineral Store in South Africa

- Nickel Seen by ANZ Rising in Next Few Months on Slower Exports

- Aurubis Raises Copper Premium for Europe by 4.8% for Next Year

- Rio’s Bullish Iron Ore Outlook Bolsters Glencore Case for Bid

CURRENCIES

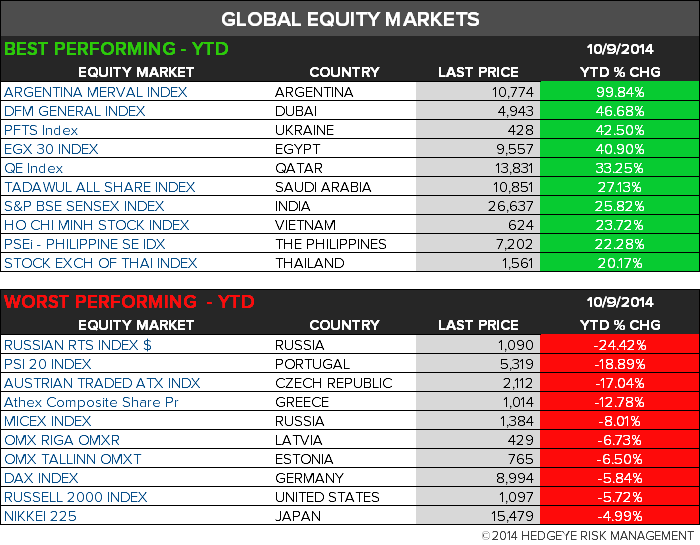

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

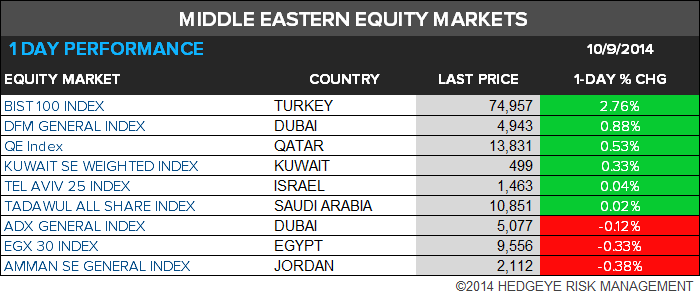

MIDDLE EAST

The Hedgeye Macro Team