Conclusion: The weaker September trends are clearly taking center stage as it relates to the stock. But we wonder if people are internalizing that the company’s financial plan – its first believable one in at least five years – suggests that JCP will be squarely profitable in 2017. Sales productivity going from $108 to at least $135 (on the low end), and earnings between $0.44 and $1.05 -- keeping in mind that the Street is at a loss of ($0.17). One of the key things we needed to see from JCP (see comments below) was a line in the sand for when the P&L would turn a profit. While they did not spell it out explicitly, when you build up the components of the model the message is clear -- profit by '17. Tack on the fact that Ullman seemed to strengthen his posture that finding a new CEO is a top priority, and we think that the story strengthened today, not weakened (as the market suggests). Are we enamored with the stock here? No. We’re not. It’s trading at a 23x a base-case earnings number three years out, and 22x current year EBITDA. We have a real hard time finding any valuation support on this name, and quarterly volatility in the model is intense. But we think that JCP’s revenue and margin targets are defendable, and that it will continue to be a net share gainer on a consistent basis for the next three years (unless a new CEO derails the plan – it’s happened before). We’re comfortable enough sitting back and watching this one grow into its multiple, or getting involved if it gets any cheaper.

DETAILS

It’s stating the obvious that the market did not like JCP’s lower comp guidance for the quarter (low-single instead of mid-single digit comps). While we’d call the sell-off in the name today excessive given that company stuck with margin guidance and annual sales/earnings guidance, the reality is that nothing really shocks us anymore with how this name trades in reaction to near-term data points (particularly given an infinite multiple on current earnings and 30% of the float held short).

But we are surprised that people are not talking more about the company’s long-term financial targets.

1) First off, let’s simply acknowledge the fact that JCP finally has long-term financial targets for the first time in more than five years.

2) Second, JCP outlined $3.5bn in revenue as its internal goal by 2017. That equates to $148 per square foot, which tops the $140/ft we’ve been talking about since last year. The level that the company set with the Street was 60% of this level – that’s $2.1bn in incremental revenue, or a total of $135 per square foot.

3) JCP also gave a Gross Margin target between 36.5% and 37.0%, versus 29.5% last year and a current run rate of 34.5%. That’s on top of SG&A that should be held relatively constant, and a slight decline in interest expense as $300mm in maturities come due.

4) Add that all up, and you get to EPS of $0.44 on the low end, and $1.05 if the company hits its internal goal.

We’re certainly not betting on the company hitting its internal goal – not by any stretch. But let’s keep in mind that the consensus has JCP losing ($0.17) in 2017. The company just took up expectations by anywhere between $0.61-$1.22.

Still a lot to digest from the day’s events. We’ll be back when warranted.

10/06/14

JCP – What JCP Needs To Say

Takeaway: There’s a gap between what JCP should say vs. what it will say on Wednesday. All it needs to say is “break even in 2016.”

Ullman & Co have a pretty easy job at this Wednesday’s JCP analyst meeting. Expectations are low, and this company has not articulated a long-term plan since Ron Johnson took center stage and then proceeded to destroy $8.6bn in shareholder value – or 87% of JCP’s market cap. Talk about easy comps. We don’t think it will take much to get people excited.

There’s sure to be information overload on Wednesday, but there’s only a few simple messages we want to hear.

- “Sales productivity of $140 by 2016”, up from $108 today. This includes Store productivity going from $98 to $120, and JCP adding another $500mm in e-commerce sales (much of which we think will come from Kohl’s).

- “Positive Earnings by 2016”. This would actually be a huge news event for JCP given that the consensus has JCP losing money…well…forever. We think that positive in 2017 is very likely, but 2016 is certainly possible.

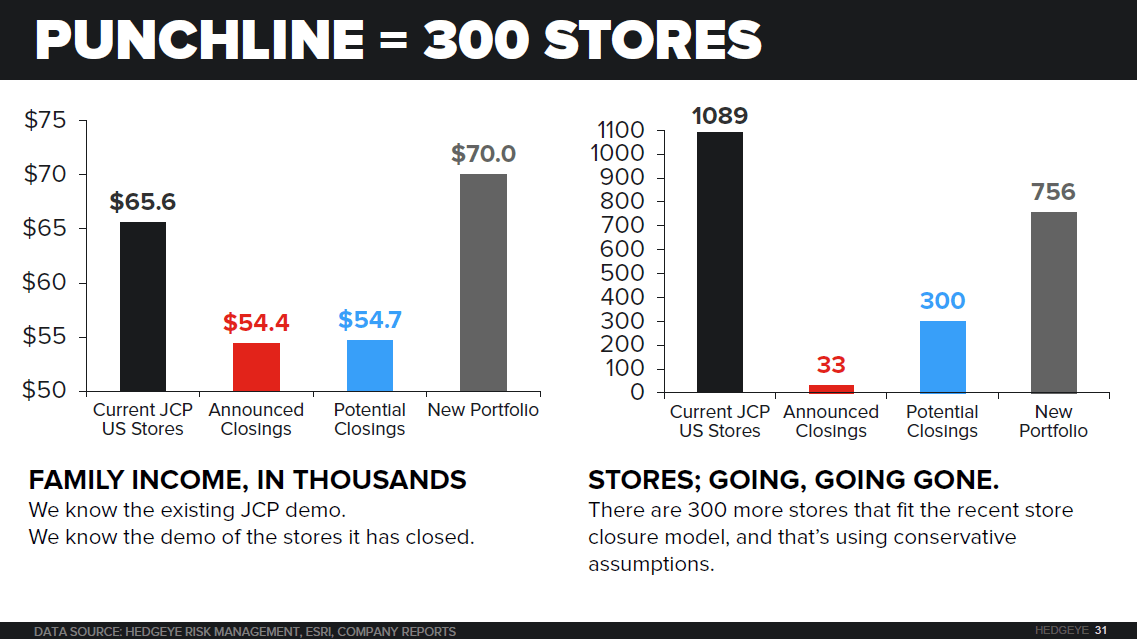

- “Close 300 Stores”. Our math suggests 300 stores that need to be closed. We identified each of them in an analysis in May, and outlined some of the salient points below. We’d peg a 25% or less chance in getting this announcement on Wednesday. But we don’t see how Ullman can stand up there with a straight face and say that the company is currently running the optimal fleet size. It’s too close to the holiday for him to send a message to 25% of his rank and file that they might not have jobs anymore. We expect some acknowledgement of a small number of store closures on Wednesday, with a far greater announcement coming in the new year.

POSITIVE JCP DATAPOINT FROM OUR CONSUMER SURVEY

We’re in the process of compiling one of our Deep Dive Black Books and will be hosting a call next week. We’ll be discussing several things, including…

a) What the Department Store landscape should look like (operationally and financially) when we enter the next economic cycle.

b) Detailed Revenue analysis for all the Department Stores – by category, consumer, and demographic.

c) Detailed Results of our latest Consumer Survey on the department stores.

d) Real estate deep dive – including overlap with stores that are likely to go away.

e) E-commerce – growth and profitability prospects for the companies and industry.

Here’s one chart as it relates to JCP that we thought was worth sharing. Each time we conduct our Consumer Surveys, one thing we ask the 1,000 department store shoppers is to rank which are their ‘go to’ stores in each product category. We don’t necessarily look at the results compared to one another, as Macy’s will obviously get more votes across the board than Lord & Taylor or Bon-Ton, for example. But we can gauge the incremental change for each company from one survey to the next (in this instance, 1Q14 to today).

There’s only one company that improved its ranking in every single product category – and that’s JCP.

REAL ESTATE OVERVIEW

Here are a few select highlights of the JCP Real Estate Analysis we conducted in May.

1. Real Estate Approach: We did this analysis from the vantage point of a) optimizing JCP’s fleet, and b) seeing what the revenue impact would be for KSS. In order to properly assess the potential, we analyzed every JCP market to see where the most likely closures are, and whether or not they overlap with KSS. For starters, we did not simply map out store locations (a feat in itself) and draw a circle around each point on the map to gauge overlap by market. We mapped out a 15-minute driving radius around every store, which as you can see by the chart below is very different for every single store location in the country. This shows Tallahassee, FL, which has two locations where JCP and KSS overlap perfectly, and another location where JCP exists without KSS as a competitor. We did this in every market in the US.

2. Productivity Analysis. This next chart shows us what the implied sales per square foot range is for JCP’s 1089 stores. What we know is that in the US, JCP has 0.47% share of wallet in apparel, home furnishings and other relevant retail goods across its portfolio in aggregate – again, we’re looking at all expenditures within a 15 minute drive of its stores. If we apply that ratio to each market, we get implied sales/square foot levels ranging from $8 to nearly $1,000 (Manhattan). We know that share is likely to vary by market, so we’re not trying to say that these are the exact productivity levels of each store. But directionally, we think we’re right. And that direction tells us that 782 stores, or nearly 72% of JCP locations, are running below the system average of $98/square foot.

3. 300 Store Closures: We think that JCP needs to close 300 locations, at a minimum. We know that the demographic profile in the surrounding area of JCP stores in aggregate is about $66k in annual household income. We also know that JCP just identified 33 stores that it is closing. We analyzed those locations, and the demographic profile is $54k annually – that’s 18% lower than the portfolio average. So we looked throughout the system of JCP stores and looked to see how many other stores fit that profile. There are 300. If these stores are closed, the average income statistic goes up for the whole portfolio by 7% to $70k. The 300 stores closed have implied sales/square foot of less than $38 annually. There are still almost 500 stores above $38 and yet still below the system average.

4. Revenue Impact of Closures. Our math suggests that these stores would only result in about $550mm-$600mm in revenue loss to JCP. Importantly, KSS only overlaps in 42% of these markets. Our research shows that KSS took about 19% of the $5.4bn in sales JCP hemorrhaged over the past three years. If we apply a 20% share gain level to this analysis for KSS, it suggests about $73mm, or less than 0.4% to KSS in comp. If you want to get more aggressive and assume that KSS takes 100% of that revenue (which WMT won’t allow) you’re looking at about 1.9% in comp to KSS. We think something far below 1% is closer to reality. Here’s the sensitivity analysis below.