TODAY’S S&P 500 SET-UP – October 8, 2014

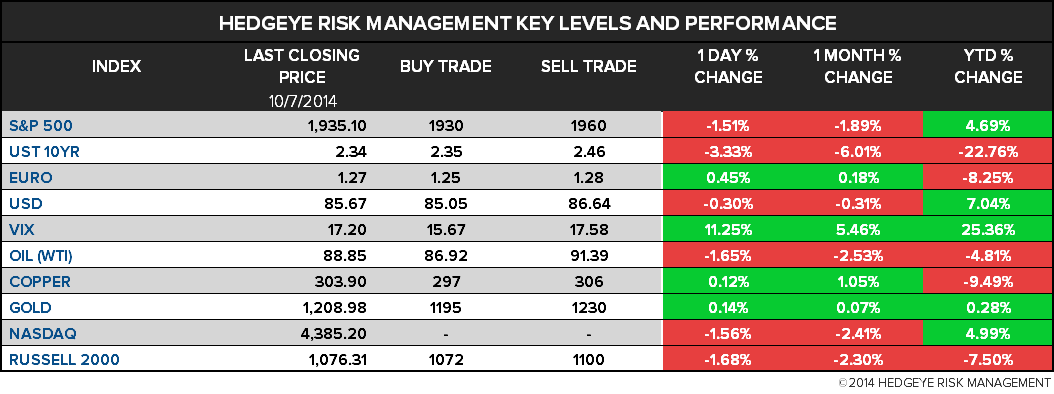

As we look at today's setup for the S&P 500, the range is 30 points or 0.26% downside to 1930 and 1.29% upside to 1960.

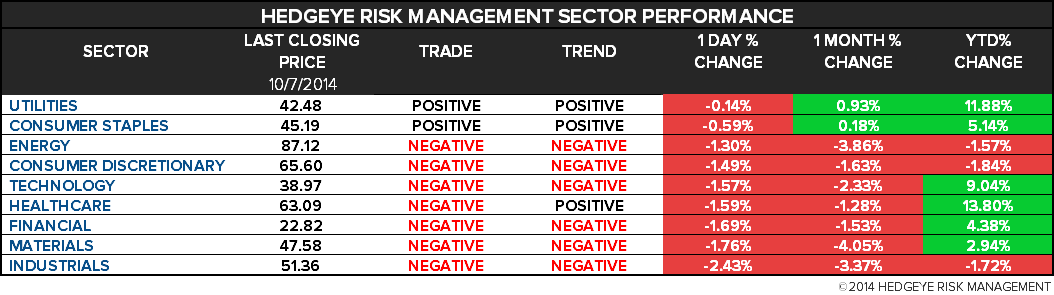

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.85 from 1.83

- VIX closed at 17.2 1 day percent change of 11.25%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Oct. 3 (prior -0.2%)

- 8:30am: Fed’s Evans speaks in Plymouth, Wis.

- 10:30am: DOE Energy Inventories

- 1pm: U.S. to sell $21b 10Y notes in reopening

- 2pm: Fed releases minutes from Sept. 16-17 FOMC meeting

GOVERNMENT:

- Senate, House out of session

- FCC deadline for replies on CMCSA/TWC Deal

- 10am: Supreme Court to consider arguments on whether workers at Amazon.com warehouses must be paid for time spent in security screenings after they clock out

- 2:30pm: Chinese Vice Minister of Finance Guangyao Zhu speaks at Peterson Institute talk on China-U.S. economic relations

- 4:30pm: Former Fed Chairman Ben Bernanke speaks on future of global economy at World Business Forum

- U.S. ELECTION WRAP: Kansas May Set New Trend; S.D. Crooning

WHAT TO WATCH:

- U.S. Said to Ready Charges Against Banks, Traders in FX Case

- Symantec Said to Explore Split Into Security, Storage Businesses

- Valeant Said to Plan Raising Allergan Bid Near December Vote

- Yum Cuts Profit Forecast as Chinese Food Scare Weighs on Sales

- Costco Profit Tops Estimates as Same-Store Sales Increase

- Russia Buys Rubles for a Third Day While Shifting Trading Band

- Marchionne Says He’s ‘Done’ After 2018 Plan for Fiat Chrysler

- Kurdish Protests Roil Turkey as Islamic State Attacks Kobani

- Facebook to Let Advertisers Target Users Based on Locations

- SolarCity to Finance Rooftop Systems in Shift From Leasing Model

- Chimerix’s Antiviral Drug Improved Survival in Josh Hardy Study

- Bard Said to Pay $21 Million in First Big Vaginal-Mesh Accord

- World Growth Eclipses Dollar as Concern for Lew, Manufacturers

- 18 Banks Said to Adjust Derivatives Contracts Practices: FT

- Fed Needs Plan to Sell Mortgage-Backed Assets, Lacker Says: WSJ

- San Francisco Supervisors Agree to Legalize Airbnb: SFGate

AM EARNS:

- Blackhawk (HAWK) 8:30am, $0.03

- Jean Coutu (PJC/A CN) 7am, C$0.29

- Monsanto (MON) 8am, $(0.24) - Preview

- RPM Intl (RPM) 7:30am, $0.78

PM EARNS:

- Alcoa (AA) 4:03pm, $0.22 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- London Metal Exchange Wins Appeal Over Rusal Warehouse Ruling

- Brent Drops to 27-Month Low on IMF Growth Cut; WTI Declines

- Gold Climbs on Demand From China After Holiday; Platinum Rallies

- Corn Retreats in Chicago as U.S. Harvest Seen Exceeding Forecast

- Narrow Price Gap Opens Door for African Oil Exports to U.S. East

- Arabica Coffee Slides in New York on Speculation of Brazil Rain

- China Steel Demand May Slow as Economy Becomes More Sustainable

- OIL DAYBOOK: EIA Crude Build Fcast; OPEC Basket Drops Below $90

- Northeast U.S. Homes to Pay Higher Prices for Less Gas in Winter

- Commodity ETP Outflows Totaled $1.8 Billion in Sept: Blackrock

- Gold With Iron Ore Seen Least Preferred Metals by Morgan Stanley

- OPEC Crude Below $90 Won’t Spur Immediate Output Cut: Julian Lee

- Nickel to Aluminum Decline on Demand Concern as IMF Cuts Outlook

- Indonesia Seen Losing $20B Mining Investment on Political Risk

- Rusal Says Will Seek to Appeal U.K. Court Ruling on LME Today

CURRENCIES

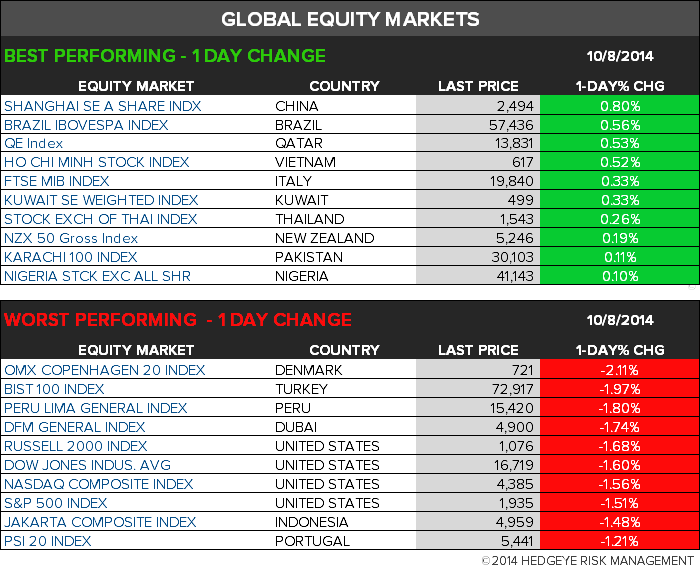

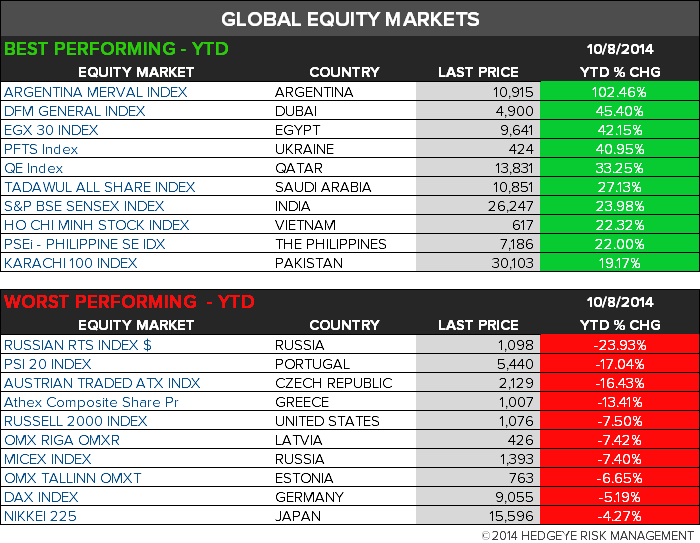

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team