Summary

We typically introduce the Hedgeye Industrials research process using the shipbuilding cycle and industry structure as an illustration. The discussion typically goes something like “after WWII, war related tonnage was converted to commercial use, but ships last for only, give or take, 30 years, so there was a replacement cycle in the mid-1970s”…and so on. But shipbuilding is not just an example of a capital equipment cycle and a flawed industry structure, it has also been, and will likely continue to be, a once in a career short opportunity.

Beyond the Fishfinder updates, we have only written on shipbuilding occasionally because not much happens that is relevant to our thesis. Basically, our view is that shorting South Korean shipbuilders should work for several years; the next move for investors is to buy Chinese shipbuilders in roughly 2030 (only partly kidding). Recently, however, there has been more action.

Industry Structure: Extremely Fragmented, Government Subsidized

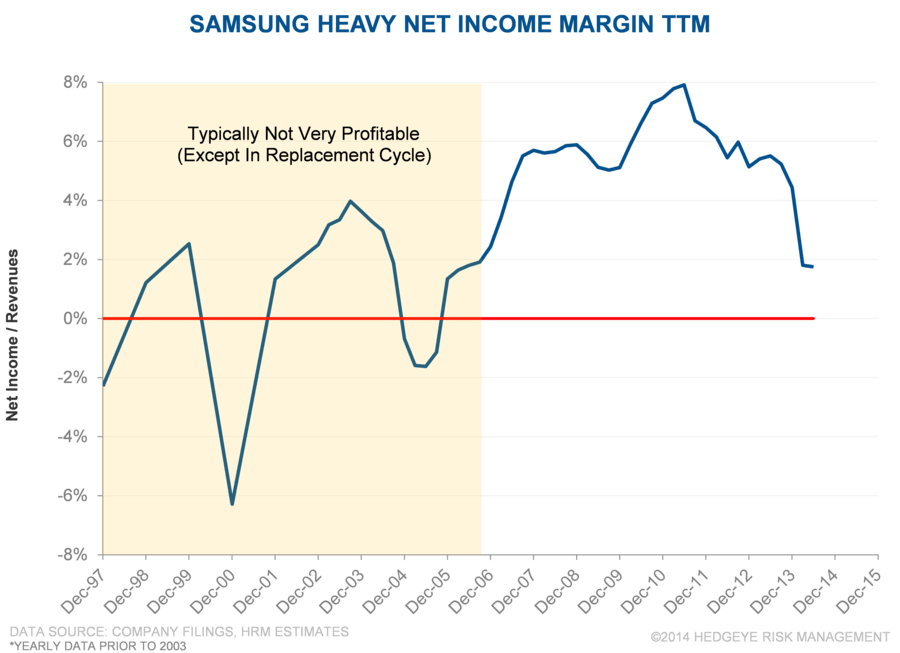

We focused on Samsung Heavy in our launch deck and subsequent notes because it had fewer non-shipbuilding exposures. Samsung Heavy shares have dropped about 45% in the past year, significantly underperforming the KOSPI. Below, we provide some updates.

Key Highlights

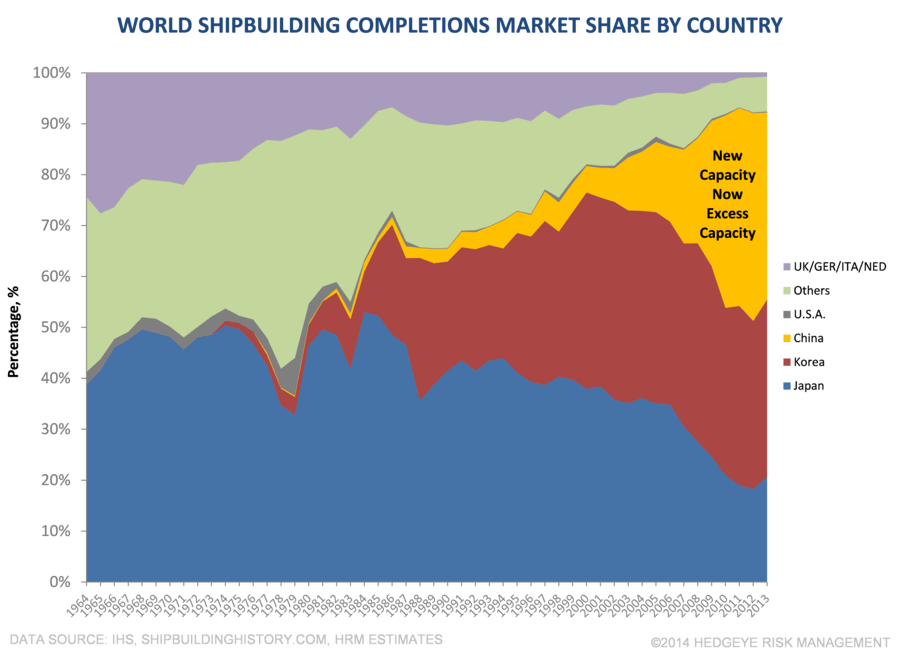

- Chinese Shipbuilder ‘Bailout’: Excess shipbuilding capacity has largely been of a massive ramp in Chinese capacity. To us, it has become clear that China isn’t exactly planning to layoff shipbuilding employees. For instance, the handling of China Rongsheng, a theoretically private competitor, has consisted of local government support for the company while it does a restructuring analysis due in mid-2015. Apparently, the government is looking to merge the shipbuilder with a financially stronger competitor at some point, but maybe not. This is consistent with our view that the industry is more of an employment project than a viable profit center. Excess Chinese capacity will likely continue to weigh on industry pricing.

- Pressure on Margins, Pricing: SHI’s orders have been below management expectations this year and excess capacity has pressured industry pricing. Given the intense competition in standard ship categories, Samsung Heavy and others South Korean builders have competed for complex offshore energy-related orders (drill ships, FPSOs, etc). Unfortunately, the margin on these complex ships has been poor. Costs and schedules have proved more difficult to forecast than those of more traditional products. As a result, SHI’s margins have suffered so far in 2014. We would expect that earlier orders in backlog carry better pricing than current orders, setting the stage for ongoing margin pressure.

- Not Just Samsung Heavy: Obviously, Chinese shipbuilders are experiencing stress, but other South Korean firms have also seen margin degradation.

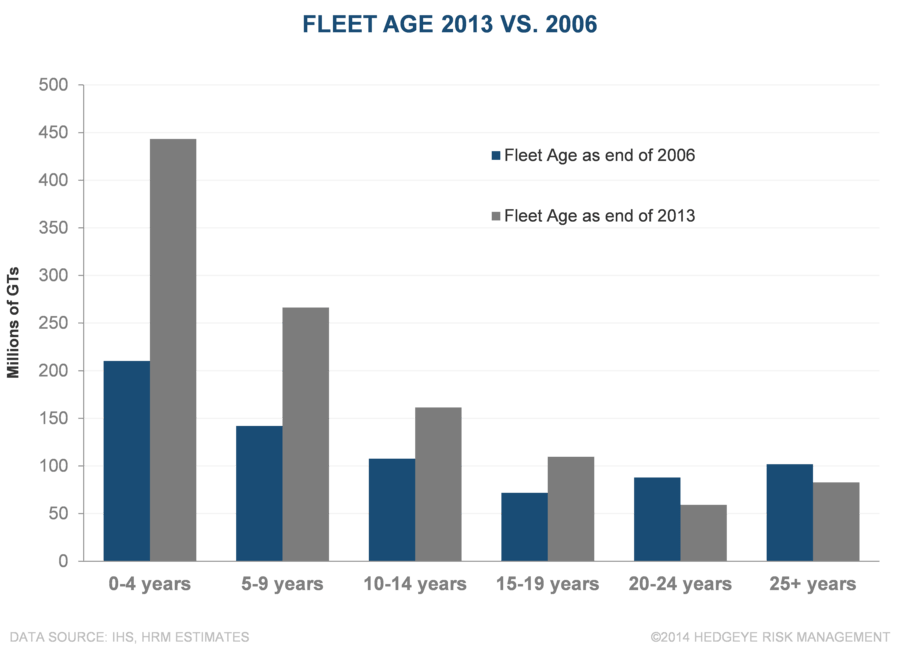

- Last Time It Took 13 Years To Bottom: The global shipping fleet is young, having just completed a replacement cycle. Energy and bulk commodity prices have seen pressure in recent months, with customers in those end-markets driving demand. We expect pricing pressure from weak demand, excess capacity, and government subsidization to depress SHI’s profitability for years. In the last replacement cycle, deliveries peaked around 1975 and bottomed in roughly 1988.

- Low Profitability, Except During Peak Demand: Aside from the boom years of the replacement cycle, shipbuilding seems more like an employment scheme than a profit-making enterprise.

- Still Lots of Value to Lose: Given that the South Korean shipbuilding industry has lost significant ground to Chinese competitors in the last decade, we would expect valuations to compress below pre-boom norms. We also expect that Chinese shipbuilders will further develop capability in drill ships, FPSOs, and other more specialized vessels.

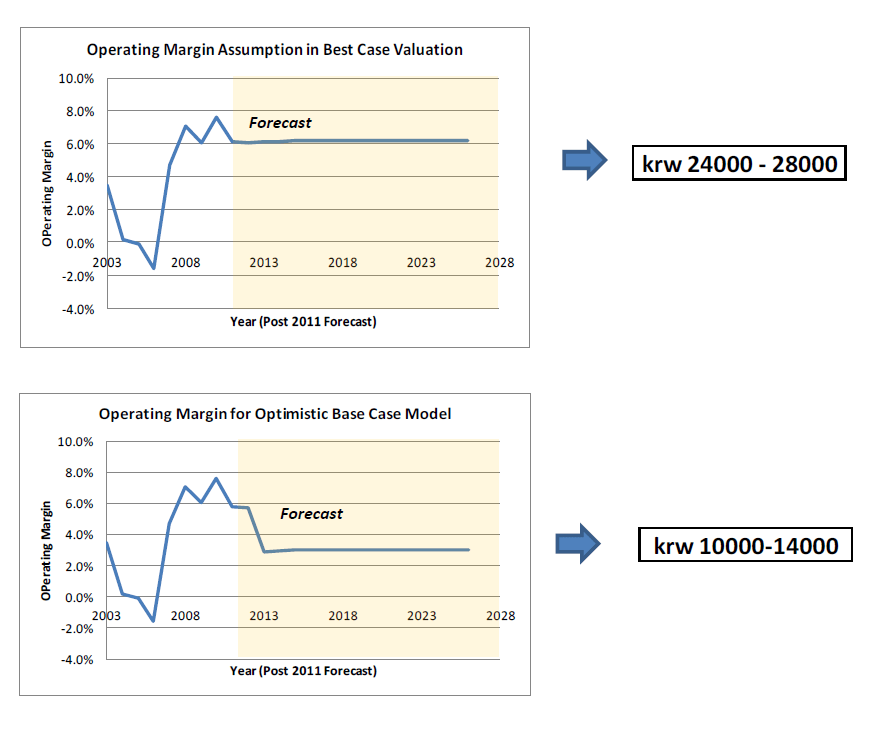

- Prior Valuation Range: We continue to think that our June 2012 launch deck valuation range for Samsung Heavy is still reasonable. The shares are now below our “Best” case scenario, however, but have downside to the “Optimistic Base” case.

- Over-Sold & Inheritance Tax Issue: We are not expert in the Samsung inheritance tax issue, but it seems clear that minimizing shareholder value may be a short-run priority. The shares have declined precipitously in the past year, and it might be best to wait for a bounce to press the short or initiate a position. The tax liability may be a fruitful topic for further analysis.

- Overseas Plant Addition: Samsung Heavy has announced plans to add an overseas facility in a location with lower labor costs. Vietnam, Indonesia, and Malaysia are apparently under consideration. The plant would cost $950 million and focus on lower value ships. In an industry awash in excess capacity for less complex vessels, this seems a bizarre idea at best.

- Merger with Samsung Engineering: The merger with Samsung Engineering, an engineering & construction company with exposure to the Energy sector, makes a bit more sense than the addition of overseas capacity (almost anything would). That said, it is difficult to see how the minor cost synergies would offset the customer perception problems that may result.

Upshot

We continue to believe that Samsung Heavy is, well, somewhat doomed and that the shipbuilding industry is good hunting for shorts. While SHI may have a numerically substantial backlog, the margin on that backlog need not be good or even positive and a portion is pass-through. SHI’s plan to add capacity and merge with Samsung Engineering looks like a strategy developed by a flailing capital intensive enterprise caught in a long downcycle. That said, the inheritance tax issue, pressure on commodity prices, and sell-off in the shares would probably leave us looking for a bounce (like the one CAT recently completed) to press or enter a short. While we expect the shares to eventually trade much lower, we might wait for a better short-run entry point.

(Interested readers should feel free to ping us for our earlier materials.)