The GGR decline of 12% was only part of the story

CALL TO ACTION

- Expectations for September market wide GGR ratcheted lower following August’s details, as a result September’s GGR decline of 12% was in line with recently revised lower expectations.

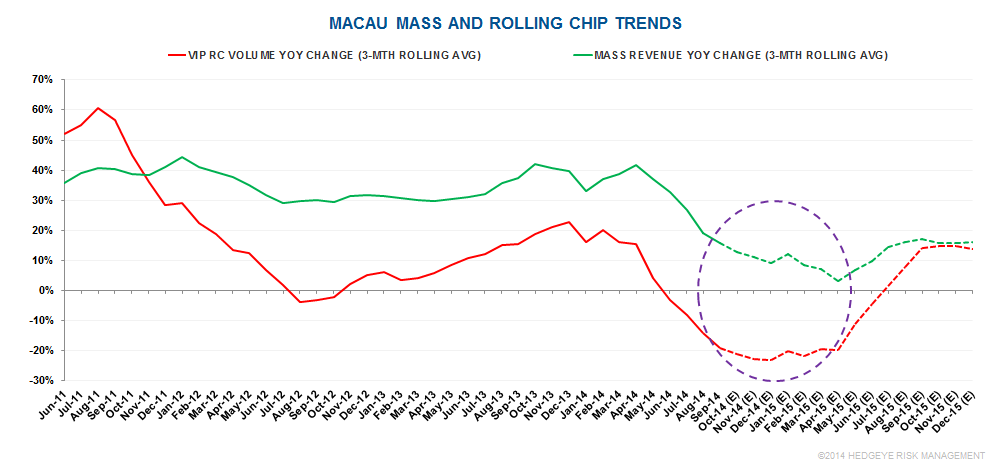

- Mass revenue growth was 15%, confirming our Mass Decelerating thesis for 2H 2014 and we expect additional deceleration during Q4 2014 and Q1 2015.

- We remain concerned with the potential for continued margin pressure as labor costs continue to escalate and player reinvestment rates rise.

- While stock valuations look attractive but we don’t see any positive catalyst on the near term horizon.

- We remain cautious on the Macau stocks with the exception of Galaxy.

SEPTEMBER TAKEAWAYS

Macau Market:

- As already known, GGR fell 12%

- What was not known was that VIP growth was -26%, a further deceleration from August’s -17% and -16% contraction for the prior three months.

- Mass YoY growth only +15%, slightly above August’s increase of +14% and the third month of mid-teens Mass growth as compared to 1H 2014 growth of +36%.

- Our Mass Decelerating theme (first espoused in June) of 2H 2014 is continuing and we expect additional mass deceleration during Q4 2014 and Q1 2015 – at a faster (slower growth) rate than even we thought.

- VIP hold was close to normal for the market and slightly higher than last year

- Rolling Chip volume declined 19% YoY – the second sequential month of such a decline and the worst performance since early 2009

- Galaxy & MGM performed well while LVS was below trend.

LVS:

- Market share dropped to 21.8%, 110bps below the 6 month average driven by very high hold

- VIP revenues declined nearly 14% YoY, while hold was higher than expected at almost 3.6% a 15 bps improvement YoY.

- Disappointing GGR growth was driven by Rolling Chip volume that fell 39% YoY, worst in the market

- Mass revenue grew 15%

WYNN:

- Market share increased 20bps above the 6 month average due strong Mass revenues

- Wynn’s VIP hold percentage fell about 60bps on a YoY basis but was respectable near 3.1%

- GGR fell 16% YoY due to lower VIP hold but Mass revenue grew at 29%

- Rolling Chip volume dropped 19% in line with the market

GALAXY:

- Galaxy’s GGR share was 22.8% an improvement of 190 bps from August and 240 bps above the 6 month average

- Galaxy’s estimated VIP hold improved 35 bps YoY and was near 3.55% for September

- YoY GGR growth of 9% led the market based on market leading VIP growth of 9% and Mass growth of only 10%

- Galaxy remains our favorite stock in the group given its ability to drive VIP revenue growth amid a difficult environment and the likely earlier than expected opening of Phase II on Cotai. We think Phase II could operate for 6-9 months as the only new property on Cotai

MPEL:

- MPEL’s GGR share was 12.6% a decline of 30 bps over the 6 month average

- GGR dropped more than 19% due in part to lower VIP hold and a nearly 35% decline in Rolling Chip volume

- While below last year, MPEL’s September VIP hold was a slight below normal and down almost 50 bps on a YoY basis

- Mass revenues declined 20%

MGM:

- MGM GGR share was 11.1% an increase of 180 bps over the 6 month average and 230 bps above July and August details

- YoY GGR driven by high hold near 3.4% an increase of 70 bps YoY

- Market leading Mass revenue growth was +36%

- Rolling Chip volume declined 26%

- Mass share was slightly better than the 6 month average