Takeaway:

After removing BLMN from our Best Ideas list as a short back in May, we now find ourselves turning constructive on the name, albeit for atypical reasons. The company continues to operate what we believe to be an unsustainable business model, comprised of a portfolio of five different casual dining brands. Furthermore, the fundamentals of the company – decelerating same-store sales, cost of sales inflation (beef, seafood, dairy), margin deterioration and little brand momentum – remain unattractive. The value, however, is there and we suspect management will be forced, or tempted, to unlock it one way or another. With casual dining sales improving, brand initiatives underway and an inflection point in cost of sales approaching (could become a tailwind in 2015), we believe now is an opportune time to get long the stock.

Key Themes:

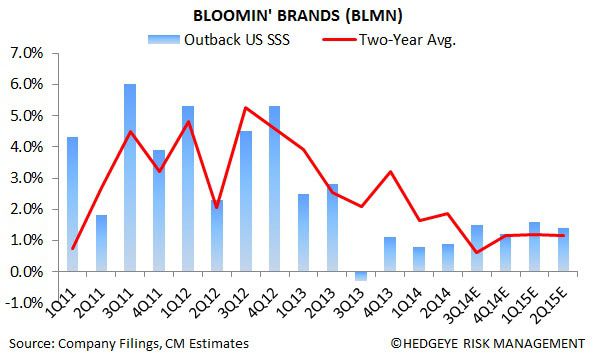

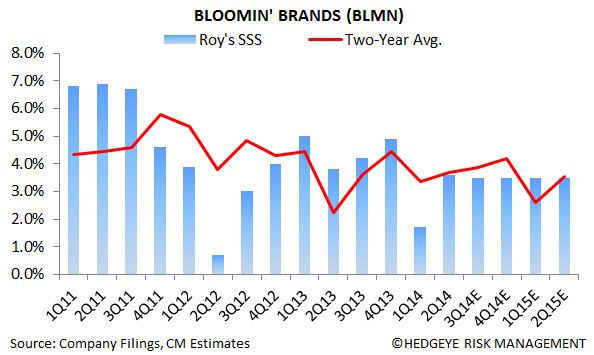

- Same-Store Sales: Two-year average same-store sales have been deteriorating at all of Bloomin’s brands since the end of 2011. In fact, two-year average same-store sales have decelerated nearly ~400 bps since 1Q12. Outback’s dinner business, the core business of BLMN, has shown notable weakness lately as management continues to rollout weekday lunch. Coincidence? We think not. Carrabba’s new menu launch at the end of February proved unsuccessful and Bonefish, in a similarly dire situation, launched a new menu on July 29th. Internationally, the Brazil business continues to be strong but Korea has been a material headwind, as casual dining sales have fallen over 20% the past two quarters likely due to an oversaturated market. We have little visibility into trends in this region, but believe management will take an aggressive approach to stem this decline.

- Daypart Expansion: Management continues to rollout weekday lunch at Outback and Carrabba’s restaurants and was being served in 56% and 51% of locations, respectively, at the end of 2Q. While adding a new daypart should boost same-store sales in the immediate-term, we believe it has hampered the core dinner business and, subsequently, margins. We continue to have our doubts with the lunch daypart, as casual dining chains have been falling out of favor to more convenient fast casual restaurants that offer similar (or higher) quality food at a lower price point.

- Potential Transaction: We recently penned a note calling for management to sell-off its non-core assets and refocus on growing the profitability of the Outback Steakhouse brand. The crux of our reasoning is that multi-concept casual dining companies are structurally flawed and the current fundamentals of the company would suggest the same. If management can restructure the company by pairing it down to one (Outback) or two brands, it could then focus on improving low margins at Outback and growing the business internationally, where it has had great success (save for Korea) to-date. Our sum-of-the-parts analysis values the total of Bloomin’s chains close to $35 and suggests shareholders are getting the Outback business at a discount and the company’s four other brands for free.

Valuation & Sentiment:

The street is bullish on BLMN for reasons we don’t necessarily agree with as 73.3% of analysts rate the stock a buy. Short interest is also fairly low at 4.67% of the float. At 7.7x EV/EBITDA (NTM), BLMN trades at a discount to its peers, reflecting structural issues, lower margins and a high debt-to-EBITDA (~3.6x).

*Appendix: Same-Store Sales

Please note that consensus estimates are shown.

*Appendix: Margin Structure

Please note that consensus estimates are shown.

Email or call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst