Key Take-Aways:

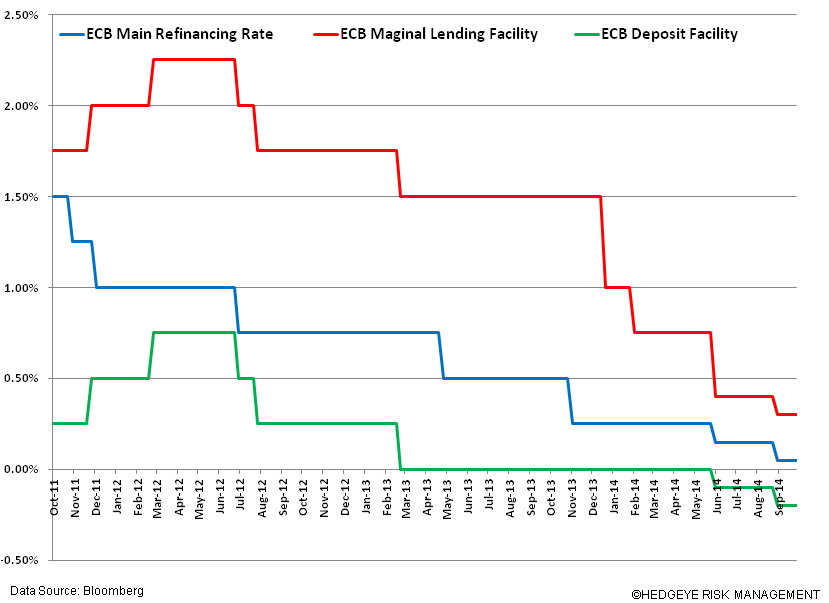

- As expected, the main three interest rates remained unchanged

- Draghi did not deliver or hint at the need for the “drugs” (sovereign QE program)

- We believe the market is finally calling Draghi’s bluff – namely that QE and currency debasement will not produce sustainable economic growth (following the announcement European equities fell further and the EUR/USD is up small and near our oversold TRADE level of $1.26)

- The meeting centered around outlining the terms for the ABS and covered bond purchasing programs – as expected the ECB will accept (with lenient conditions) countries with ABS rated below BBB-

- Again we see Draghi in “wait and watch” mode (admittedly significant action has been taken since June’s first rate cut); however, we’re doubtful that the combo (ABS, covered bonds, and TLTRO) will successfully deliver sustainable credit growth to the “real” economy (target SMEs) over the intermediate term. This is, in part, due to the unwillingness of banks to lend (given weak regional and country growth outlooks) and the lack of structural reform at the country level to spur a business climate of confidence and entrepreneurship.

- Witness the first TLTRO tranche (issued on 9/18) in which only €82.6B was drawn by participating banks (well below consensus estimates of €150B – €300B)

- We expect Draghi to remain challenged to revert the strong levels of disinflation across the region

- Hedgeye’s bearish bias on the EUR/USD (etf FXE) and select European equities remains (for more join today’s 4Q Macro Themes call at 1pm EST – ping for access)

On ABS and covered bond purchase programs:

- Programs will last at least two years

- ABS purchases to start in fourth quarter 2014

- Covered bonds purchases to start in the second-half of October

--For more details on terms and conditions see the ECB’s release

Other Selective Commentary:

- Draghi reiterated the ECB’s willingness to take the balance sheet up by ~€1Trillion (to 2012 levels)

- Draghi reiterated the need for balance sheet adjustment from public and private sectors so that the combo of measures (ABS, covered bonds, and TLTRO) could have hopes at success

- Draghi said the 10bps M/M drop in Eurozone CPI (to 0.3% in SEPT Y/Y) was due primarily to declining oil prices

Matthew Hedrick

Associate