The next big update on likely Fed direction will be tomorrow's employment report for the month of September. Expectations are relatively high, with consensus looking for a sequential acceleration of over +70k net new jobs to 215k; admittedly, off a disappointing 142k print last month. Last month, in conjunction with our macro team, we published a note that looked at the historical relationship between ADP and NFP (that note can be found here). We found that ADP tended to move in the same direction sequentially as NFP 64% of the time across the 160-month history of the ADP series. For reference, yesterday's ADP print came in at 213k, up sequentially from the 202k in August (revised from 204k). While it appears that consensus is set up right directionally, our analysis revealed no strong correlation on magnitude of sequential change.

Where Are We In the Grand Scheme?

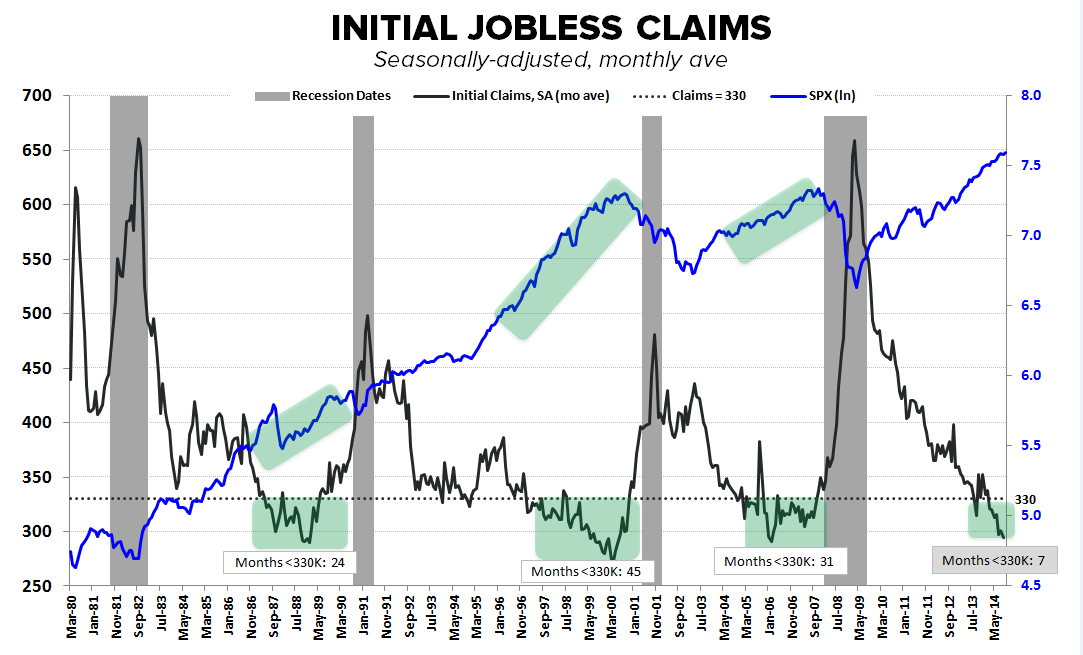

The initial jobless claims data this morning is reasonably strong. SA rolling claims continue to trend lower, coming in just under 295k this week. As the first chart below shows (courtesy of Christian Drake of our Macro Team), the data has now been sub-330k for 7 months. Looking back historically at the last two cycles, rolling SA claims ran at sub-330k for 45 and 31 months, respectively, before the corresponding market peaks in March, 2000 and October, 2007.

The Data

Prior to revision, initial jobless claims fell 6k to 287k from 293k WoW, as the prior week's number was revised up by 2k to 295k.

The headline (unrevised) number shows claims were lower by 8k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4.25k WoW to 294.75k.

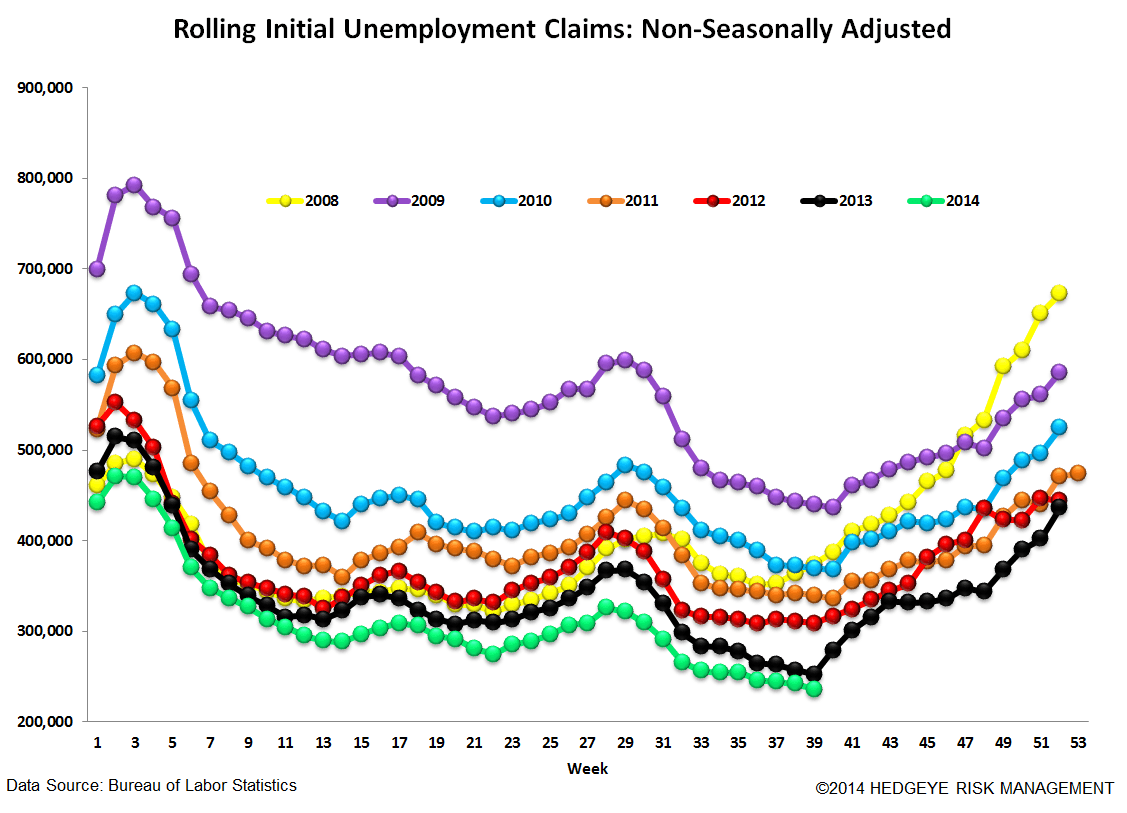

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -6.5% lower YoY, which is a sequential improvement versus the previous week's YoY change of -5.9%

Yield Spreads

The 2-10 spread fell -10 basis points WoW to 187 bps. 3Q14TD, the 2-10 spread is averaging 199 bps, which is lower by -22 bps relative to 2Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT