“The triumphant success of Hong Kong demands - and deserves - to be maintained.”

Charles, The Prince of Wales

The crowds of tens of thousands in Hong Kong are swelling in number. Today, Chinese National Day, the numbers are likely to increase significantly. While started by students, all facets of the population are represented. One can only be in awe at how so many can demonstrate peacefully, even in the face of harsh and utterly unnecessary police tactics: Not one single shop window has been broken in 5 days of protest.

Back to the Global Macro Grind…

How did this all get started?

In the run-up to the 1997 Handover of Hong Kong, Universal Suffrage was promised under Article 45 of the Basic Law. In 2004, the National People’s Congress said this would not occur before 2012. In 2007, the NPC pushed the date to 2017. In 2014, Universal Suffrage is redefined: Everyone can vote, but only for the 2 or 3 candidates pre-selected by Beijing. The serious matter of a peoples’ freedom to elect their leaders has been made a farce by the Central Government and the current Hong Kong leadership.

Over the summer, Beijing completely misread the situation thinking that its version of a seemingly democratic process would be sufficient to keep the Hong Kong people at bay. Yet the proposal was so far off the mark and without any room for negotiation that a tipping point was reached.

While Beijing is known for digging in and using all means necessary to obtain its will, it appears the people of Hong Kong are willing to do the same this time around. There is no quick solution given Hong Kong Chief Executive CY Leung’s unwillingness to work for the Hong Kong people he supposedly represents. Leung’s administration has fantastically mismanaged this situation.

The Central Government needs this win. A loss of face isn’t the primary concern: The very survival of the Communist Regime is at stake in the eyes of China’s leaders. No progress is being made at containing unrest in Xinjiang Province where Uyghur separatist are claiming the region.

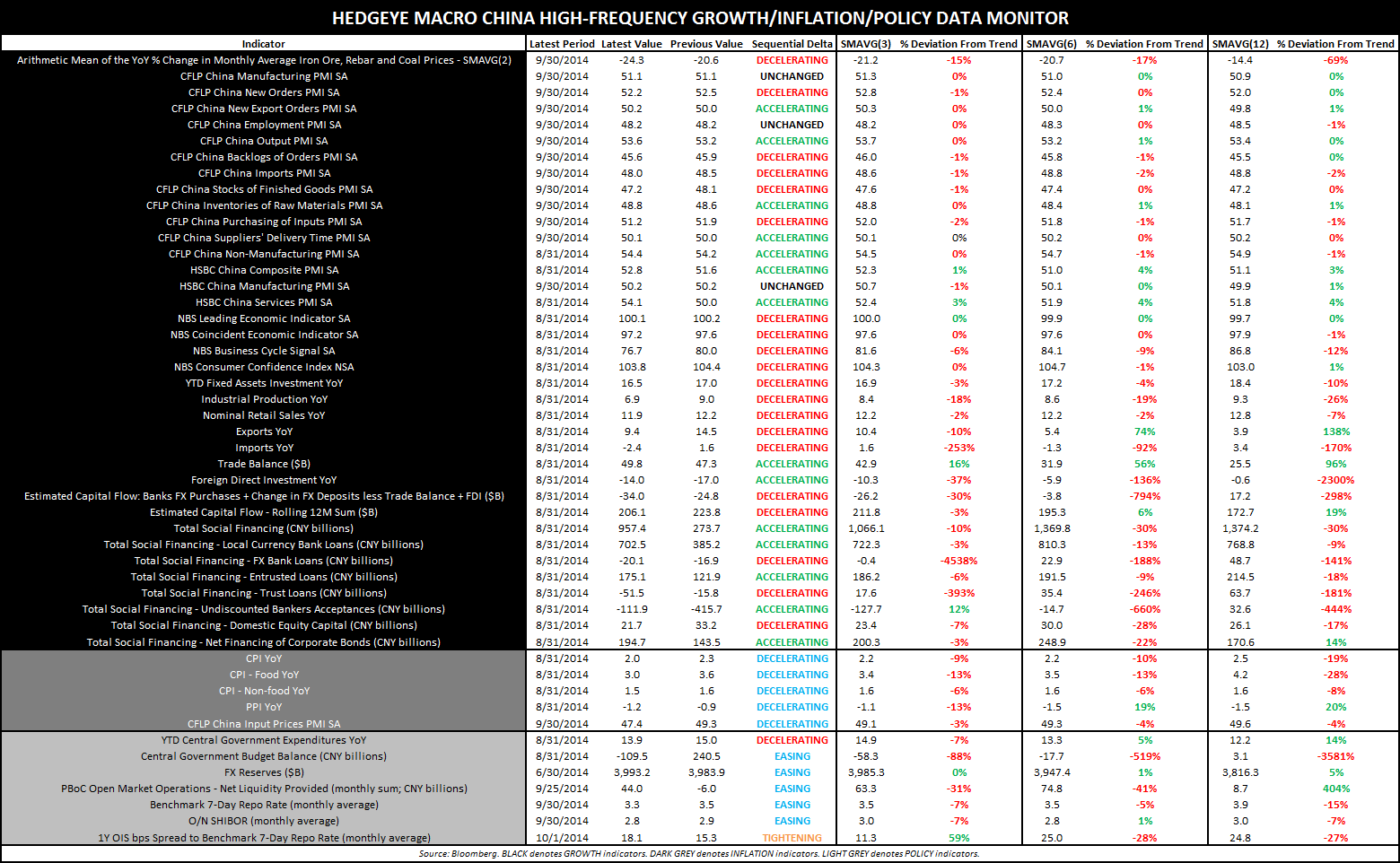

To add to Beijing’s woes, the Chinese economy is cooling quickly. Fixed assets investment is slowing both sequentially (as of AUG) and on a trending basis – as are retail sales, exports and imports. Manufacturing PMI and consumer confidence are also slowing on a trending basis as of SEP and AUG, respectively. Additionally, the property market is in dire straits, as Darius Dale details in a note yesterday titled, “DEFCON 2.5: The “China Overhang” Is Likely To Continue”.

Already, we have seen a few, albeit small, public gatherings in large cities supporting the protesters in Hong Kong. What if demonstrations spread beyond Hong Kong?

In the last few days, the world has experienced an unprecedented crack-down on social media and freedom of speech to prevent just that from happening. But we know very little about it in the United States. One would need to live in the PRC to experience it. It’s hard for us to imagine what the internet looks like when one only gets to see a carefully selected portion of it. Overnight, there are reports of a Trojan virus aimed at infiltrating the iPhones of HK protesters. Make no mistake, this is a first rate electronic communications war being played out in front of us.

How will the world react to all of this? The United Kingdom, as former colonial masters, surely has a moral responsibility. But the West is and will be reluctant to take a stand against China. Cross-strait relations also play a factor: Beijing continues to strive for a unified China, inclusive of Taiwan. The wrong action in Hong Kong could further alienate the Taiwanese people.

Unless the protesters get tired we will all be watching this for some time. There will be economic impact. But the big changes will play out in the long term.

Can democracy thrive in Hong Kong? And will this lead to a softening of the regime in Beijing?

The people of Hong Kong appear ready to find out.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.46-2.55% (bearish)

SPX 1 (neutral)

RUT 1090-1026 (bearish)

EUR/USD 1.26-1.38 (bearish)

WTIC Oil 90.16-94.42 (bearish)

Michael Blum

President and Resident of Hong Kong