TODAY’S S&P 500 SET-UP – October 1, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 0.78% downside to 1957 and 0.70% upside to 1986.

SECTOR PERFORMANCE

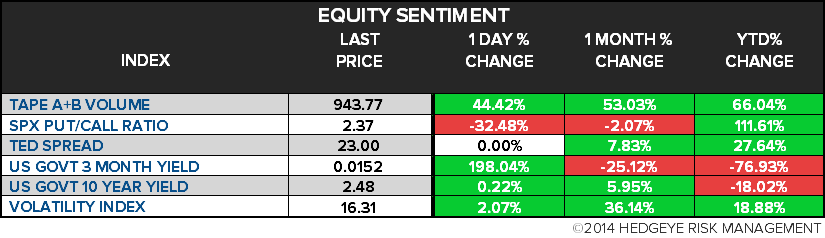

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.91 from 1.92

- VIX closed at 16.31 1 day percent change of 2.07%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Sept. 26 (prior -4.1%)

- 8:15am: ADP Employment Change, Sept., est. 205k (prior 204k)

- 9:45am: Markit US Mfg PMI, Sept. final, est. 57.9 (prior 57.9)

- 10am: ISM Manufacturing, Sept., est. 58.5 (prior 59)

- 10am: Construction Spending m/m, Aug., est. 0.5% (prior 1.8%)

- 10:30am: DOE Energy Inventories

GOVERNMENT:

- Senate, House out of session

- 9:30am-1pm: Energy Sec. Moniz speaks at energy security event

- Panel afterwards incl. IHS Vice Chair Yergin, White House counselor Podesta

- 10:30am: Former President Bill Clinton World Energy Engineering Congress keynote address

- 2pm: SEC Commissioner Gallagher speaks at mkt structure conf.

- 2:45pm FINRA CEO Richard Ketchum and SEC head of trading, Steve Luparello, also speak

- 2:45pm: SEC Chair White speaks at panel at Intl Organization of Securities Commissions meeting in Rio De Janeiro

- 4pm: Sec. of State Kerry to meet with Chinese counterpart Wang Yi at State Dept

- U.S. ELECTION WRAP: Latino No-Shows; Senate Control Consensus

WHAT TO WATCH:

- Pershing Square Raises Size of IPO to $2.73b From About $2b

- Eurozone Sept. Manufacturing PMI 50.3; Est. 50.5

- First Ebola Case Diagnosed in U.S. Confirmed in Dallas: CDC

- Japan Stock Orders of $617b Scrapped in Trading Error

- Bristol-Myers Transfers $1.4b of Pension Risk to Prudential

- Nomura, Goldman Sachs Among Firms to Lead Japan Post IPO

- FAA Orders New Pilot Displays for 1,300 Boeing Jets: WSJ

- Oracle Seeks Partners in China to Expand Cloud Service Business

- Fannie, Freddie Investors Lose Suits Over Profits Taken by U.S.

- Wal-Mart Judge Says Retailer Must Face Mexican-Bribe Probe Suit

- Apple Said to Add Gold Option to IPad in Effort to Boost Sales

- BNY Mellon to Shutter Its Derivatives Sales, Trading Group

- U.S. Said to Reach Accord With Brazil Ending Cotton Trade Fight

- Hong Kong Leader Jeered by Protesters on China National Day

- President Obama meets with Israeli Prime Minister Netanyahu

- GM, Chrysler, Ford Sept. Auto sales; SAAR may drop vs Aug.

EARNINGS:

- Acuity Brands (AYI) 8:56am, $1.22

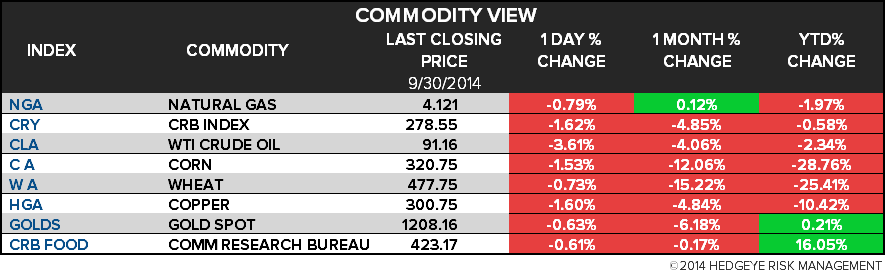

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Corn Extends Drop to Five-Year Low as U.S. Supply Tops Estimates

- Goldman Sees Corn to Soybeans Extending Losses on U.S. Supplies

- WTI Crude Rebounds Before U.S. Stockpile Report; Brent Climbs

- Nickel Declines to Six-Month Low as Stockpiles Expand to Record

- Arabica Coffee Rises on Outlook for Brazil’s Crop; Cocoa Falls

- Platinum Drops to 5-Year Low as Palladium Declines on Car Sales

- Top Cotton Trader Says Prices Need to Fall More to Cut Surpluses

- U.S. Oil Exports Seen Breaking 1957 Record as Traders Dodge Ban

- Palm Oil Declines After Posting Biggest Monthly Gain Since 2009

- Marubeni Offloads $1 Billion Canadian Coal Mine for a Buck

- Gas Allure in U.K. Power Poised to Extend Into Winter on Outages

- Worst Seen Over for Global Oil Prices as Saudis Cut Output

- Shanghai-London Parity Signals Aluminum Rally: Chart of the Day

- Mideast Turmoil Keeps Gasoline at 45 Cents in Oil States: Energy

CURRENCIES

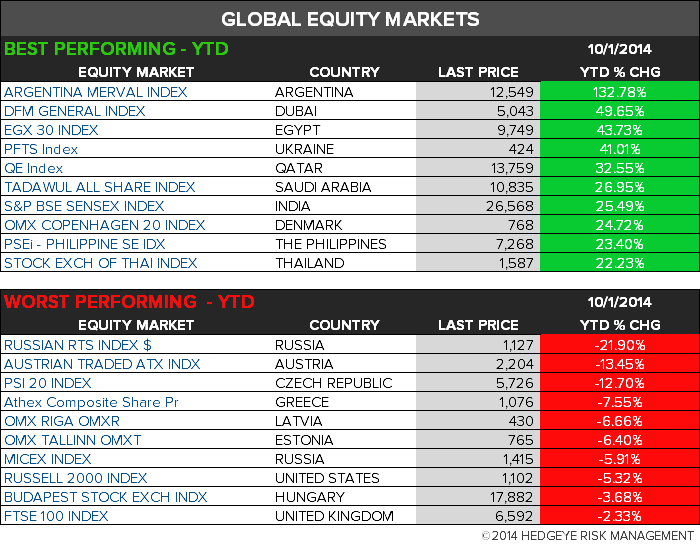

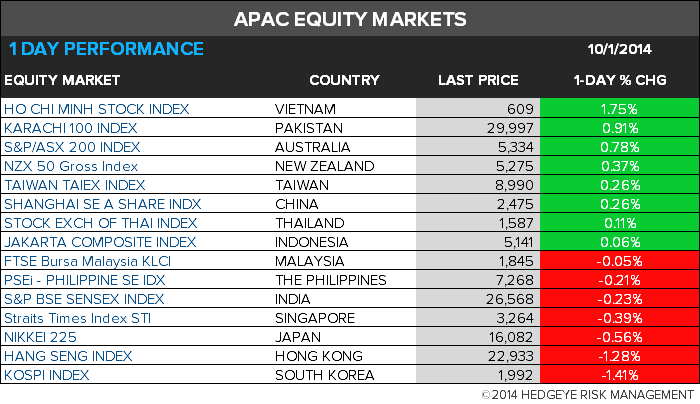

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team