Last week we hosted a conference call to review our 60-page slide deck as to why we think KSS is a short. If you’d like to listen to a replay of the call and download the full materials, please click the link below. We picked out eight slides below that are among the more controversial.

Replay Link: CLICK HERE

Materials: CLICK HERE

Point #1: Expectations Too High

Yes, near-term numbers look doable given several tailwinds facing all retailers. But one we get past this year (only four months away) we think KSS numbers will start to come down materially. The consensus has earnings growing 10% next year, while we think they will be down nearly 10%. Then they’ll be down again, and again, and again. Ultimately, once we’re past 2014, we don’t think that KSS will earn $4 again until the tail end of the next economic cycle.

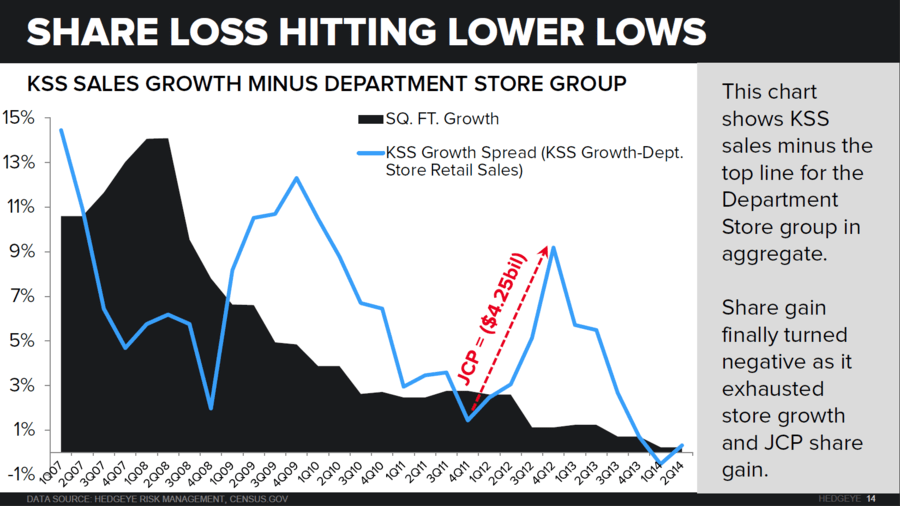

Point 2: Losing Share At A Faster Rate

It’s no secret that department stores are losing share of wallet (3.5% of Retail Sales vs 10% a decade ago), but KSS is losing share within that context. The blue line in the chart below shows KSS’ share gain of the department store space. The first big bubble – from 1Q09 to 4Q10 – came about 3-years after a meaningful square footage growth spurt. That’s when the stores began to hit the sweet spot of the maturation curve. Then the next bubble came a little over a year later when KSS gained what we think (based on our surveys) is $1bn in share from JCP. Our latest survey shows that about $150mm has shifted back to JCP – but that still leaves $850mm at risk for KSS. The punchline is that after gaining share of this space every single quarter since its inception, KSS is now a net share loser.

Point 3: This Model Is Broken

There’s no square footage growth – at all. Productivity of $210/ft in brick and mortar stores is trending down. E-commerce is the only growth engine, but unfortunately it is the lowest margin business at KSS by a country mile. As such, gross margins are structurally headed lower. SG&A can’t be cut in line with the gross profit erosion. D&A was just lowered from $950mm to $900mm – which is stunning in itself. That’s not likely to go down much further. Cash flow still remains healthy enough to buy back 7% of the stock this year. Buy with lower net income, we think that repo/financial engineering gets cut by better than 50% for the duration of the model. EBIT should be down 5-8% each year, with share count making up about 3% of the gap. Net/net = EPS declining every year.

Point 4: Store Productivity Bifurcation

Sales per square foot have been flat for the past four years, but that is only if you include e-commerce. Brick & Mortar productivity is $210, and is at the lowest rate we have ever seen it. There is absolutely no valid argument we can find that this turns around – particularly given that JCP is sitting at just $108 in productivity and has KSS right in its sights. We think those two will converge over time.

Point 5: New Brands – Juicy and Izod

This topic absolutely dominates the information flow around KSS. We all know that Juicy Couture and Izod are now available at KSS. That said, our consumer survey shows Kohl’s purchase intent is down year/year, while retailers like JC Penney and Macy’s are up meaningfully. So we know about the brands – but consumers might not know, or might not care. Nonetheless, let’s keep in mind that there’s noise around new brands EVERY year at Kohl’s. Take a look at the graphic below. Could this years’ additions be better than last years? Possibly. But keep in mind that Izod and Juicy are not exclusive. Izod is all over Macy’s and JC Penney’s. Juicy is in the process of growing distribution through new owner Authentic Brands. To get a good read you need to quantify the impact (see next exhibit).

Point 5b: Quantifying Juicy and Izod

We know that these brands occupy 525 sq ft and 700 sq ft, respectively, inside the average KSS box. That’s 1.42% of KSS’ total square footage. Now…it can’t just create space out of nowhere, which means that it needs to take out product that is underperforming – but is still productive. Assuming that these brands generate $225/ft in productivity, and that it is replacing private label brands that are doing $110 per foot in the same space, we build up to about $250mm in incremental sales in another two years. That’s about 1.3% accretion to sales, but it comes at a lower margin as these national brands carry lower profitability than the portfolio as a whole. The bottom line = it’s going to take a lot more than a couple of mediocre brands to salvage KSS’ top line.

Point 6: Structural Margin Decline

Gross margins on KSS’ e-commerce business run about 1,200bp below the store-level margins. Some people are hoping/banking on a margin rebound as KSS did not seemingly benefit from the same tailwind the rest of the group has over the past five years. The truth is that it has. Without that tailwind we’d be looking at KSS with margins near 5-6% today. The industry tailwind was masked by the massive growth in KSS’ e-commerce business. In fact, from ’05-’13 KSS put up the highest growth rate of any ecommerce business in the US throughout all of retail. But as this business continues to grow 15-20% annually (the only line item to grow aside from SG&A) it naturally depresses aggregate GM% by 30bps per year. Those are margin points that this model can’t afford to lose.

Point 7: Keep An Eye On KSS Credit

Many retailers have, or maintain, credit cards. It’s a solid tool to keep customers and incentivize them to spend more. But our consumer survey suggests that 18% of KSS shoppers have a rewards card. But more importantly, we know that 57% of purchases are made by that card. That is a simply staggering figure from where we sit. Three years ago KSS shifted its partnership from Chase to Capital One. But median credit scores for Chase customers range between 700-750, which are optimal for a mid-tier retailer. But the 700bps in card penetration that KSS saw under Capital One came at a median credit score of 600-650. Basically, this tells us that incremental sales growth is likely coming from more marginal consumers. This is not exactly a smoking gun on the short side, but taken in context with the other pressures we see to the model, it certainly does not bode well.