TODAY’S S&P 500 SET-UP – September 26, 2014

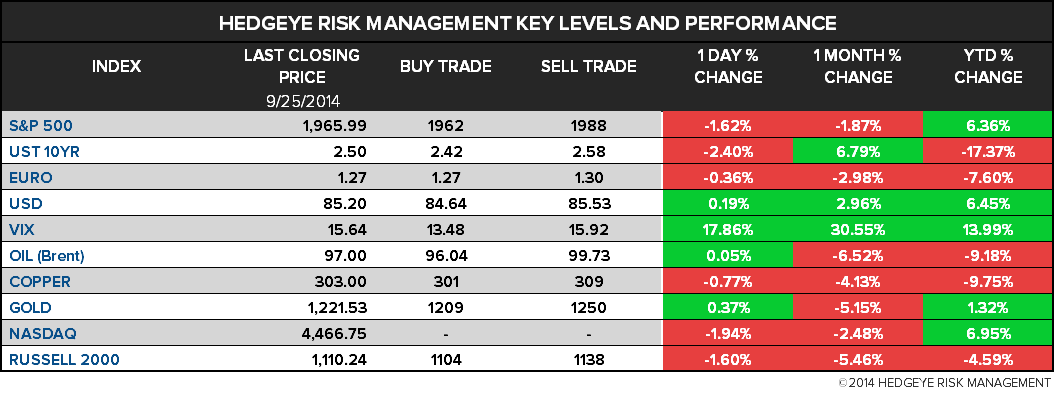

As we look at today's setup for the S&P 500, the range is 26 points or 0.20% downside to 1962 and 1.12% upside to 1988.

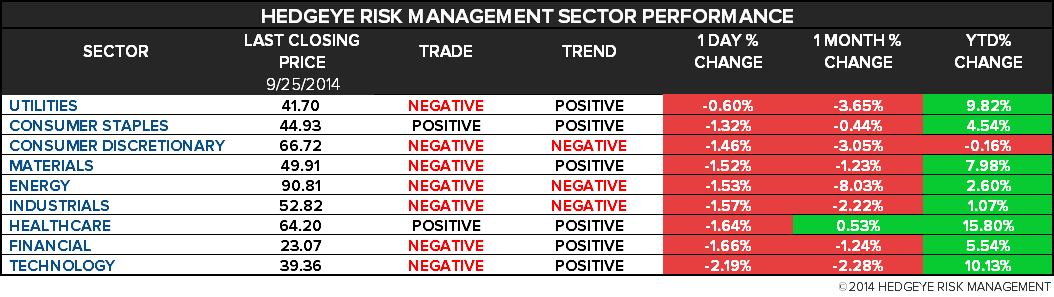

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.94 from 1.95

- VIX closed at 15.64 1 day percent change of 17.86%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: GDP Annualized q/q, 2Q final, est. 4.6% (prior 4.2%)

- 9:55am: UofMich Confidence, Sept. final, est. 84.8 (pr 84.6)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Senate, House out of session

- 10am: Indonesian President Yudhoyono delivers remarks at GWU

- 1:15pm: TSA Administrator Pistole at Aero Club of Washington

- U.S. ELECTION WRAP: Keystone Hangs on Sen. Race; Debate Dates

WHAT TO WATCH:

- Netflix, Charter Said to Get Data Demands in Comcast Probe

- Deadline to Shut Down Sanctioned Oil Ops. w/ Russian Partners

- Obama Delivers Remarks at Global Health Security Agenda Summit

- Alibaba Bears Emerging to Short 8.9 Million Shares After IPO

- Apple’s IPhone Software Snafu Has Links to Flawed Maps

- Apple Releases iOS 8 Update to Fix iPhone 6, Plus Bugs

- Symantec Appoints Interim Chief Michael Brown as Permanent CEO

- GM CFO Says Ratings Upgrade Aids Loan Unit to Support Car Sales

- Intel Spending $1.5b to Bolster China Phone Market Access

- Chiquita Sweetens Fyffes Merger Terms After Rival Approach

- New ABC App Lets Mulitasking Fans Post Clips Fast

- Iraqi Leader Seeks Decisive Airstrikes to End Extremist Terror

- U.K. May Start Iraq Strikes Within Days of Parliament Vote

EARNINGS:

- BlackBerry (BB CN) 7am, ($0.16) - Preview

- Finish Line (FINL) 7:05am, $0.60

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Rebounds From 14-Week Low Before Figures on U.S. Growth

- Top Palm Oil Growers Scrap Export Tax Amid Battle for Buyers

- Cheaper Energy to Grain Signals Tame U.S. Inflation: Commodities

- Soybeans Extend Drop to Lowest Since 2010 on U.S. Crop Prospects

- WTI Oil Set for Second Weekly Gain Before GDP Data; Brent Rises

- Gold Falls Before GDP to Inflation Reports as Silver Holds Gains

- Philippine Lawmaker Files Bill Aiming to Ban Ore Exports by 2021

- Nuclear Plants Across Emerging World Defy Japan Concerns: Energy

- Saudi Arabia Said to Plan Steady Oil Output for Rest of 2014

- Europe Seen Sustaining Russian Gas Cut During Normal Winter

- European Gold Sales Total 6.8 Tons in Final Year of Accord

- Polar Ice Research for Climate Clues Means Having an Armed Guard

- Soybean Traders Bearish for Seventh Week as Harvest Accelerates

- Oil Curve Errs as U.S. Sales to Shrink Spread: Chart of the Day

- Natural Gas Pricing Outlook Restrained in U.S. ’Shoulder’ Months

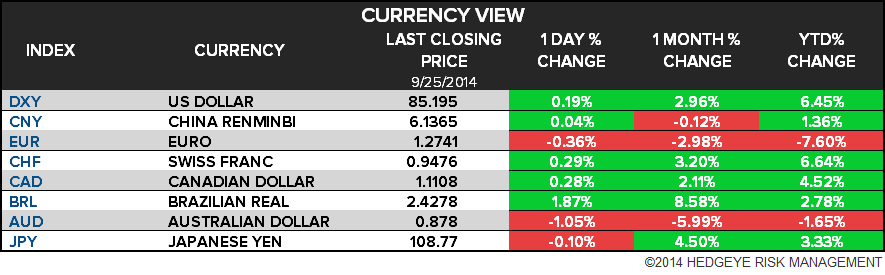

CURRENCIES

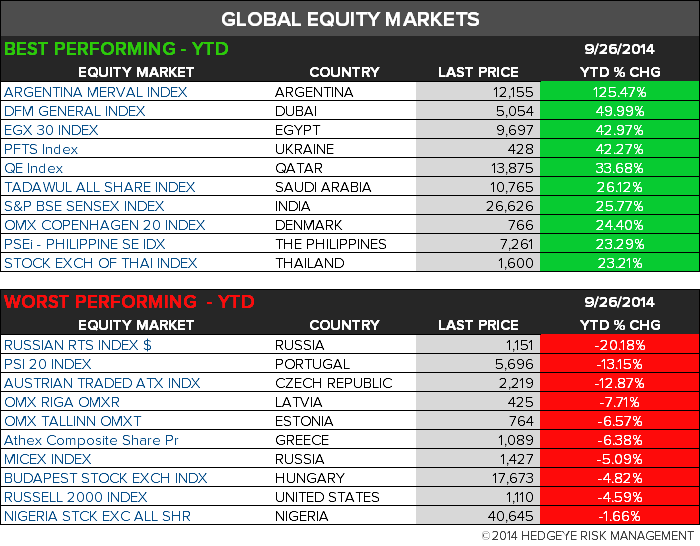

GLOBAL PERFORMANCE

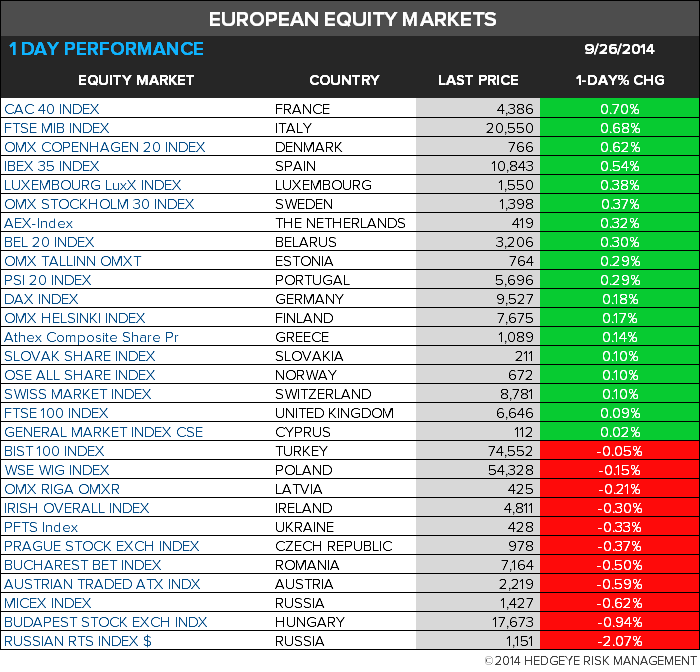

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team