While we might not like Nike as much as some of our key long ideas, we’re comfortable owning it into the print on Thursday. The general consensus out there is that we should see an in-line (ish) quarter, with continued strength in futures – and management throwing out an element of caution with guidance given that the Dollar has strengthened 6% against the Euro in the 13 weeks since NKE last gave guidance – and during that time NKE has actually gone up by 5%. We think all of that is true – sort of. Yes, futures are likely trending in the 10% range, and management will almost definitely use the FX environment as a way to keep estimates grounded for the remainder of the year. But the one thing the street is missing is the leverage on the P&L this quarter. The Street is looking for Nike to deleverage 9.3% sales growth into a measly 2% growth in EPS. We think that’s way too conservative.

We think that sales will be up by 12% in the quarter – despite a poor showing by Nike teams in the World Cup, the company definitely turned this into a very commercial revenue event – in traditional Nike style. Importantly, despite what should be a $390mm boost in SG&A (175bp deleverage), Nike should leverage its growth into 12-13 EPS growth. We’re at $0.97 versus the Street at $0.88. As a point of reference NKE’s $390mm SG&A boost for the quarter is 55% greater than UnderArmour’s entire annual marketing budget.

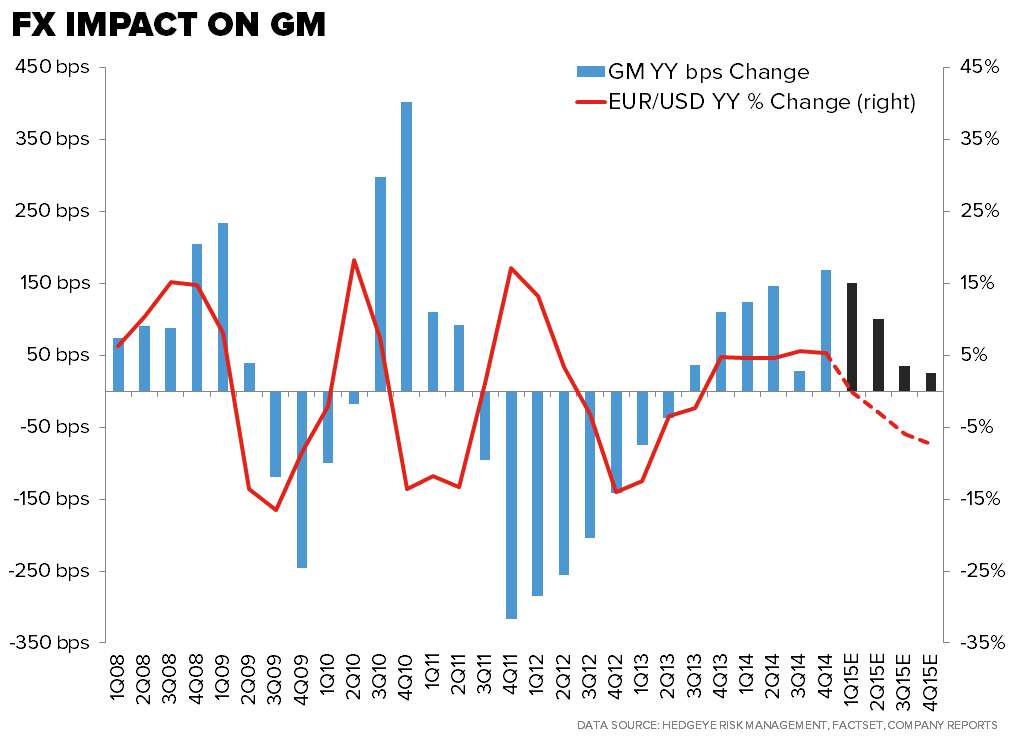

While we think the quarter will be big, we’re not going to gloss over the near-certain tempered FX-related guidance for the rest of the year. The chart below speaks volumes. No matter how you cut it, a strengthening dollar is bad for Nike’s P&L. If it leads to increased US consumption that could help the business in the home market, but let’s face it…Nike does not need any hand holding in the US to drive its business. Maybe it boosts US tourism abroad a bit, but we’re hard pressed to think that many people travel to distant lands to buy a pair of Nike kicks. Net/net, FX trends are bad. The company has a sophisticated hedging process, that protects it from about 75% of the FX move on its cost of goods (when it receives an order, it uses local currency to buy dollars forward and match its product costs – which are all sourced in dollars). But we’re more concerned about the translation effect of foreign-denominated profits. Nike does a pretty good job of offsetting the Gross Margin hit and unfavorable translation with hedging – which it does purely on a transactional basis as opposed speculative hedging – and as such, EPS growth is unlikely to slow materially due to FX. But in the 15+ years we’ve covered Nike, we have yet to find a time when investors paid as much in the earnings multiple for better ‘other income’ from favorable hedges as opposed to better organic gross margins.

If the stock were trading at 18x earnings, we could care less. But at a 24x p/e, it’s definitely something to consider. The other thing that could save Nike in an unfavorable FX environment is SG&A, which should slow dramatically over the course of the year. We’ve got 19% growth in Q1 going down to -1% by Q4 – and it could end up being much less than that. Again, we don’t think that people will pay as much for SG&A leverage as they will for GM improvement, but this is the beauty of the Nike model – they’ll almost always find a way to hit annual growth targets.