“When we are no longer able to able to change a situation – we are challenged to change ourselves.”

-Viktor E. Frankl

As egotistical as many successful stock investors seem on the outside, a common attribute for many of them is, ironically, their ability to change their minds. Now often some poor analyst in their employ is blamed for the mistake, but when the facts and/or thesis changes, the position is rightfully exited.

Hubris is a dangerous thing and in investing it can be downright deadly. The ability to adapt to new information and admit mistakes, on the other hand, can be an immensely valuable skill.

The ability to adapt, of course, is hardly new to our species. A recent article in Smithsonian magazine based on new research actually argues that the ability to adapt is maybe the most important skills and has enabled homo sapiens to thrive over the last 1.85 million years.

According to this article:

“What results from these analyses is the realization that there is no simple, clear picture; no obvious mechanism as to why the genus we know as Homo came to arise and dominate. What we've long thought of as a coherent picture—the package of traits that make Homo species special—actually formed slowly over time.”

So if it was not our unique skill set that allowed us to thrive, what was it? Well, according to the article, the answer is quite straight forward:

“That early Homo species would have had to cope with this constantly-changing climate fits with the idea that it was not our hands, nor our gait, nor our tools that made us special. Rather, it was our adaptability.”

So, of course, it begs the questions: when are the Old Wall consensus economists going to adapt their projections for 3% U.S. economic grow in perpetuity?

Back to the Global Macro Grind...

The 3% growth projection noted above may seem like a non-sequitur, but the comment was actually born of out attending the Bloomberg Markets Most Influential conference earlier this week and comments from William C. Dudley, the President of the New York Fed. Since Bloomberg radio and TV called him one of the smartest men in the world, it seems only prudent that we pay attention to his comments.

Aside from his comments that all will indeed be well if we hit 3% in growth in perpetuity, Dudley also indicated he doesn’t have a lot of faith in that happening. We’ve paraphrased below, but a couple of interesting comments from Dudley were as follows:

- The Fed is difficult to manage as it relates to the economic estimates that come in from various methods (Takeaway: this transparency and democracy stuff related to setting policy may be less effective if the inputs aren’t systematic, which they are not);

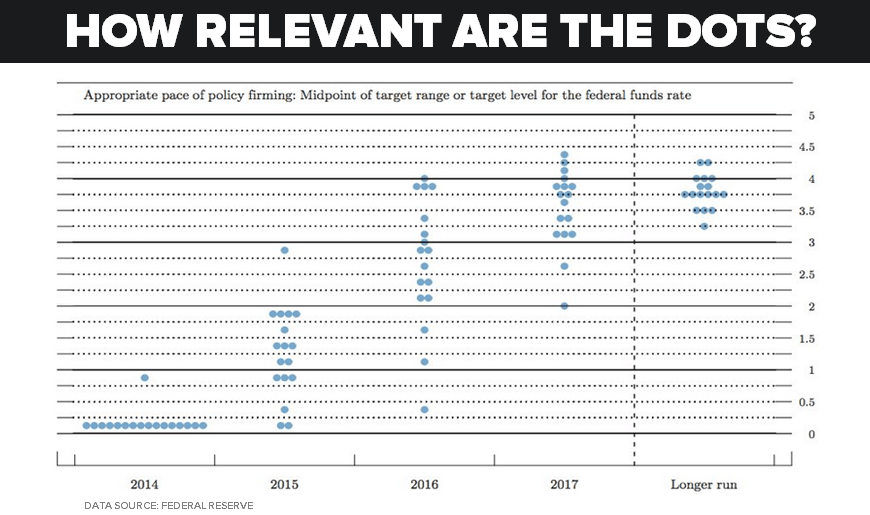

- Dudley said not to overweight the “dots . . . he has a wide confidence interval in his dots (Takeaway: we would agree as the fascination with the dots is reaching near epic proportions, so they are certainly soon to be irrelevant);

- According to Dudley, the Fed doesn’t care about the dollar per se, but too strong of a dollar is an economic deterrent (Takeaway: the Fed cares about the dollar, and, shockingly still doesn’t get the economic value of a strong dollar policy); and

- There are reasons to be patient on monetary policy and as an example monetary policy was tightened too quickly during the Great Depression (Takeaway: if you didn’t know whether Dudley was dovish, now you know. But really Bill, a Great Depression reference?).

On one hand, we certainly appreciate Dudley acknowledging the flaw in forecasting--it shows his adaptability. Conversely, the Great Depression and strong dollar fear mongering is a little disturbing, but certainly difficult to read much from brief comments on a thirty minute panel! And who are we to judge...

As for Hedgeye, we don’t know what the Fed is going to do next and frankly despite my comments above, Fed watching is a bit of fool’s errand. In our analysis, as the data changes, we adapt. It is that simple.

The most recent change for us recently has been the view that the U.S. economy is now likely in what we call Quad 4, which is an environment in which growth is slowing, inflation is slowing, and monetary policy is loose.

Especially on inflation, this is an about face for us. But that fact is that headline inflation is now down to +1.8% for the quarter, which is a deceleration. Along with that many commodities are now deflating incrementally, and Brent Crude in particular is down more than -12% on the year.

Even as inflation is decidedly decelerating, we do continue to get mixed data on growth (some good, some bad). But as my colleague Darius Dale recently highlighted, we think it’s important to highlight the risk of #GrowthSlowing given where consensus expectations for growth remain – i.e. out to lunch. Moreover, the lack of dispersion among forecasts remains a key risk.

Specifically, in the previous five quarters, the standard deviation of growth is 0.44% and peak to trough is 122 basis points. Meanwhile the forward consensus projections for the next five quarters have a standard deviation of 0.02% and peak/trough spread of 18 basis points. We don’t know much, but we do know those projections will be missed.

Our immediate-term Global Macro Risk Ranges are now (with intermediate term TREND signal in brackets)

RUT 1115-1149 (bearish)

Shanghai Comp 2 (bullish)

VIX 13.14-14.99 (bullish)

Pound 1.62-1.64 (bullish)

Copper 3.01-3.09 (bearish)

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research