Given trends seen from our pricing survey, we believed a F3Q beat was already in the bag with the Caribbean, while slowly improving, still limping along in a tough promotional environment. The ECA cost impact may be a little above expectations but more importantly, we wonder if the exuberance on Europe is overstated heading into 2015.

CONF CALL

- Steady progress in both Carnival and Costa brands in F3Q

- 3Q confirmed Carnival turned the corner

- Notable lengthening of bookings curve across European brands

- NA/Europe bookings/pricing higher for 1H 2015

- Yield growth can be sustained

- Without mitigation, ECA requirements were originally expected to reduce EPS by $0.75. But with new technology, limited ECA impact to $0.10.

- Technology initiatives: propelling, lighting and air conditioning.

- Costa: seeing steady improvement in yield and profitability

- New Princess ship: only new build for 2014 and will sell Ocean Princess

- China: expect double digit growth over next few years

- Already the largest cruise operator in mainland China (1st in market through Costa brand in 2006).

- China operations have and are profitable.

- 4 homeports (shifting) and 12 marketing offices

- 3Q

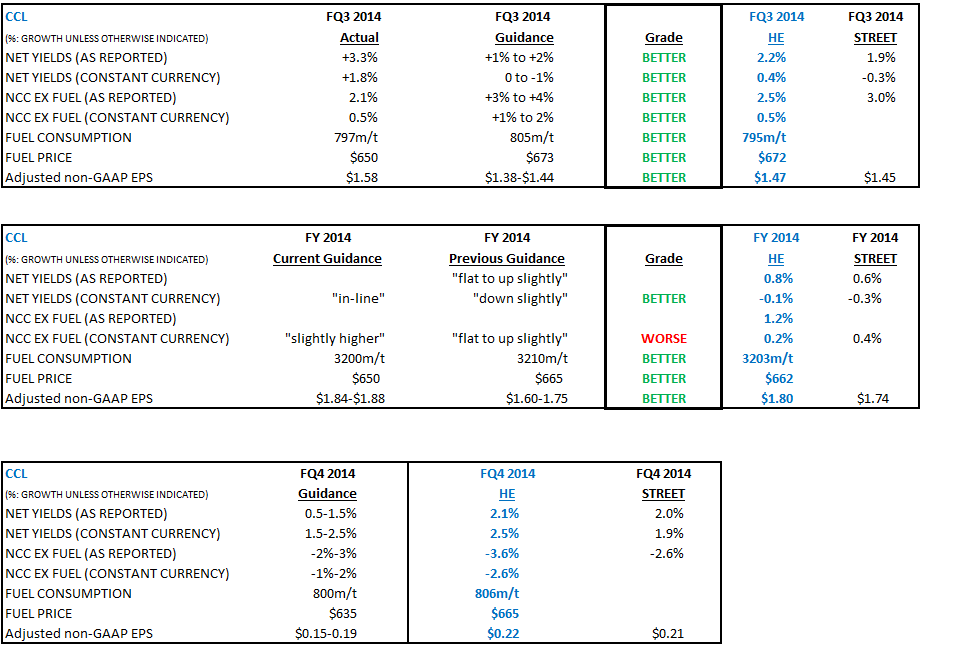

- Better rev yields (11 cents) - split btw ticket and onboard

- Lower NCC ex fuel (3 cents)

- Lower fuel prices (2 cents)

- Net ticket yields turned positive in 3Q

- Capacity increased 2% (NA: +4%, EAA: flat)

- Occupancy: point higher than June guidance

- Net ticket yields: + 0.7% (EAA: +4% led by continental Europe and China); NA yields: down just over 1% due to continued promotional pricing environment in Caribbean

- Net onboard and other yields: +5.5% (considerably more positive than anticipated), increases in almost all categories.

- NCC ex fuel: up +0.5%, better than guidance due to timing of certain expenses

- 4Q yield: expect NA brand net ticket yields will turn positive

- Higher EPS for FY 2014 due to: 11 cents (better 3Q), 4 cents from fuel prices and currency.

- 1H 2015:

- NA

- Caribbean ahead on price and occupancy (56% of 1H 2015 capacity)

- European program: ahead on price and occupancy

- Booking volumes good at nicely higher prices

- EAA

- Ahead on occupancy; prices in-line with prior year

- Booking volumes higher YoY at slightly higher prices.

- Expect to offset inflation in 2015

- Aggressively rolling out EGCs. 16 ships beginning in FY 2015; 42 ships by end of 2015.

Q & A

- 2015 costs: 2/3 of cost increases due to dry docks; 1/3 due to 'investment in various areas of the business in terms of deployment and occu. Not afraid to reinvest in business to drive yields.

- Double digit ROIC target: 3-5 yrs

- Holding price while sacrificing occupancy is only a tactic; they will continue to use the tactic as long as it works

- Casino to-date has not been strong on CCL ships. CCL is purely a cruise product.

- Chinese govt has a plan for cruise development

- China: Lost money in 2006, broke even in 2012, made money in 2013/2014

- Additional onboard opportunities: casino/restaurants/beverages

- $75-80m cost investments

- Negotiations with airlines ongoing

- NCC ex fuel (excluding dry costs): flattish over 2015/2016

- Carnival brand: recovery a little faster than where mgmt forecasted

- Caribbean: very tough environment

- Capex 2014: $3 billion (similar levels for 2015 and 2016)

- China challenges: challenge is to communicate what is a cruise to the consumer; cruise port development; availability of international ports; infrastructure development.

- China: most ships are chartered; customers purchasing through a distribution network

- 2015 yield: late 2Q and onward should show better yields for Caribbean due to capacity reduction.

- Evaluating where some of Costa's/Princess's Asia ships will continue to use Euro functional currency

- May explore China partnership; Carnival chief operating officer Alan Buckelew will relocate to Shanghai.

- 2014 NCC ex fuel guidance raised: unexpected pension expense and some other expenses bumped the range up slightly.

- 2/3 of dry dock costs in 2015 will disappear in 2016.

- Optimistic on both NA and Europe in 2015

- 10 cent ECA cost: early season dry dock may offset a little of that; much of 10 cents will be eliminated in 2016 and gone by 2017 due to ECG implementations.

- 1% change in fuel efficiency equates to 2.6 cents in EPS. Expect 2-3% fuel consumption improvement going forward.

- Raised ticket and onboard guidance for 4Q

- Industry seems to be at or very near 2007 peak levels (mostly not coming from Carnival)

- Not worried about the new ships coming on line; industry capacity growth still manageable. Expect Asia to absorb much of the additional capacity.

- 2014 Net ticket yield increase: 50% from occupancy, 50% from higher prices

- Booking curve: 85%-95% (next Q), 50% (2Q out) 25% (3Q out).