Slightly better weekly results but still down YoY

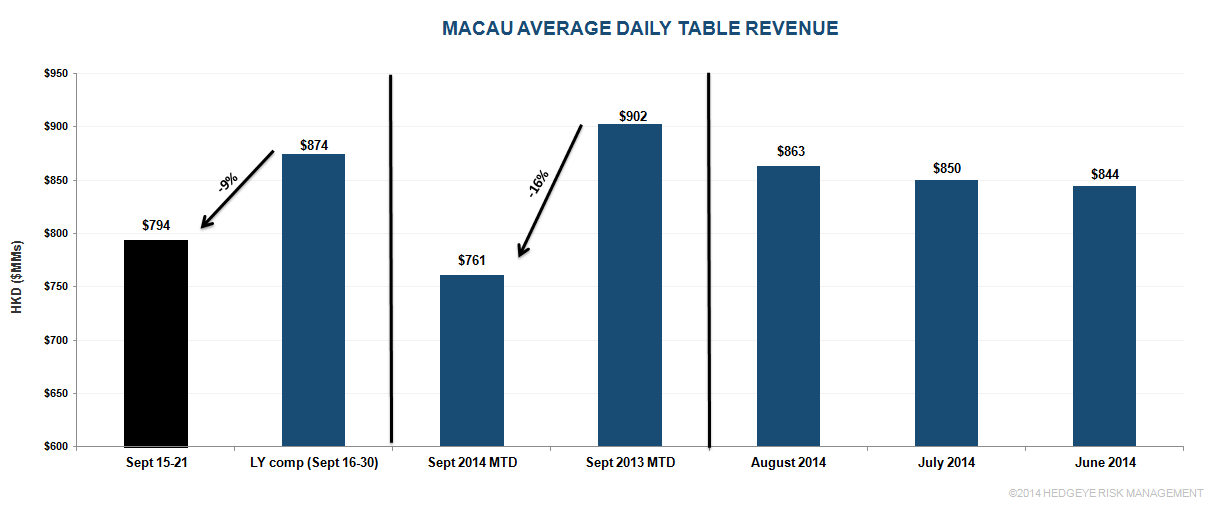

Through September 21st, table revenues were HK$15.99 billion. Average daily table revenues (ADTR) for the week (Sept 15-21) was HK$794 million, -9% YoY when compared with last year’s ADTR of HK$874 million for the period Sept 16-30, 2013. For the full month of September, we continue to expect gross gaming revenues (GGR – includes slots) to fall 13-17% from last year which would represent the largest YoY decline since June 2009.

We’re hearing that the normalization of Mass hold the past week may have led ADTR +7% week-over-week. Sands China may have held very low in the Mass segment in the 1st half of September (single digits) but has since normalized. There is a little bit of urgency in Macau as various management teams are discussing new mass marketing strategies including 1) moving more VIP tables to mass; 2) increasing reinvestment rates on loyalty club promotions by lowering entry points on packages.

Market VIP win % appears fairly normal but volumes remain weak but steady.

In terms of market share, Galaxy continues to lead the way, with MGM and MPEL also producing above trend. LVS, SJM, and WYNN‘s share remain below trend.

We think Galaxy is holding well in VIP, while SJM may be holding low.

Many eyes are rightly focused on the upcoming smoking ban. We believe Sands China could be the culprit behind yesterday’s warning by the Macau Health Bureau of an operator who did not completely separate the smoking areas from the mass market gaming areas.