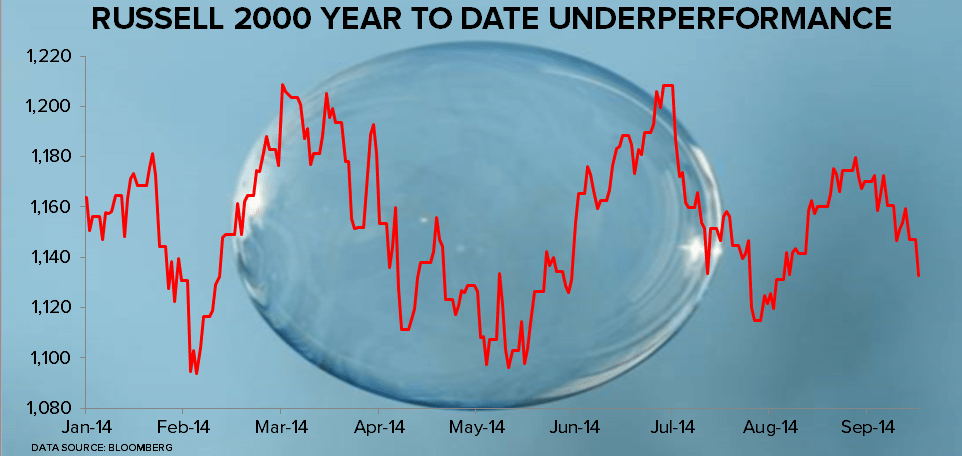

The Russell 2000 finished down -1.4% this past Friday, which of course was Ali-Bubble’s epic IPO day. It’s down another -1% today, bringing its total year-to-date decline to -2.4%.

While the bubble in illiquid, small cap stocks (over 50x trailing earnings) will only be clear in hindsight, we remain bearish of it in the meantime vs. big cap liquidity on the long side.

Tread carefully.