Investment Ideas

The table below lists our Investment Ideas as well as our Idea Bench -- a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

Notable Callouts

We are removing short PBPB from both our Best Ideas and Investment Ideas list. Note to follow shortly.

Recent Notes

09/15/14 Monday Mashup: SBUX, LOCO and More

09/18/14 Short SBUX Call Today @11AM

09/18/14 Short SBUX Call Replay

Events This Week

Tuesday, September 23rd

- JMBA Wedbush California Dreamin Consumer Conference 1:20 pm EST

- DENN Wedbush California Dreamin Consumer Conference 2:30pm EST

- KONA Wedbush California Dreamin Consumer Conference 2:30pm EST

Chart of the Day

Recent News Flow

Monday, September 15th

- DRI upgraded to outperform at CLSA with a $51 PT.

- THI announced preliminary 3Q14 quarter-to-date same-store sales of +3.6% in Canada and +7.0% in the U.S.

- RRGB announced it is two weeks away from opening its newest restaurant in Illinois.

- DRI filed an investor presentation regarding operating initiatives underway at Olive Garden and other restaurants.

Tuesday, September 16th

- JMBA introduced made-to-order Energy Bowls in stores nationwide. "Jamba's new Energy Bowls are a nutritious blend of real, whole fruit and soymilk or fresh Greek yogurt, topped with an assortment of dry toppings and fresh fruits."

- DNKN announced its commitment to 100% sustainable palm oil for all Dunkin' Donuts U.S. restaurants by 2016.

- SONC announced its FY15 outlook which includes EPS growth guidance at the high end of its 14-20% long-term target, positive same-store sales in the low single digit range, drive-in-level margin improvement of between 50 to 100 bps and more.

Thursday, September 18th

- DRI sent a letter to shareholders urging them to vote the BLUE proxy card "FOR ALL" of Darden's nominees. In the letter, Darden fired shots at two of its former employees - former Olive Garden President Brad Blum and former Olive Garden executive Bob Mock - who are currently working in advisor roles to activist Starboard Value.

- MCD increased its quarterly dividend by 4.9% to $0.85 from $0.81.

- TAST exercised its right of first refusal to purchase 30 Burger King restaurants in eastern North Carolina for a total purchase price of $20 million payable in cash. Carrols plans to sell these properties and lease them back for net proceeds of $13 to $14 million. Assuming the low end of that range implies that TAST is buying 30 locations for $7 million or approximately $233,333 per unit.

Sector Performance

The SPX (+1.3%) outperformed the XLY (+0.2%) as both casual dining and quick service stocks, in aggregate, outperformed the XLY.

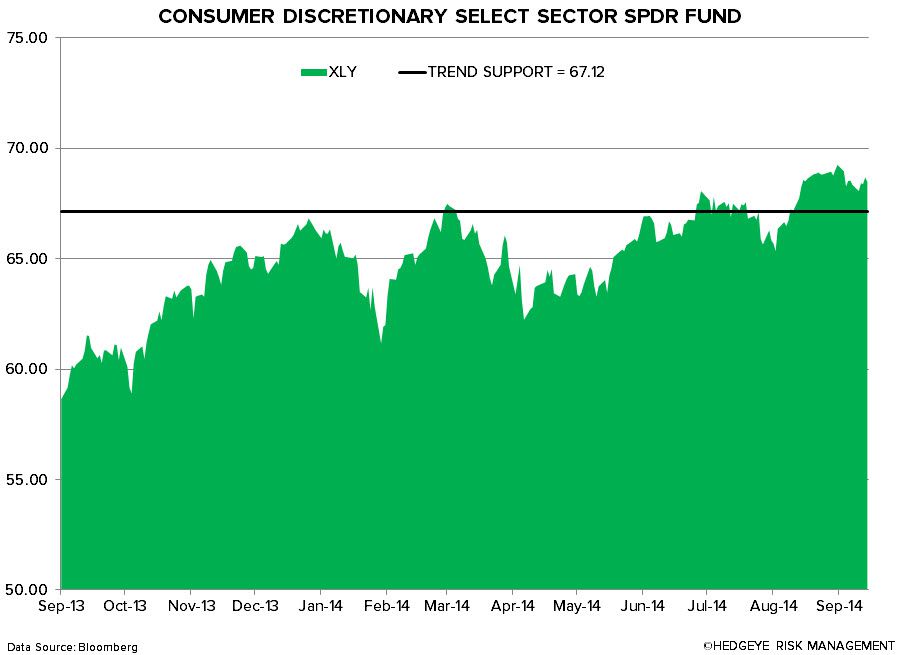

XLY Quantitative Setup

From a quantitative setup, the sector remains bullish on an intermediate-term TREND duration.

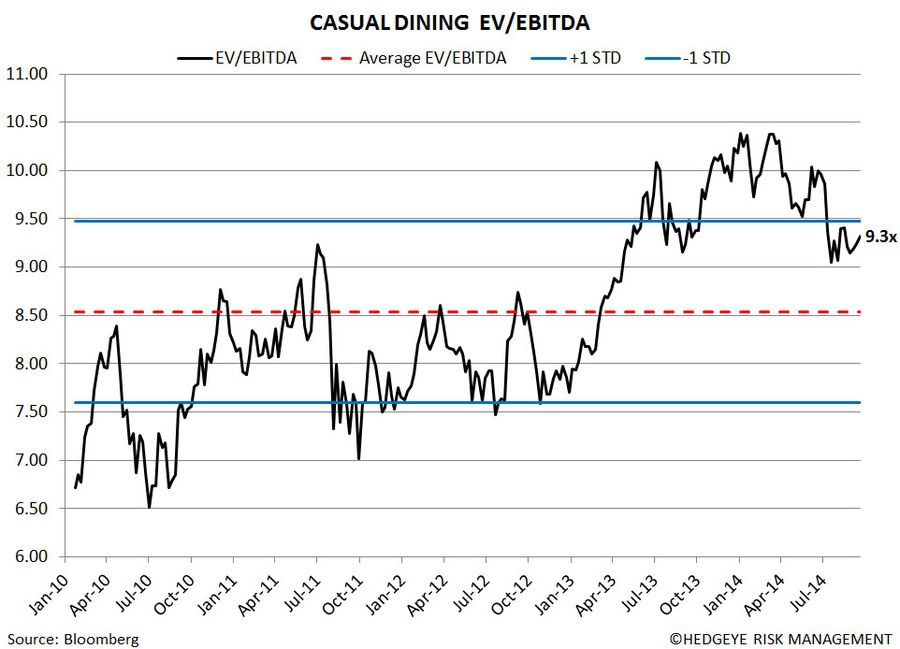

Casual Dining Restaurants

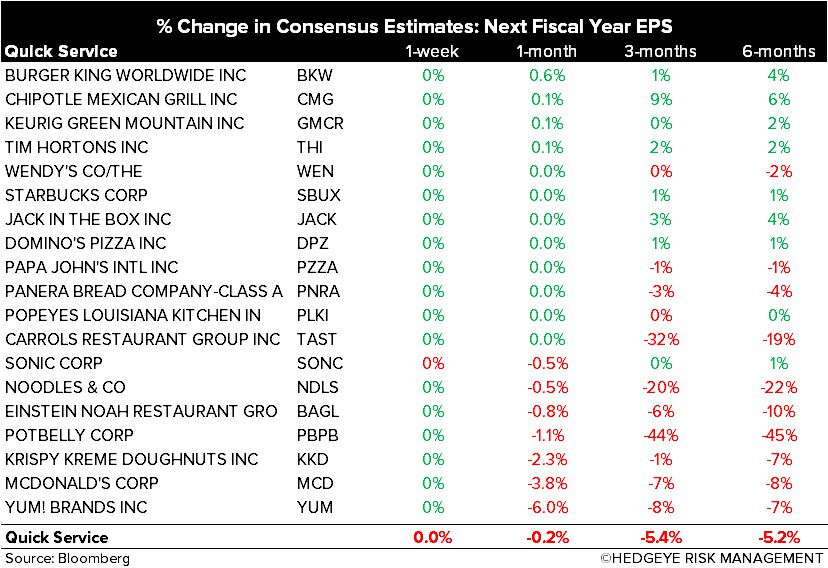

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst