Overview

We have ‘liked’ FedEx shares since late 2012, gradually reducing our affinity as the shares have moved higher (although a bit too quickly). With today’s gains, we will move to ‘roughly indifferent’. Much of the undervaluation in the Express division has been recognized at this point – perhaps 2/3s, if it were possible to provide such allocations. Management caution on 2H FY15 and static guidance may point to a softer second half. We preferred FDX when the Express division looked like it was detracting from the market’s valuation of FDX shares. We would look to re-enter at more attractive prices and would not short/underweight FDX shares. We do expect FedEx to be reasonably successful with its profit improvement plan and may again be exiting too early.

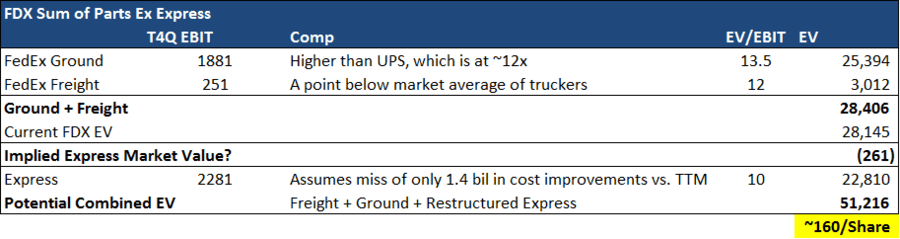

Updated Sum of Parts

We have written a critique of this valuation methodology and recognize its flaws. However, we continue to find it a helpful framing when explaining our views on FDX. We present a comparison of the June 2013 SOTP table with the current one.

Sum of Parts in June 2013 – FedEx Express Implied Negative Valuation

(published here, odd formatting included)

Sum of Parts Following FY1Q 2015 Results – FedEx Express Implied $15 bil Valuation

FY 1Q 2015 Results

We will let others provide a detailed review of FDX’s quarter, but pull out some highlights below.

Express Segment Margin: The FedEx Express margin has made progress, but still has a way to go to reach those of UPS and Deutsche Post. We do not see a reason that FDX’s profit improvement plan (PIP) will not significantly close the gap between FDX and competitors. That said, we think a good portion of the margin improvement is already reflected in FDX shares.

It Isn’t Just Apple Product Launches: Call Q&A seemed to imply that the quarter was just an Apple launch phenomena. FedEx Express may wish it were more closely tied to iPhone launches, but the data suggest they are largely unrelated.

Far From Outlier Results: FY1Q 2015 was better better, but without easy comps or with unusually strong yields/volume growth.

Yields improved slightly, most likely because of less International Priority headwind.

Volumes also improved, consistent with broader airfreight data.

Ground Still Solid: Management again commented that it won’t be satisfied with less than high-teens margins.

Freight’s Highest Margin: The best quarter since the financial crisis for FedEx Freight.

Guidance: Management commented that the stronger FY1Q 15 was factored into guidance and implied a weaker back half relative to consensus. Guidance may just be conservative, but guidance has been fairly on target in the last couple of years.

FedEx Investment Negatives: When we presented FDX as a long in late 2012, we often heard its myriad investment negatives. Many of them were true negatives, but we felt there was adequate compensation for the risks. That offsetting compensation is less available at current prices. Negatives include:

- The Express business is capital intensive and historically not a great generator of free cash flow

- FedEx Ground faces ongoing legal and regulatory challenges to its independent contractor model

- Belly space in wide body aircraft in the Asia appears a significant challenge, FTN or not