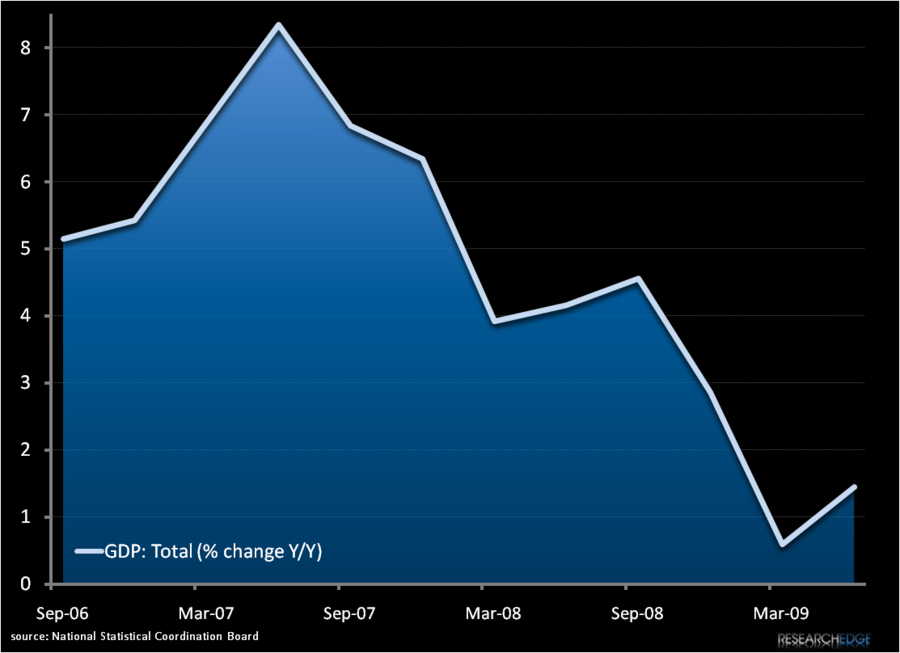

Forecasters were surprised by Q2 GDP data released in the Philippines today as the island nation’s economy grew by 1.5% on a year-over-year basis driven in large part by government stimulus.

Incremental improvements in smaller South Asian economies like the Philippines, Thailand and Malaysia are sending clear signals that demand is strengthening throughout the region as low relative rates help coax increased consumer spending and capital investments despite continued malaise in many exports markets in the west. Resilient demand from China is also moving the dial as exports and re-exports bound for “The Client” make up an increasing portion of total foreign trade (see the chart below showing US & China bound Exports as a % of Philippine total shipments.

Although we do not take positions in smaller economies like the Philippines, we follow them closely looking for signals and confirmation for our regional investment thesis.

Andrew Barber

Director